Searched “2 wheeler light manufacturers in india” on google and I could find more than dozens of manufacturers stating they supply to almost all brands. Not sure whether FIEM will have competitive advantage in long run.

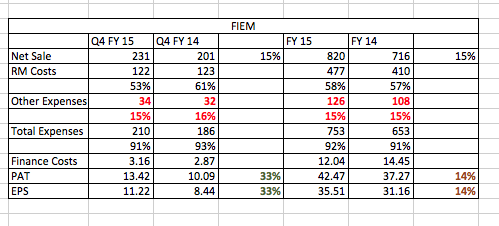

They had a good quarter with 33% PAT growth but overall year was just 14% growth.

They have ~15% as other expenses. Can somebody help figuring out - what are these?

I have studied this company recently in detail - not much on the valuations still, but much on the business/sector part. Auto sector has great growth opportunities in coming years. LED business in which they have diversified is also lucrative. Some worries/questions -

—> How much proportion of total Honda/TVS/suzuki orders for auto parts are supplied by Fiem? I find 44% of our revenues from sale of auto parts come from Honda. What importance do we hold to Honda? Are we just another fragmented supplier to these companies - with low pricing power.

—> Company’s LED business (street and house) is great- but govt driven. EESL will buy from these companies by way of tenders. Again no pricing power. Again how many players in this segment at present needs to be found out.

I worked in auto component industry and was involved in pricing discussions. Hence my further comments are coming from my past experience. Auto component suppliers have very less pricing power with their OEM customers. OEMs tend to have long term pricing agreements (with annual price downs built in sometimes) which forces auto component players to absorb most of the cost increases. Any new competitor brings in further pressure on pricing.

In short, only highly efficient low cost suppliers makes money in auto component market on OEM side. Most of them make money from aftermarket business (if the product has after market business). Hence suppliers of tyres, batteries, brakes, wipers and shock absorbers are more attractive due to their aftermarket business (provided they have good brand image) Very few suppliers like Bosch can command premium due to technology.

Hence any auto ancilliary stock could be short/medium term play on operating leverage (assuming they have spare capacity) but will struggle to be long term “wealth generators” unless they have huge after market business.

Also I think LED is becoming commodity, considering the fact that all players that has anything to do with electrical supplies, are entering into LED production eg. Eveready, Phillips,Bajaj,Syska,Anchor, Havells etc So I am not sure how much margins can be made in this business.

The company started doing conf call from last quarter. The stock looks interesting as one can expect many triggers to play out in next 6 months.

1… Honda Motors is increasing its two wheeler capacity from 46 lakh units to 58 lakh units. The new capacity will be operational from Q4 FY16. FIEM is setting up a dedicated plant for Honda’s additional capacity. Management mentioned in the conference call that they are targetting 150 cr revenue in the first year and 200 cr from second year onwards from this new plant.

The company is executing two orders for LED worth Rs. 150 cr. The order is to be executed before January 2016. One of the order is for street lights for SDMC Delhi. This order is of 100 cr. The second order of 50 cr is again for government for 7 lakh 9 watt LED bulbs. The company has booked just 10 cr from these orders in H1 FY 16. 140 cr will be booked in H2 2016.

The company is increasing LED capacity by nearly 3x. Currently, the company has capacity of 60,000 bulbs per day and 500 street lights per day. The management mentioned that capacity will be increased to 200,000 bulbs per day by March 2016 and 400,000 by FY17 end.

There has been a thrust from the government for using LED bulbs. There was an ET article which mentioned that EESL (Energy Efficiency Services Ltd) is going to float tender for 5 cr LED bulbs. EESL procures LED lamps in bulk through competitive bidding and distributes them to the consumers through power distribution companies. Power minister Piyush Goyal last month announced distributing 30 million LEDs under the scheme. All state governments have also been asked to procure LED and distribute in their states.

In anticipation of such demand, FIEM is increasing the LED capacity aggressively. The management claims that they are the only company who is doing 100% manufacturing in-house. Only LED chip is imported. This is the reason why they are price competitive. It is interesting to note that average price in the June tender was Rs. 77. FIEM bid was for Rs. 72. The management mentioned that margins in LED business will be more than Auto component business. They also mentioned that working capital will not be an issue in LED business and it will be similiar to auto component business.

FIEM EBITDA margins have remained in the range of 12-13% for last 3-4 years. This is unlike its competitors where margins have been volatile. Lumax which is its bigger competitor has margin of just 7-8%.

In the conf call, mgmt guided for 1000 cr revenues in fy16 with improvement in margins (due to higher share of LED business. the guidance implies revenue of 565 cr in 2H FY16 compared to 435 cr in H1 FY16. this implies 30% yoy growth in sales. with the current ebitda margins fiem can easily report 40% yoy growth in net income in 2H FY16. FY17 can also be a good growth year due to higher contribution from Honda’s Ahmedabad plant and increase in LED capacity.

Few of the risk which I can see are:

High client concentration: Honda forms 45% of the total revenue and TVS is around 26%.

Higher competition in LED business: There are bigger players like Everaddy, Havells, Crompton greaves who can bid aggressively in government tenders.

1…It is BIGGEST RISK

2…a…Fiem working from last 10 years on LED

b…Biggest R&D in INDIA(Working in Japan Italy)

c…Complete Backward Integration in LED EXCEPT LED CHIPS (I think they are importing)

d…Manufacturing cost can be reduced to any extent to tackle COMPETITION

e…Expecting HIGHER MARGIN in LED vs Auto ie…5 %

Have scope to reduce Margin to tackle competition

f…Turnover ratio in LED is about 5:1 and auto 2.5:1as per mgmt

3…Fiem OPTIMISTICALLY said Working Capital will remain same (I doubt This as working with GOVT there will be issue with Revenue recognition and cash flow and Increased Working Cap)

Some bacl leaf calculations on LED and street Light Business:-

New Planed Capacity ie…Additional Revenue apart from auto

1…LED Bulb :- 400000 per day

= 4 lack * 50 * 300 = 600 cr

Expected margin in between 5 % to 10 % ie…30 cr to 60 cr

2…Street Light :- 1000 per day

= 1000 * 1000 * 300 =300 Cr

Expected margin in between 5 % to 10 % ie…15 cr to 30 cr

We cam assume expected PE will be in between 15 to 20 in next 3 years

FIEM inds has reported very good set of Q3 results.

Sales up 10% qoq and 27% yoy

EBITDA up 14% qoq and 37% yoy (EBITDA margin at 12.9% vs 12.4% in Q2 and 12.1% in Q3 15)

Net profit up 25% qoq and 55% yoy

The co has also disclosed that 9M LED sales are at Rs. 55 cr. This means that Rs. 95 cr sales should come in Q4 from LED. (two order worth Rs. 150 cr are to be executed in FY16). Also, this implies that underlying auto ancillary business sales growth in around 20% yoy for the quarter which pretty good considering that the sales of its top 2 customers (HMSI and TVS) were impacted by Chennai floods in Nov and Dec.

The co has also mentioned in notes that it has commercialized its Ahmedabad plant for HMSI. FIEM had earlier guided for 150 cr revenue in first year from this Ahmedabad plant.

The stock increase as much as 10% in the last 1 hour alone after staying sluggish pretty much all day and hit it’s all time high of 859, after which it settled down in the next 4-5 minutes and closed at 823 in NSE, 5.76% in the green.

I did some research about this stock in the last one week and apart from it’s terrific numbers in the last 5 years, it’s CMF has been above 0 for the last 45 days or so, and was 0.14 yesterday. Also a look at it’s Bollinger bands clearly tells that it’s been expanding ever since the stock has crossed the upper band at 15 March.

I also learned that Economic Times has given a target of 895.

Disclaimer : I don’t have any investment in the stock. Also do pardon me if I made any mistake or disobeyed any rule of this forum, since this is my very first post here. Thank you all for reading!

FIEM had informed the stock exchanges that they have received an LOI from a UP based company for LED bulbs ( 7W and 9W ) for Rs 24 Cr approximately. This is to be executed in a 10 month period.

good set of results…25% sales growth in Q4. EBITDA margin improved to 13.7% in Q4 16 compared to 13% in Q3 16 and Q4 15. profit increased 45% in Q4 16.

revenue from LED business stood at Rs. 62 cr in Q4 16. 40 cr is still remaining to be booked from 150 cr order received during FY16.

press release mentions EBITDA margin in LED segment at 16.6% and auto business to be at 12.5%.

FIEM now trades at 16x TTM EPS.

Q1 FY16 should be good for FIEM as their largest customer (Honda Motors & Scooters India) has reported strong April-May sales. HMSI contributed nearly 45% to FIEM revenue in FY16. HMSI sales were up 27% and 19% yoy in April and May respectively. HMSI targets 20% increase in sales in FY17.

Also, 60cr order backlog in LED segment should be cleared in Q1 FY17.

So what about the other expansion plans which company earlier used to mention - MOU with some company to manufacture sockets, wires, etc. There has been no mention of that in the IP.