I have started this thread, since other thread doesn’t have much info and is locked.

company website:http://fiberwebindia.com

CMP: Rs 312

Book Value: Rs 54.47

Market Cap 449.15Cr

Face Value: 10

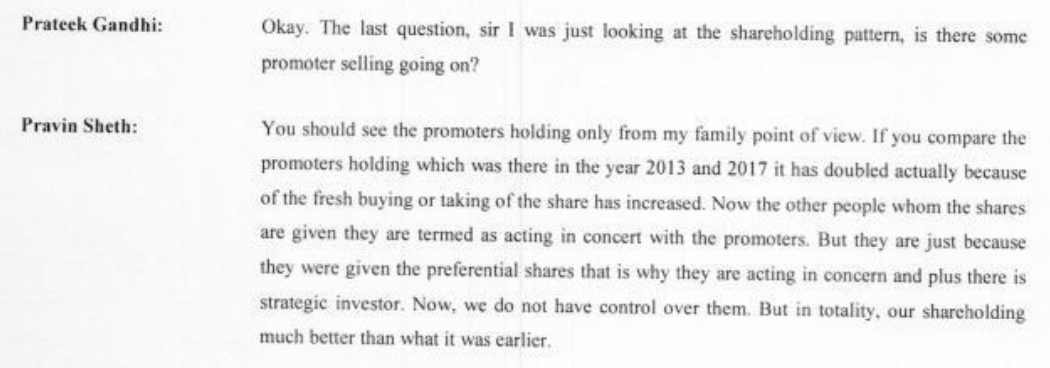

Promoters Stake: 52% (39.89 Mr.Seth Family)

Pledged: 0%

Debt Free

About FIL

Established in 1985, is 100% export oriented Spun bound nonwoven fabric manufacturer. once declared sick unit by BIFR, has come out of preview of BIFR and gained Star Export House status and now has positive net worth and is debt free.

Spunbound nonwoven fabric has variety of applications in hygiene products (baby diapers, adult diapers and sanitary napkins). Agriculture products like crop covers, wind and insect protection. Textiles like protective garments in hospitals.

Being Export Oriented Unit, FIL enjoys tax benefits from the Govt. and automated machinery procured from Germany reduces the manual labor cost.

Investor Presentation: http://www.bseindia.com/xml-data/corpfiling/AttachHis/d37ee2ef-9e66-4a4f-a372-89ed2f6c7f3a.pdf

What makes it interesting to invest?

Growing demand for technical textiles

Her is the link for the paper (http://www.reuters.com/brandfeatures/venture-capital/article?id=15814) (thanks to @madhavikkutti for the link)

As per the paper, Spunbond Nonwoven Market will grow by 8.5% CAGR from 2017 to 2025.

Value Added Products

Since FIL turned to manufacture VAPs from synthetic fabrics, turnover has inceased from 5-8% from FY16 to 15-16% in FY17. VAPS has high realization and margins.

Robust Orderbook

Link

Company order book is worth Rs105Cr till Q4, which grew by 29%, and bagged order worth Rs 10.9Cr on 28Aug.

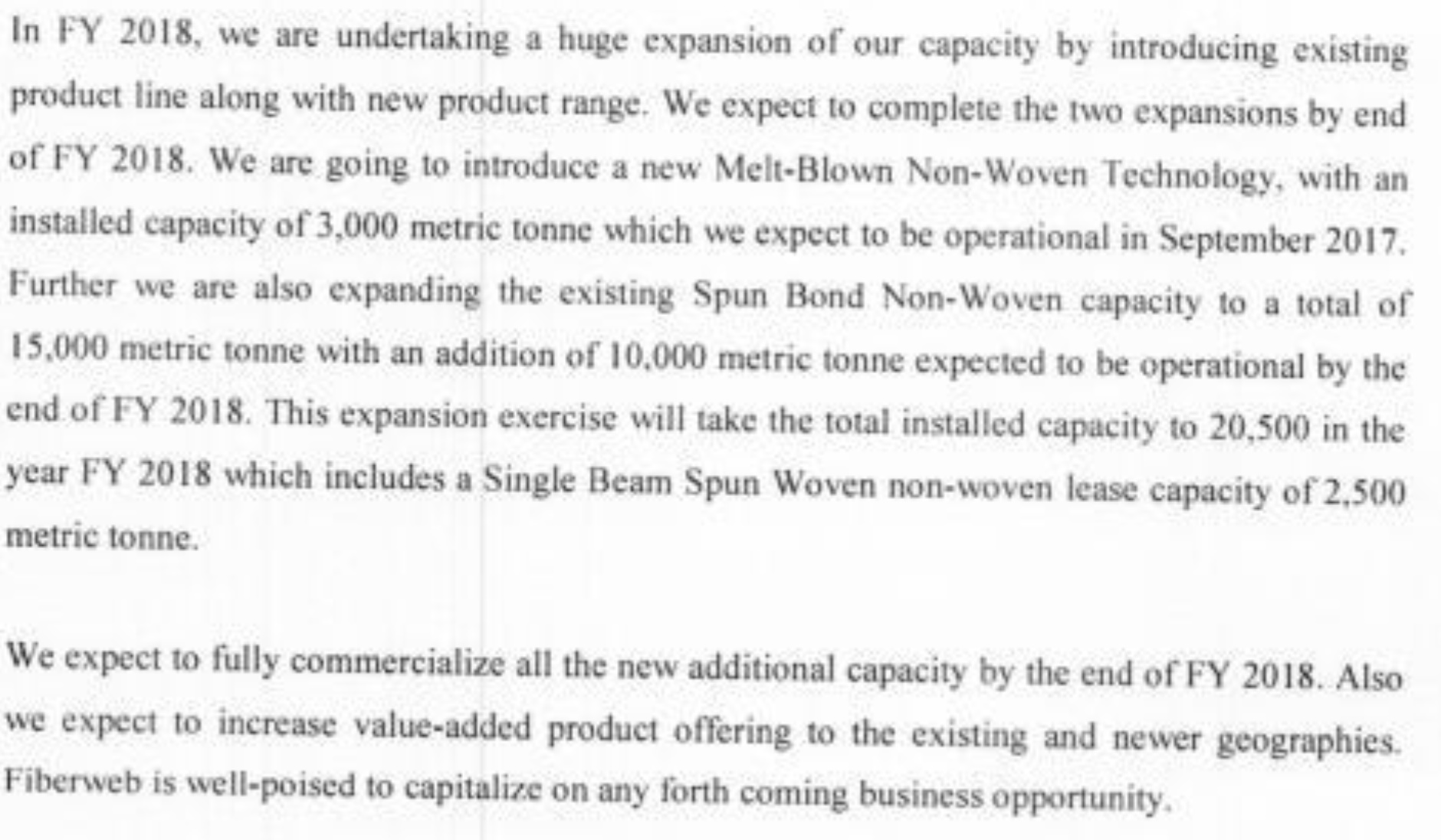

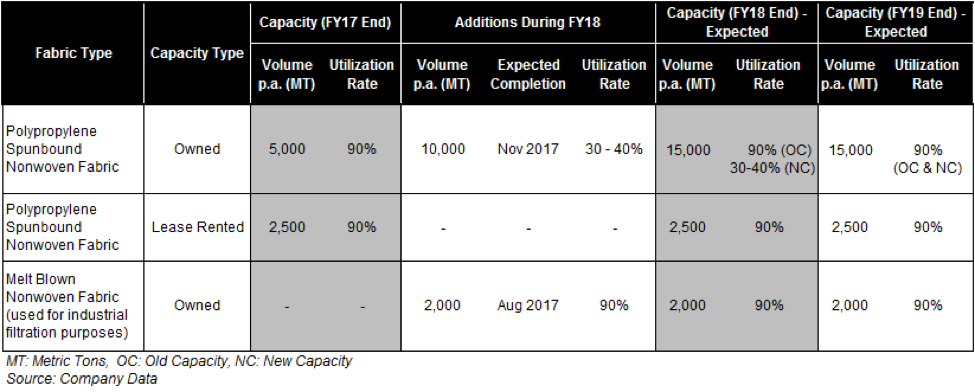

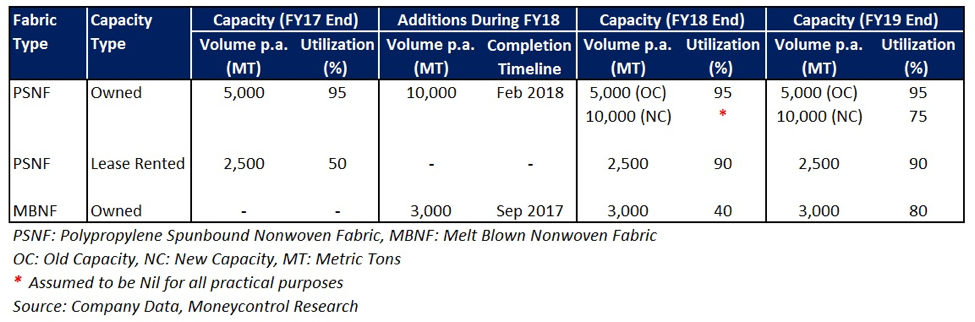

Capacity Expansion

Demand for technical texteils in the global market is huge and gap between demand and supply is about 25%., to tap into this opportunity management has decided to expand the capacity from current 7500 tons to 15000tons.

From ConCall,

3000tons expansion is due September 2017 will start contributing to topline and bottom line growth

100% subsidiary in UAE

as per concall, there are clients in US who need spunbound nonwoven fabric at less cost, they are ok to compromise on quality, since management do not want to spoil the reputation of FIL, 100% subsidiary of FIL is started in UAE which procures material from china and sell in US for 10% commission. Which is contributing to topline growth.

Here is the link for transcript of ConCall http://www.bseindia.com/xml-data/corpfiling/AttachHis/5fa95037-b651-42cb-9e95-4d7f31cd9856.pdf

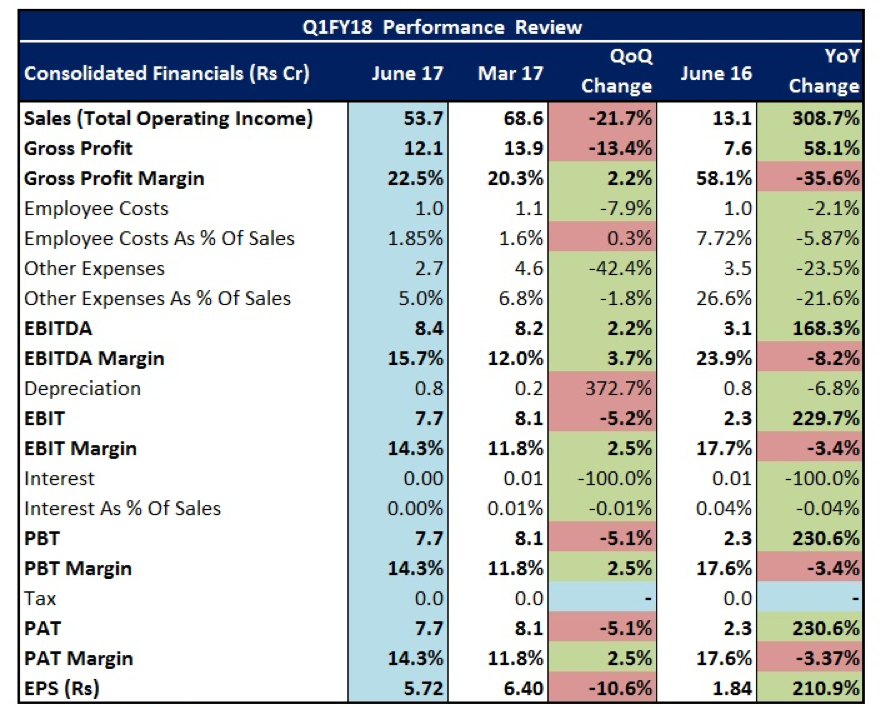

Good QoQ performance:

Risks

Forex fluctuations

Raw material cost

Fluctuations in crude oil prices will have impact on the raw material cost. FIL has consistent raw material supplier for over a decade now, which is competitively priced and good quality material provided by supplier.

Complying to Regulatory Checks

From company website, FIL has plant established to manufacture samples from the spunbound nonwoven fabric to check for quality compliances.

My personal opinion: catch it young watch is grow

Please do your own research before investing.

Desc: I have invested in this

Source:

http://www.reuters.com/brandfeatures/venture-capital/article?id=15814

http://www.moneycontrol.com/news/business/stocks-business/dnp-this-smallcap-gained-its-mojo-back-2284069.html

http://www.moneycontrol.com/news/business/stocks-business/fiberweb-india-fundamentally-promising-post-good-q1fy18-numbers-2361271.html

http://www.bseindia.com/stock-share-price/fiberweb-(india/#stock-opportunities)-ltd/fiberweb/507910