Gsfc – Analyst Meet

Q-What about Ammonium sulphate subsidy?

The ammonium sulphate Subsidy matter from 2013-16 has been submitted to Finance Ministry . It will resolved in 2-3 Month and company will get subsidy, Upto 2013 all claims are received . From March 2017 Claims for subsidy is getting regularly received from government.

DBK impact is still yet to see what will be the actual impact, but What we assume is going to happen is We will be in serious cash crunch for all the companies.

For P&K fertilisers the actual appreciation of sales is very limited very small window twice in a year and we have to keep on producing the material throughout the year. We are trying to address this thing :-

One is collect all our money like sodium sulphate, P&K , etc and going to create “wartches ” to manage our cash flow.

Second Long term goal is we are to open 800 outlets , So 30-40 % of our product is sold through our own store and then we were able to manage our product sales in a much better manner.

Thus we are planning to increase our outlet in our primary market of Rajasthan, Madhya Pradesh and Maharashtra.

We don’t want to expand very aggressively, first need to see business climate.

In Rajasthan it is going to start 6-7 outlets. In Madhya Pradesh and Maharashtra also process is going to open first pilot Outlets and see what’s impact and possible impact and then we will take decision.

So these are few strategies

Q-What is the current agro spread and given current economy and market scenario, How you see that fluctuate the near future ?

Our agro spread during last year was 911 $ and in current month there has been small increase in basic price but still two more trading is left in September Month. So we expect agro spread will be stable and in November and December there will not see any pressure from environment regulations so good season will be there in India.

Q-Will our volume like we have valued the earlier coated bill 1.9-2 Million Ton , Fertilizer Volume from FY 18 Now already Six Month Has been gone due to monsoon so what you think will we achieve that numbers ?

So Far We are on track, Our agro Business we are very much confident to achieve it.

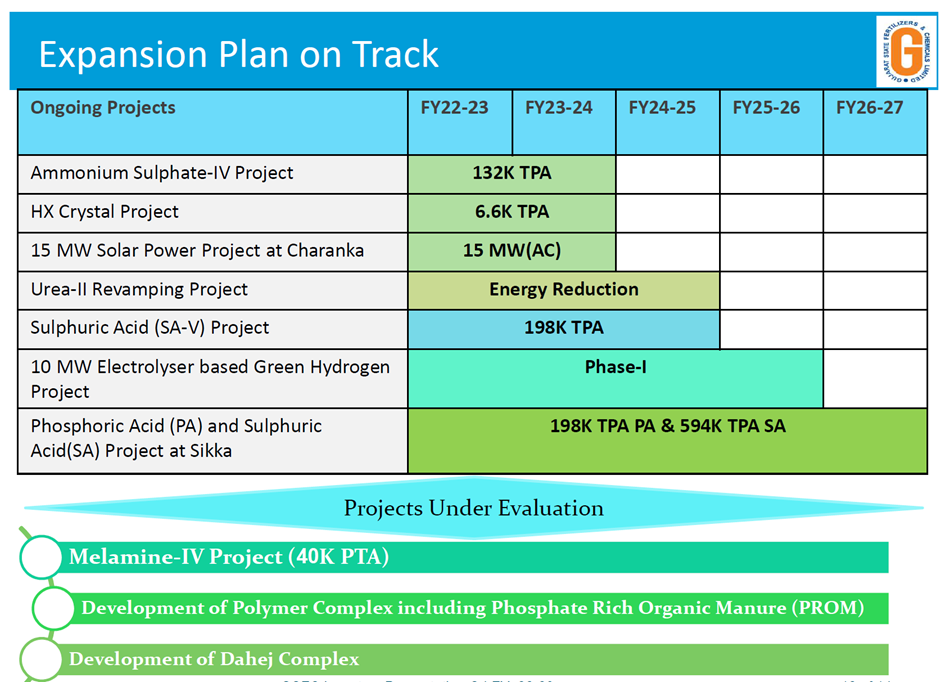

Q-In Immediate term we are looking on Capex of 400 Crore for Melamine. All other Capex will be coming in 2020-21 So First of all what will be the optimistic EBITDA we are looking for this Mega mine and what kind of initial ROE we are expecting and what will be Capex Schedule at 2018-19-20 ?

In Melamine as we got approval of 400 crore actual capex is of 800 Cr and we had already spend 400 crore on it and remaining 400 crore will be spend in this year or next year.

For other projects like Phosphorus Acid Plant and P&K Plant we are in planning phase will not give any commitment except a commitment would be a 10 Megawatt . So our projects expand will be in range of 50 Crores only. This Year we are working on rerating of our existing Ammonia Plant , Because after the Mega mine Plant we will need more Ammonia so we are working on that and expected the cost in a range of 150-200 Crore which will increase the production by 50,000 ton per annum and that will come in next 2 years step so expecting a outflow of 350 crore in next year.

Q-What will be the EBITDA generated on this Melamine?

See EBITDA Margins of melamine has been quite stable in last 3-4 years . In initial years ,So Capital cost will be more and thus EBITDA margin will be in range of 18-20%.

Q- In balance sheet there is an Old Mine non core Investment which is above 2500 Crore which is not giving any additional return so why we don’t think of diversify this non core investment ?

Ans- In our Investment, majority are strategic investments .

In Gujarat Industries Power Companies we are getting power in a capital power plant and we are getting power at a very reasonable price .

the moment we diverse ,we loose the capitive Power status .

The port at Dahej is a stragec Investment which is more important right now since we have acquired land there and got a board seat in it and also company has start paying dividends . We would like to remain in this typical port terminal project because of Dahej Interest.

Q-What about Gujarat Gas and GNFC?

GNFC is giving very high returns right now and we are the promoters of GNFC .Again another strategic investment .Initially infact we and state government came together to start it.

Gujarat State Communication Company is a another strategic investment where we are now taking advantage of water soluble fertilizers and GT is doing very good and having synergy with JJRC .

We have some small investments in Equities and even Gujarat Gas etc all these are cross holdings they have invested in us , the moment we withdraw they will also withdraw .

There are few shares of IDBI and Value Conductors . That we can say we will diversify we don’t have any interest and we have already taken decision to diverse these small ones including Gruh , IDBI and Manglore Chemicals, Rest I don’t think there will be any significant investment.

We are infact when second plant was Design , there was a space created for doubling our capacities . Space was kept for various sections for expansion so we have got rights under technology license to replicate the plant . We had started a project where we bring Caproplate from plant One (older plant) and quality has improved and one of the section new plant i.e second one is getting ready right now which will be ready from this December or January /

We have very serious thought of replicating other section and doubling our capacity and thus will be at very very low cost ,Because a lot of utility and manpower will be saved so our inventory of equipment and spare parts will also be saved.

Q- Since Last 50 years we have invested and in next 5 year we want to invest twice of last 50 years . So in next 3-4 years we will be investing around 4-5000 crores So What will be your vision about the company after 5 Year from now and how u are going to plan this 5000 Crores and as per Mr Nanavati Statement of getting 1000 Crore as bottom line after 4-5 years .

So whether 1000 Crore will be after providing whole financial cost and most important where you see this company after 5 years ?

Ans- We see that after 5 year this company will remain doing what we doing right now and we will do it more Professionally and we want to become a undisputed leader in phosphate Fertilizers One, Amonnium sulphate Two , Third is Caproplat and melamine. We are now focusing on our Capacity Efficiency we want to become most Efficient producers of these products .

Now Idle assets or lovely assets which have to start improving that return like JT where we are having around 160 odd acres of land , then we have bought 8200 cross pipeline to our plant and in the plant we have very elaborate logistics infrastructure and we are getting hardly 3 ships per month at this JT .

Now we have already completed a study as how we can harvest the best potential of this JT and it looks very attractive and If it will be properly manage then we expect around 10 Crores rupees will be annual net Profit come from this proper management .

I Don’t think that there will be any fertiliser company holding this type of asset and this will convert us to get a subsidy flow of good amount if manage properly.

Second we perceive that our future growth will come from Sikka .

Sikka is ryt now in 10 lakh annum capacity and all the raw materials are imported , so we want to now get into the backward integration by setting up a phosphorus acid plant which will give us adequate let say 50-60 % of future requirement also. So right now at Phosphorus plant is at initial stage and at the end of year it will close to maximum capacity.

So around 1.8 lakh tons of phosphoric acid will come from there.

If we set a one scale , around 3.6 lakh ton of Phosphoric acid this will give us opportunity to double our capacity at Sikka and we keep on importing little bit but Sikka we are targeting around 100 Cr net profit on Sikka . So Sikka will this profit will become more then aound 200 Crore net profit because Phosphuric acid plant will give a huge advantage from others in terms of cost of production.

Another thing we are doing like internal efficiency, we get 2 more assets which we don’t know where comparable, in filament and polymer unit . Now we are seriously working on either key assets become profitable or we just close the plants .

We has already shifted 100 Manpower from this 2 Units to our GFTL Outlets for further growth of it . So manpower is already stabilised now and Incase we are working on 2-3 options for both these units and one of the option we will take at this end of year. So when we talk about a 5 year stand, what will happen without much of investments these investments and expansion . Phospsuric acid require some investment , Caprocaite will require little investments, JT will require some investments . These 2-3 investments will give us a stable 4-500 Crore of rupees turnover and without other things we were talking So we are targeting CAGR of 24.

Internal efficiency will help us to achieve it .

Q- Wouldn’t you and GNFC coming together will give any benefits , will it make any sense ?

We don’t find any commercial relate as both are in different segments .We are Ammonia based company and GNFC besides an ammonia plant they are more on Carbon Monoxide .

The raw material is also different .So these doesn’t make any synergy between these two companies .

Q- GST Impact

Ya so your observation is right that importer of DAP is charged at 5% and sales at 5% , While in processed ammonia it will be 18% GST, so we have more input credit . But for us , we have other chemicals where unlike other fertiliser companies We charge 18% GST on Sales. So we can set off 18% GST paid on imported processed ammonia .

So it will come under huge refund case but now it wil be a question for all when government will refund . It will create impact in blockage of Working Capital. We expect to set off this on month to month basis so we don’t expect blockage ITC Credit on a long term basis .

First Priority is of launch of GST then to take care of Second to take care of technical features .

Future Outlook

The Company thinking in short term and near term goal in 4 - 5 areas.

- Capacity increase because we rely most on imports so we want to be self reliable,as there is sometimes cartelisation of international suppliers .

- Set up phosphorus acid plant , thus we are also taking with suppliers .

- Increase retail network by forward integration .

Implement of direct subsidy transfer is in process .so that we will have direct transfer of subsidy amount at time of actual sales .

Increase number of retail chain that will increase sales faster

- In cost cutting we have the target of 135 crores cost cutting which will achieve soon this initiative was taken from 01 October 2016 onwards this june we have a good avievement and we decreasing it on a sustainable basis .

Product differentiation - As we know DAP is a commodity product .So we wanted to differentiate compress DAP from other companies .

We are welcomed in outside Gujarat and Punjab State to cater huge demand of further DAP .

As of now , we are coming forward with 3 type of DAP variations premium , gold and the gold type . We are expect to come of by Dec 17 , So that will Differentiate us from other DAP and we hope that GST will be able to have a better market share plus some price improvement also .

Last time suggestions of efficient capacity utilisation is taken into consideration and this time seriously investment planning in SIKKA and Huge Saving by JT , Tanla and Mundra. 5-600 rupees steam loading while Sikka has to pay 70-80 rupees only on infrastructure so that will be a huge cost advantage with the better expansion and utilisation of plant .

We Can have a huge trading opportunity in liquid as well as bulk products so in that are we are talking to Gujarat gov to increase technically and we will have some kind of tie up with them so that better utilisation of this JT is made.

So From this backward and forward innovation, cost cutting , product differentiation and factory utilisation of asset and we belive that the finest time We should be able to add 4500 Crores to bottom line so with the existing say for net crores of average in Fy18 we should be to able to generate good figure of 1000 crore in coming days so I think that is the best way we can serve our all kind of stakeholder and give and hansome returns to them