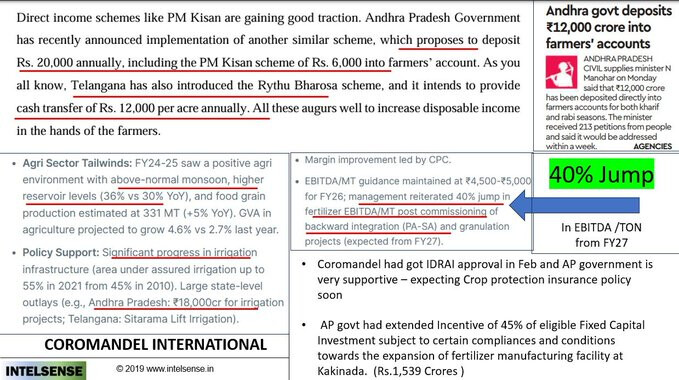

Recent Hike in NBS rates - A move expected to benefit Integrated Players

The Indian fertiliser industry operates within a tightly controlled regulatory framework. Pricing, supply, and distribution are heavily influenced by government policy, especially via the fertiliser subsidy regime.

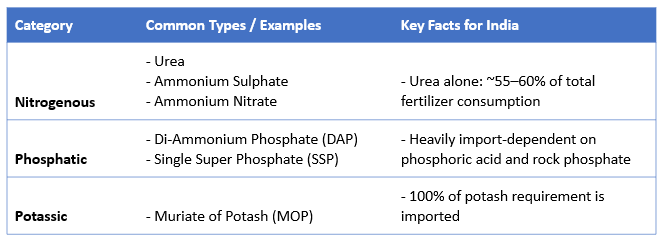

Fertilisers can be broadly classified into 3 categories:

Complex fertilisers or NPK fertilisers

These are blended or chemically granulated fertilisers that provide a mix of N (Nitrogen), P (Phosphorus), and K (Potassium) in various “grades” tailored to crop and soil requirements.

An NPK grade indicates the percentage composition of Nitrogen (N), Phosphorus (as P₂O₅), and Potassium (as K₂O) in the fertiliser.

For example, grade 10-26-26 has the composition of—10% N, 26% P₂O₅, and 26% K₂O.

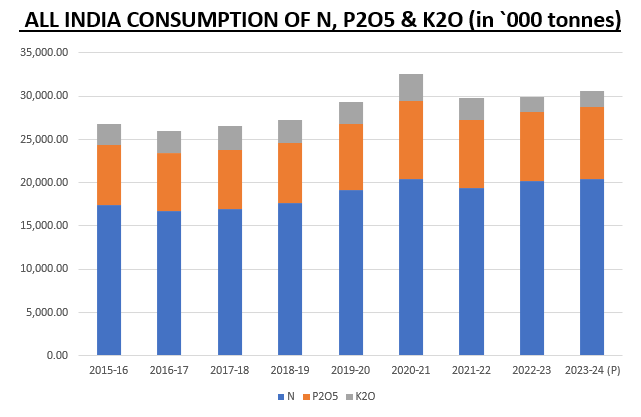

India is the second-largest consumer of fertilisers globally after China and consumes over 60 million tonnes annually of urea, phosphatic, and potassic fertilisers. Fertilisers contribute directly to food security by enhancing agricultural productivity—over 50% of crop yield increases are attributed to fertiliser use.

Challenges of the previous pricing schemes

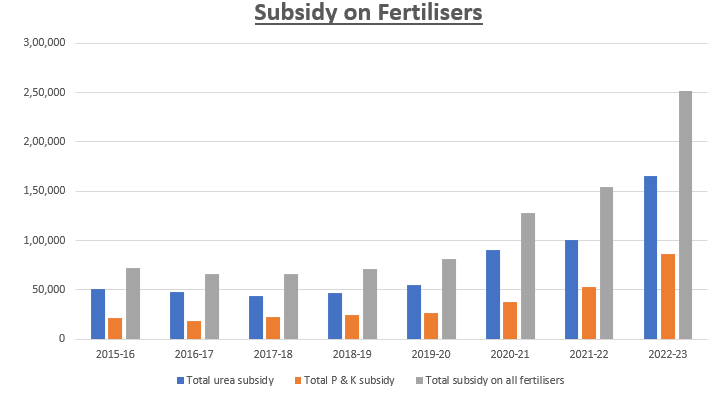

Launched in April 2010, the Nutrient-Based Subsidy (NBS) scheme was introduced to bring efficiency, transparency, and balanced fertiliser usage while keeping fertilisers affordable for farmers.

Prior to its launch, the Government controlled retail prices (MRPs) of most fertilisers (Urea, DAP, MOP, etc.). It also reimbursed manufacturers on a cost-plus basis, i.e., based on production/import cost + reasonable return. This was known as the Retention Pricing Scheme (RPS) and later as the Group Concession Scheme (GCS).

Urea had the lowest MRP, and due to price distortions, farmers overused nitrogenous fertilisers. This led to an imbalance in nutrient usage. For instance, the recommended N:P:K ratio is 4:2:1, but India reached alarming levels like 8.2:3.2:1 (2008–09), harming soil health and crop productivity.

Since prices were fixed, companies had no incentive to improve efficiency or introduce new fertiliser formulations. Focus remained on producing subsidy-favoured products, even if not ideal for local soil needs.

Introduction of Nutrient-Based Subsidy Scheme (NBS Scheme)

NBS Scheme was introduced with the following objectives:

- Promote balanced fertiliser use (avoid nitrogen overuse and improve P & K application).

- Encourage competition among producers for better efficiency and innovation.

- Improve the availability of complex and customised fertilisers suited to regional soil needs.

- Reduce fiscal burden by moving from product-based to nutrient-based support.

Under this Scheme, the government fixes a per-kg subsidy rate for each nutrient: Nitrogen (N), Phosphate (P), Potash (K), and Sulphur (S). Fertiliser manufacturers/importers are then free to set retail prices (MRP), but after accounting for the subsidy, the farmer still pays an affordable amount. The subsidy is paid directly to the manufacturer based on the quantity sold.

NBS made subsidies predictable and nutrient-linked, thereby reducing the fiscal burden. Also, by allowing firms to set MRP and compete it has promoted innovation among manufacturers encouraging custom NPK grades and specialised blends. This has made tailoring fertilisers to crop & soil-specific conditions possible unlike the previous system.

The Nutrient-Based Subsidy (NBS) rates in India are typically revised biannually, aligning with the country’s two main agricultural seasons:

- Kharif Season: April 1st to September 30th

- Rabi Season: October 1st to March 31st

However, these revisions are not strictly confined to this biannual schedule. The government may adjust the NBS rates more frequently in response to significant fluctuations in international fertiliser prices or other market dynamics to ensure the affordability and availability of fertilisers for farmers.

In its most recent rate revision in March 2025, the Indian government approved revised Nutrient-Based Subsidy (NBS) rates for the Kharif 2025 season (April 1 to September 30, 2025), significantly increasing subsidies for Phosphorus (P) and Sulphur (S) to ensure the affordability of essential fertilisers for farmers.

March 2025 Key Adjustments:

- Phosphorus (P): The subsidy was increased by approximately 42%

- Sulphur (S): The subsidy saw a 48% rise

This is a welcome move as post the Russia-Ukraine war, prices of phosphate rock, ammonia, sulphur, and phosphoric acid have seen extreme volatility, leading to sharp cost increases for fertiliser manufacturers. The increased subsidy rates are likely to benefit integrated complex fertiliser players.

Outlook

The sector looks well poised for growth, given that the companies are expanding capacities and entering into partnerships to secure key raw materials. Given that we rely mostly on imports and agricultural yield being a critical factor from the standpoint of food security, the government is also looking at supporting the industry from a strategic perspective.

Largely insulated from the ongoing tariff war, except for the volatility in crude oil and hence natural gas prices, the sector seems to provide an interesting hunting ground for investors also amidst the heightened global uncertainty.