Src -

2 Likes

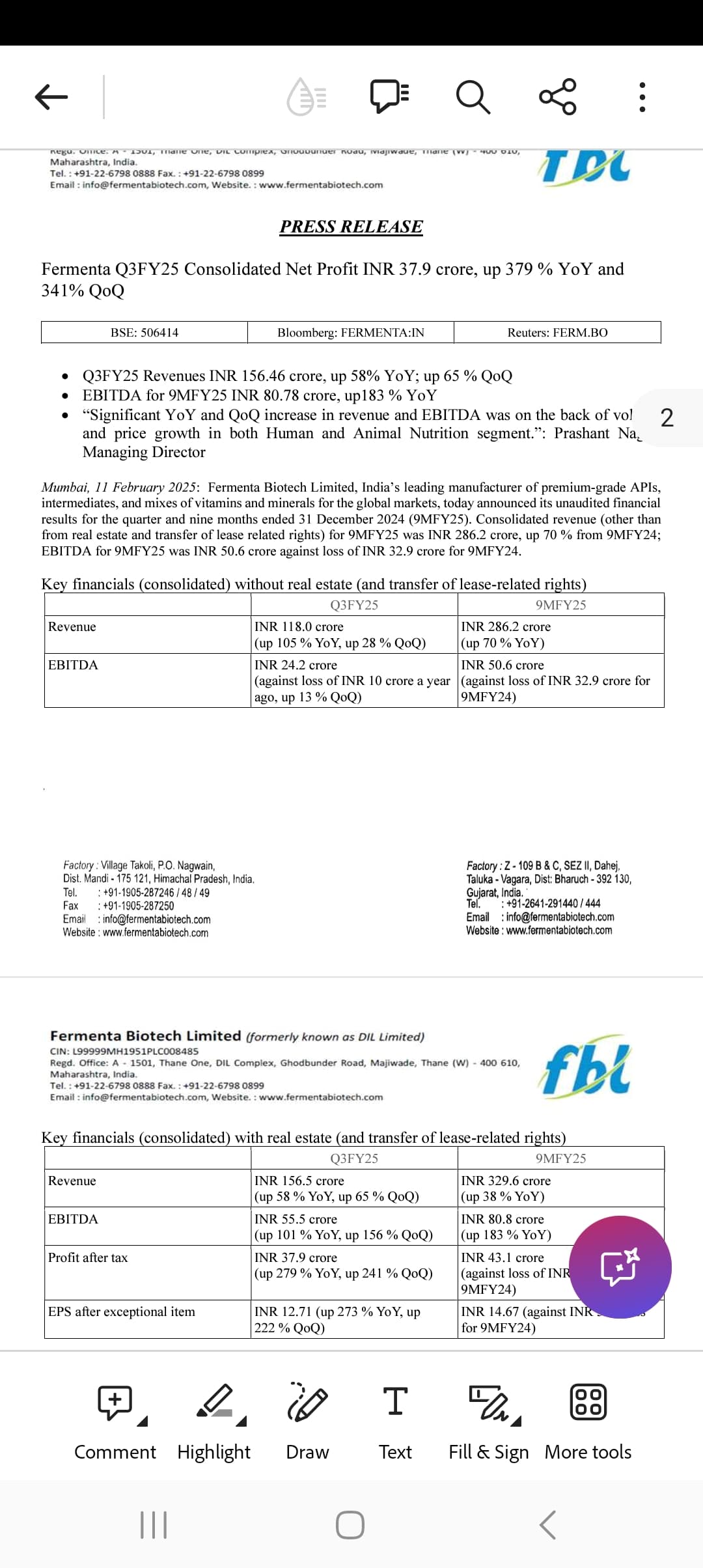

Fermenta announced Q2 results yesterday and the numbers were fantastic.

Fermenta Q2 Results.pdf (2.5 MB)

- Sales grew 67% YOY to 95 Cr, boosted by the substantially increased Vit D3 prices

- OPMs have already turned around drastically from -24% last Q2 to +20% this Q. This meant EBITDA also turned around from ~(-20) Cr to 20+ Cr for the Q

- Most of the contracts for higher Vit D3 prices would only be fully signed in Q3, so in my thesis I assume a much stronger Q3 over Q2, with further increases in sales and OPMs. OPM in peak Vit D3 price cycle in 2019 for reference was ~39%.

- Company has restructured and reduced debt through recent real estate sales

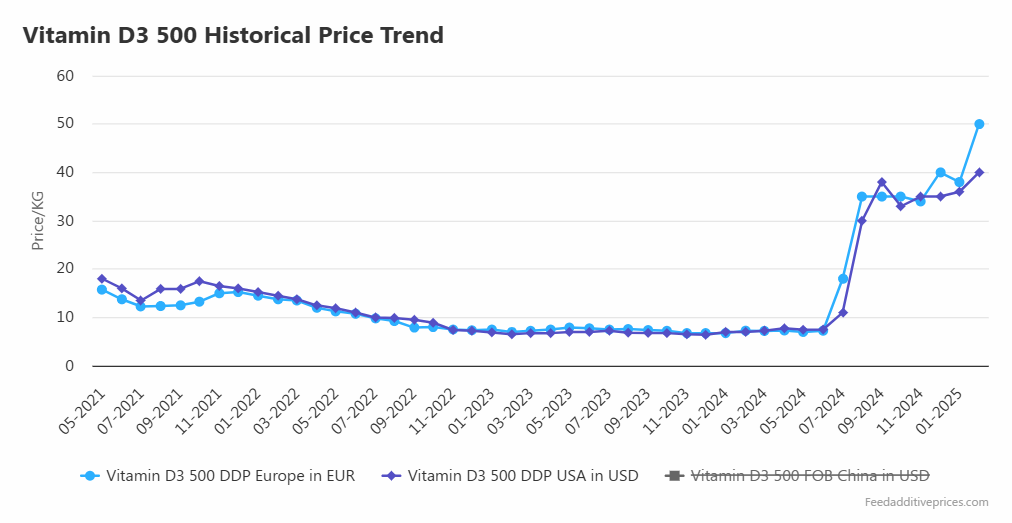

At the same time, Vit D3 prices continue to hold strong comfortably above USD 30, and this should hold them in good stead for the coming year with a very low base of Q3’24, Q4’24 and Q1’25 ahead.

Disclosure : Invested

5 Likes

Things are getting only more interesting here - prices have moved up further to 50 EURO/kg and $40/kg. The company is also selling off non-core assets every other month, would be very nice if they started hosting concalls to shed more light on the intricacies of the business.

Disc - Invested and Bullish

2 Likes

What happened with Q3 results? Here are my quick thoughts.

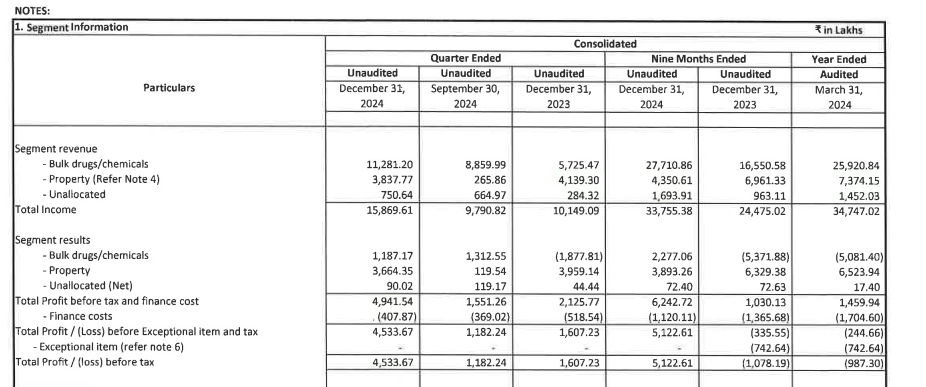

1 EPS increased because of property sales only.

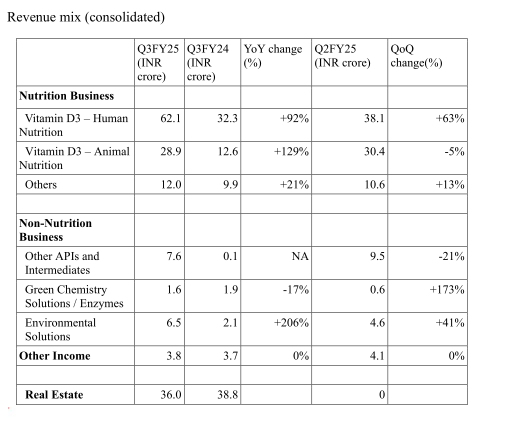

2 D3 revenue went up but margins seem very low ~10%

3 Market reacted positively at first and then brought it to 20% LC

Anyone have any comments or insights?

Invested at ~370 levels

Somehow the company managed to decrease margins from Q2 from ~16% to ~10% in Q3 when prices of vitamin D are rising. How is this possible? Company put up another document with revenue from vit D for multiple quarters but no information on margins. Scratching my head how they got this done…

1 Like

Investor PPT for Feb 25 uploaded.

This contains no details of Vit D margins, Only consolidated revenues. Can anyone understand how bulk drug margins are so low this quarter?

1 Like

Overall drug ebidta 24 cr from 118 cr sales translate ~ 20 % margin which excluded 4.14 cr of last quater inventory and not included in this quater such inventory makes EBDIT margin around ~ 30 %

Hope I am right here

Not sure if we are looking at the same figures. The only place I am able to find segmental revenues is in Q3 results not investor PPT. Bulk drug ebidta is 11.8 cr on rev of 112.8 cr which gives ~10% margins. Real estate sale ebidta is 36.6 cr on rev of 38.3 cr.

Where did you get the 24 cr ebidta figure for drugs?

Thanks for pointing that out. How do these nos compare to segment wise nos in the P&L statement

Trying to understand this better. Segmental revenue seems to convey a different story. What am I missing?

They not included inventory of this quater in cost calculation & reversal of last quater inventory of 4.14 cr that i understand from reading notes, which may reduce EBIDTA in segment results than actual

1 Like

That must be why they released the PPT later. Would be so much better if they could do a conf call and clarify what’s going on. I think the segmental revenue isue is why the stock went down after going up immediately post results…

Agreed, bleeding significantly due to this even after batter performance expected in next coming quater

1 Like

Went through the Q3 numbers and although a bit has been covered below still adding my 2 cents to the discussion:-

- Yes segmental OPMs are lower than last Q for the bulk division, but it largely seems to be due to increase in Other Expenses (Head 3g) in the segmental results. This is ~9 Cr of additional expenses, which the company has detailed in Note 5-8, also discussed in posts above

- Adjusting for this, OPMs are higher than last Q, but still below my expectations considering the drastic price increase

- My assumption for why this could have happened in the absence of any details from the company is that they would have long and short term contracts with customers, so it would probably take some time for higher prices to be reflected in the OPMs due to the longer contracts, hopefully incrementally in the next 2 Qs

- Vit D3 Prices continue to trend higher up and are now touching USD 45 China FOB

Disclosure : Continue to be fully invested in self and FO accounts, biased

2 Likes

Thanks for sharing your thoughts! Your initial post got me interested in the company…I was surprised by the segment results for this quarter which were not immediately clear post results.

Really wish company would start conf calls as they have done previously… Would provide much more clarity about the promoters, their contract situation especially with the Vit D prices rising, and the real estate biz that they seem to be monetizing.

Hi, has the company stopped producing animal-based supplements? as they have come up with plant based patents.

(Asking this to check if the company falls in my investment philosophy)

1 Like

Plant based patents is new thing and it’s in regulatory approval. having both Human and animal based supplements. Pls go through below investor presentation