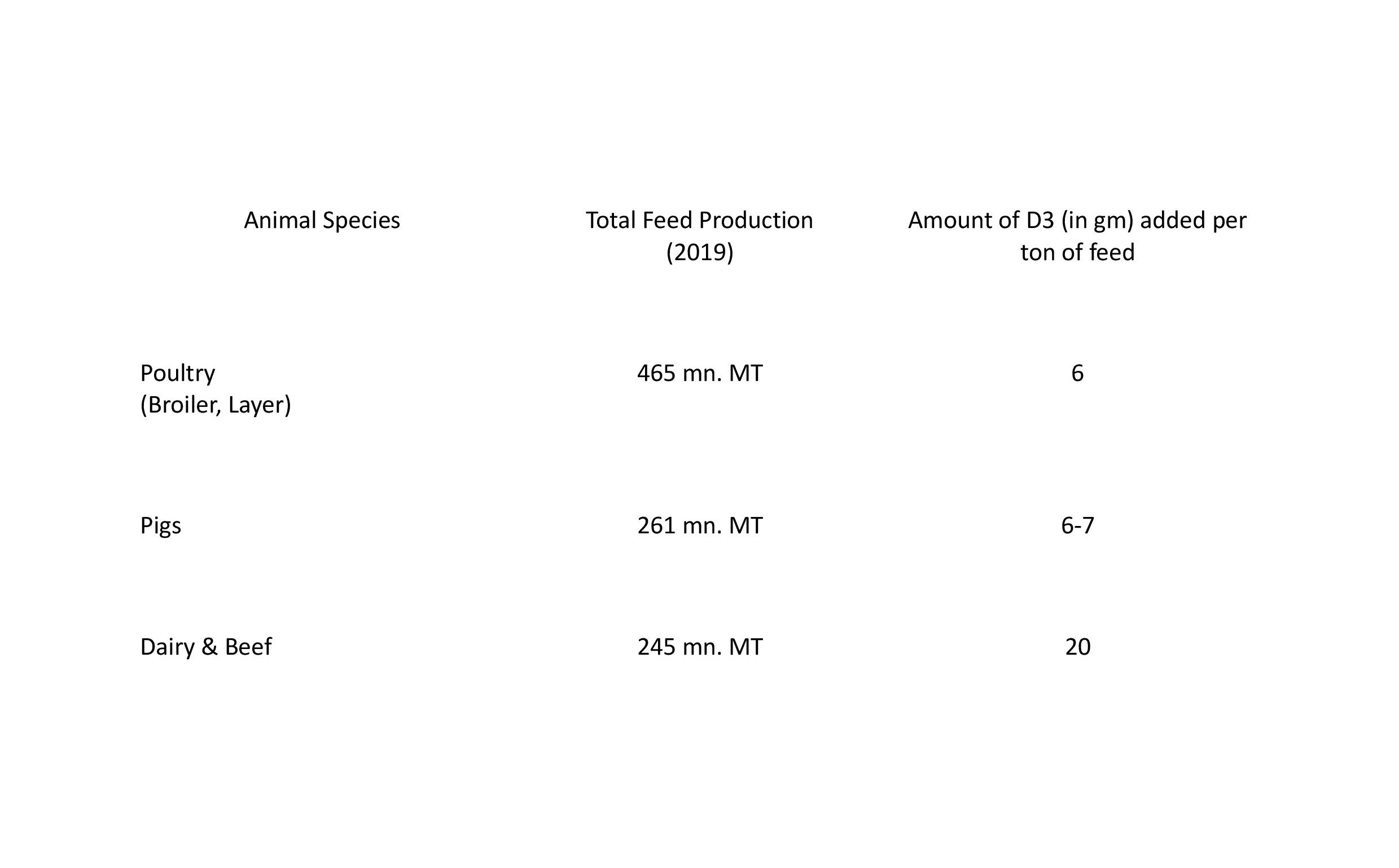

Feed Grade Vitamin D3 constitutes 70 % + of the industry demand. Vitamins are used as nutritional additives in animal feed as they play a vital role in maintaining normal immune function of livestock and poultry. Modern farming conditions devoid animals of natural conditions like sunlight, soil and green feed. Nutritional additives in the form of vitamins and minerals are therefore needed the most. Below is the recommended addition of Vitamin D3 in the feed of some animal species :

2019 Total Global Feed production is estimated at 1126.5 mn. MT p.a. On an average it is estimated that about 6-7 gm of vitamin D3 needs to be added for every 1 ton of feed which puts theoretical demand for feed grade Vitamin D3 at ~6750 MT p.a.. However, it is called ‘theoretical’ demand only as historically it is being observed that feed manufacturers adjust the quantity of feed additves added w.r.t. price change of feed additves. Because of this, although Vitamin D3 constitutes below 1 % of feed cost, yet demand is largely dependent on the price of vitamin D3 – when the price is low, demand is high whereas when the price is high, feed manufacturers adjust the quantity added and therefore volume of D3 sold actually decreases. This is the reason why Zhejiang Garden Biochemical, which is world’s largest player in Vitamin D3 market, sold 1942 MT of feed grade Vitamin D3 powder in CY2008 when its price was INR 238 per Kg whereas in CY2018, when price of Vitamin D3 skyrocketed to INR 4126 per Kg, it sold only 856 MT which doubled to 1775 MT in CY2019 when price halved to INR 2600 per Kg.

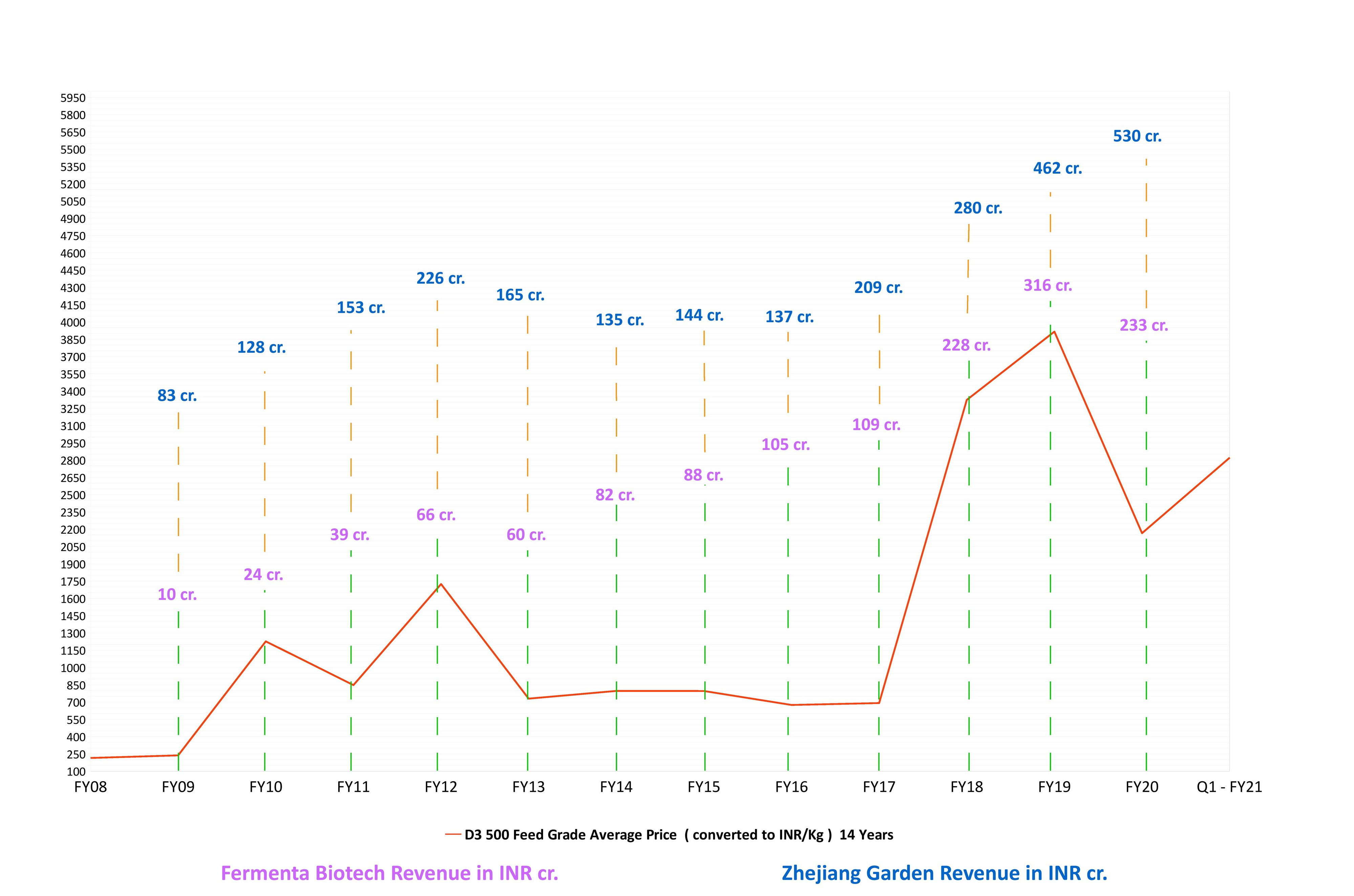

It is interesting to note here Zhejiang Garden Biochemical’s yearly sales volume in MT of Vitamin D3 Feed Grade Powder over last decade :

Green line in the chart above depicts the volume of feed grade vitamin D3 powder sold by Garden Bio each fiscal, which we can observe has largely remained in a range and fluctuated based on price of the product.

On supply side also same thing is there – when the prices skyrocket, existing players aggressively expand their capacities as also players who had exited in past but have idle capacity come in ; when the prices plunge weak players exit because of losses and market price makes a trough. When we look at last 13 years price data of feed grade Vitamin D3 the same thing can be observed – In April 2009 prices plummeted to a record low of then decade to touch INR 218 per kg (even in 2001 it was INR 575 per kg) post which it recovered to touch a high of INR 1990 per kg in Feb2010 after which it again went down gradually to hover around INR 600-700 from FY13 to FY17. Then, from FY18 it has had a sharp rise to touch INR 6100 per kg in August 2018 post which it has fallen down again to touch INR 1200 per kg in Feb2020 to recover to INR 1900 per kg in June2020.

To cite here an example, as against theoretical demand of feed grade Vitamin D3 of ~7000 MT p.a., we have ~8500 MT p.a. production capacity distributed amongst just 5 major chinese companies – Zhejiang Garden Biochemical, Zhejiang Xinhecheng, Taizhou Haisheng, Xiamen Jindawei and Zhejiang Pharmaceuticals. Here, we are not considering few small chinese companies who have small capacities to produce feed grade Vitamin D3. Also, we have not considered here the production capacities of DSM.

Hence, what we actually have is ~11500-12500 MT p.a global production capacity for production of Vitamin D3 (Feed+Food grades) as against global theoretical demand of ~10,000 MT p.a. (Feed+Food grade combine).

Over the course of next few years we need to observe the price trend as – first – feed producers themselves are under pressure because of worldwide corona pandemic – and second – new capacities of Vitamin D3 are coming up in china – majorly in CY21.

||||||

If we talk specifically for Fermenta’s feed grade market –— China, which contributes ~18 % to global feed production, is out of its reach as chinese producers themselves will be addressing that market. India, which majorly produces dairy and poultry feed and contributes ~4 % to global feed production – this might be simpler to address for the company. USA & Europe market which forms more than 40 % of global feed market are where company can focus on and compete with chinese players especially, Zhejiang Garden, which can compete aggressively on pricing. USA-China Tariff wars have still not touched this product and there has been no effect on chinese company’s sales due to that.

It is interesting to observe Zhejiang Garden Vitamin D3 (combine – Animal & Human) sales vis-a-vis Fermenta’s Vitamin D3 sales (combine – Animal & Human) over last many years in the backdrop of Feed Grade Vitamin D3 pricing :

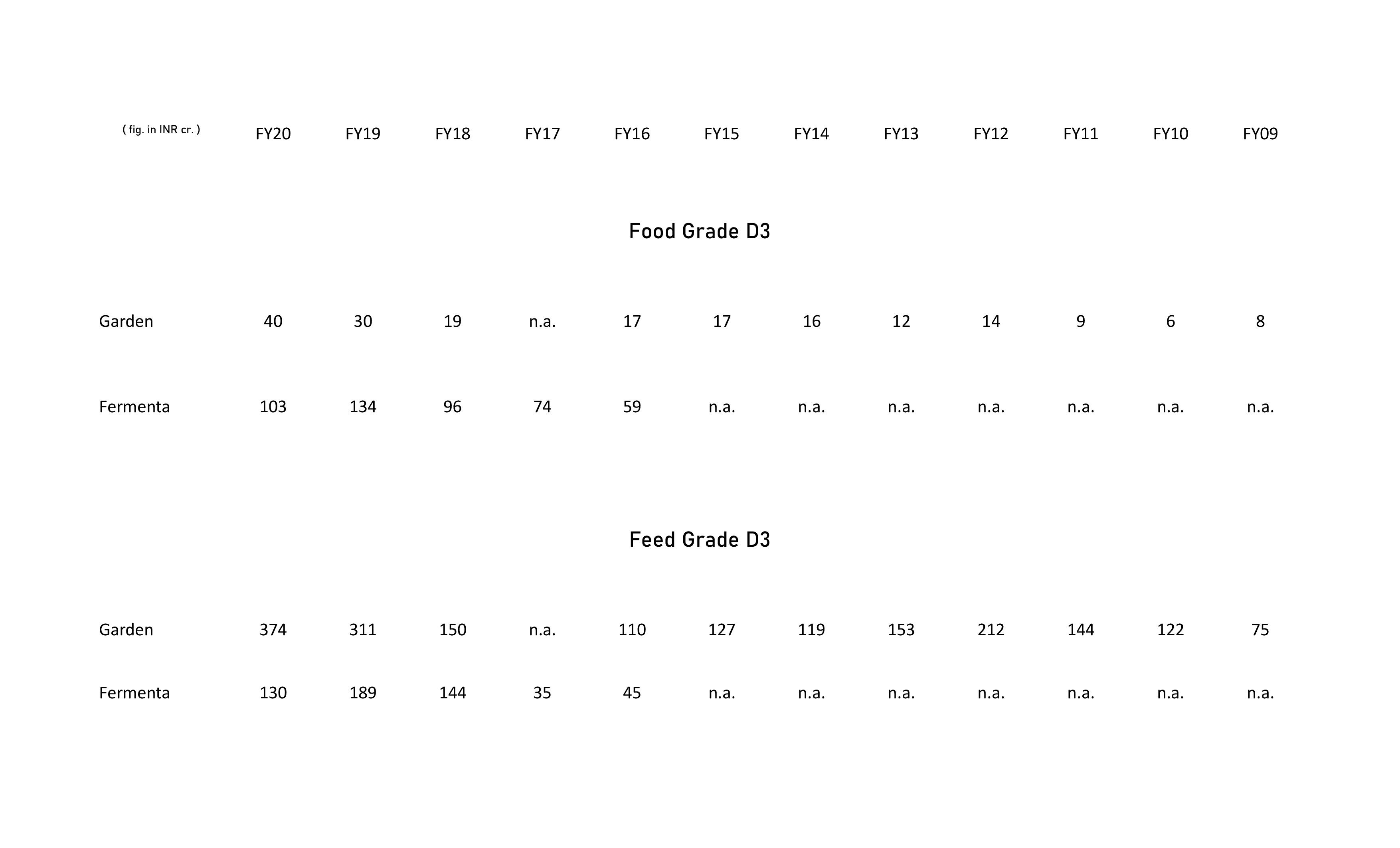

(Respective separate Feed & Food grade Vitamin D3 revenue comparison between both the companies is provided later.)

Starting from FY13 till FY18, Fermenta seems to have gained marketshare to become the second/third largest player in Vitamin D3 market (excluding DSM). From FY19 onwards Zhejiang Garden seems to be growing relatively aggressively. There might be three reasons for this :

– Zhejiang Garden seems to have cut on pricing as its costs are amongst world’s lowest,

– CEP certification for its product in March 2019 which might enable it to push Food Grade (Human) D3 sales aggressively in western markets. Fermenta got CEP certification in early FY17,

– Introduction of 25 hydroxyvitamin D in FY18.

FY21 seems to be crucial for Fermenta with regards to regaining of lost market share or atleast maintaining market share, especially in Food Grade Vitamin D3 space where, from the beginning it was very strong :

However, still Fermenta seems to be holding on to its second/third largest player status as Taizhou Haisheng which seems to be the second/third largest Vitamin D3 player in China after Zhejiang Garden is at INR 181 cr. in CY19 (FY20) while if we consider overall product mix of Carbogen Amcis BV (Dishman), which also is a major player in NF grade cholesterol, Fermenta seems to be bigger than both.