In results, Auditor qualification needs to be noted :

as also new capacities coming up with an investment of ~INR 1100 cr. of Zhejiang Garden Bio in 2HFY21 and its impact on pricing need to be monitored.

In results, Auditor qualification needs to be noted :

as also new capacities coming up with an investment of ~INR 1100 cr. of Zhejiang Garden Bio in 2HFY21 and its impact on pricing need to be monitored.

I noticed 5 things in their investor presentation.

Whereas company is interesting and into its own niche, we need to accept the fact that it is majorly still an SME style management with average corporate governance standards. This might not be intentional but comes with the working style itself. So, these issues that we see like ICDs to associate, investment into non-related businesses, significant amount ICD to another corporate, etc. will be a routine thing.

However, positive thing is that from the beginning, spanning over last 2 decades, , because of its connection with an MNC, we have a credible big auditor for the company – previously it was SR Batliboi and now we have Deloitte. This is a rarity in such companies. Another thing is that I don’t find the promoters to be fly-by-night type and they don’t seem to involved in any fraud or something – the company is being promoted by one of the son of the founder of Biological E – one of India’s prominent vaccine developer and manufacturer.

You can refer following flowchart for your query – company might start using wool grease as RM now as against Cholesterol which was previously used as RM –

Now, here, EC for this backward integration was obtained in 2015 in Dahej plant but whether Cholesterol manufacturing is started or not and if not then why it has not started that is to be seen.

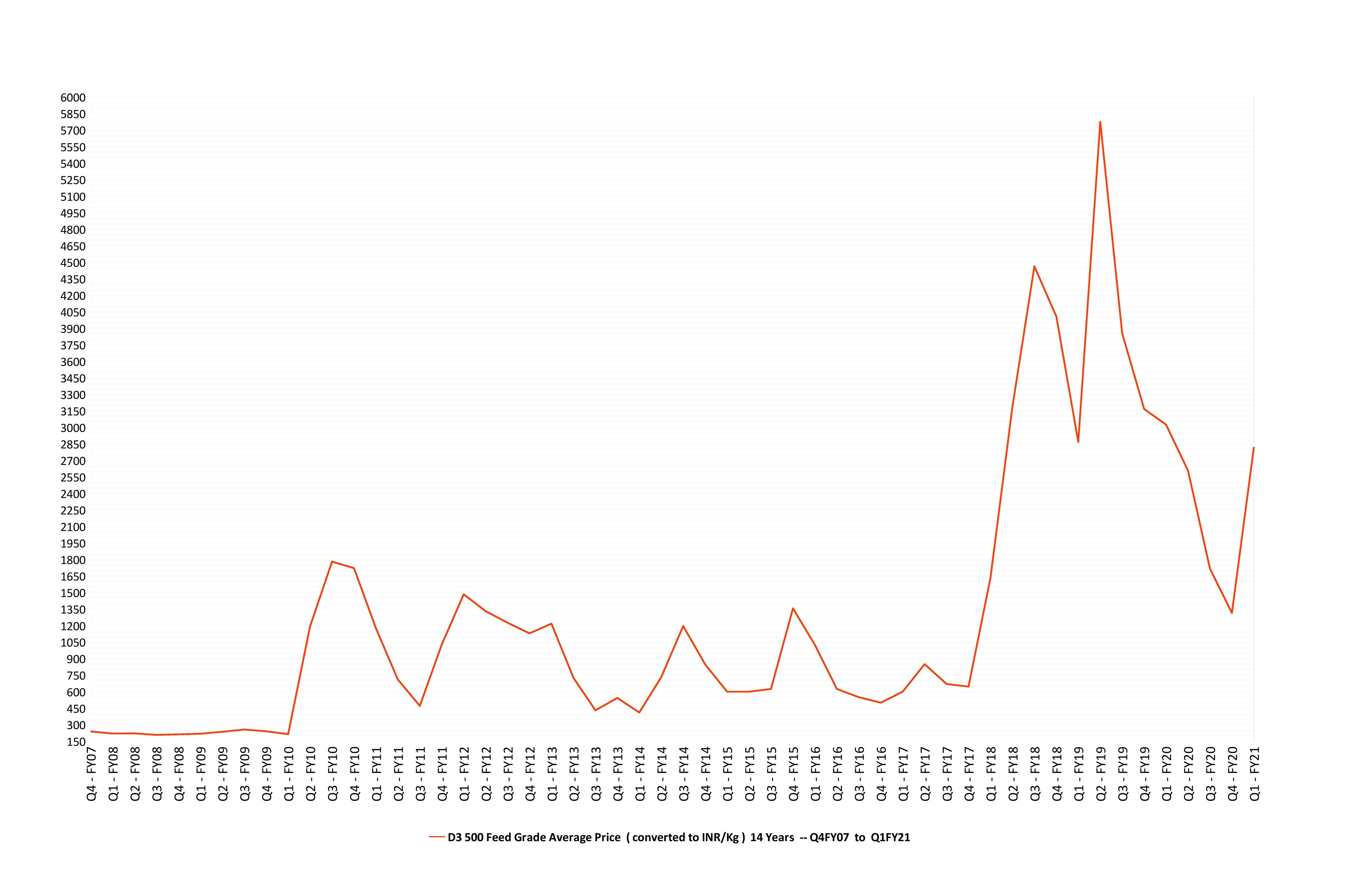

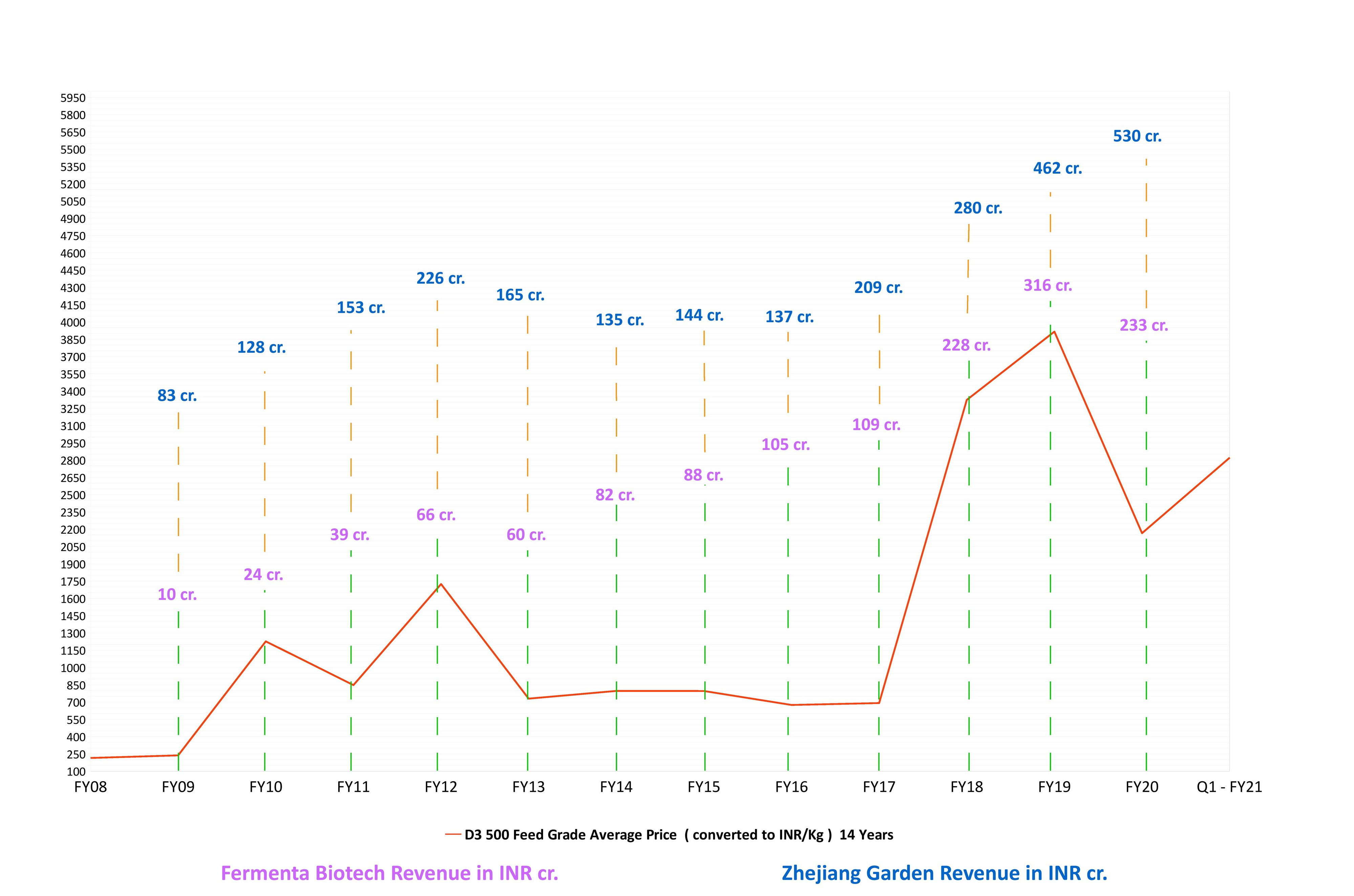

Company’s 48 % of the overall revenue and 56 % of Vitamin D3 revenue comes from Feed Grade Vitamin D3. For your query, you can refer last 14 years’ quarterly average price chart of Feed Grade Vitamin D3 given below. Q4FY20 price of the product was down ~45 % over Q4FY19 :

In addition to this, one can refer yearly average price chart of Feed Grade Vitamin D3 to understand the nature of the industry :

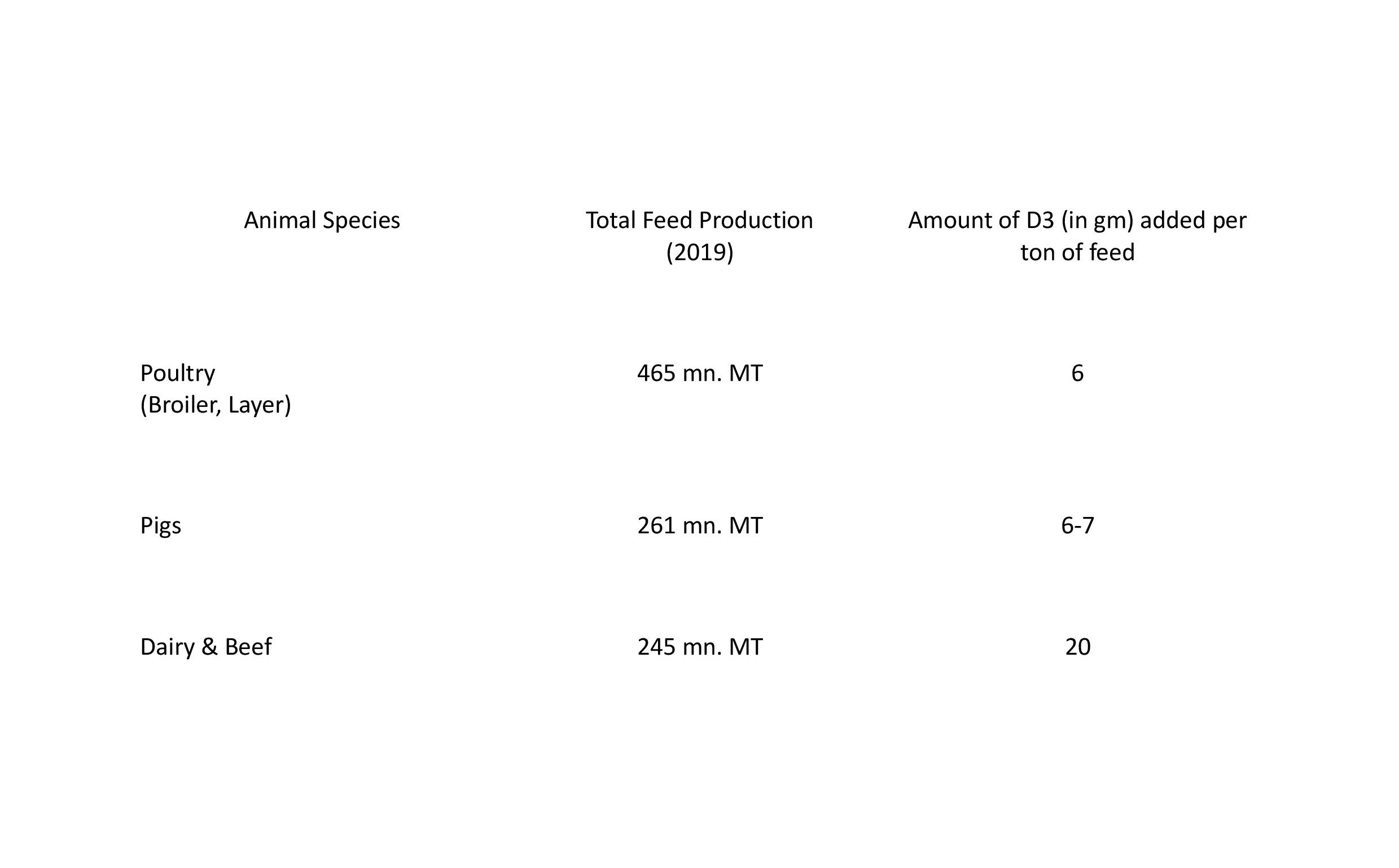

Feed Grade Vitamin D3 constitutes 70 % + of the industry demand. Vitamins are used as nutritional additives in animal feed as they play a vital role in maintaining normal immune function of livestock and poultry. Modern farming conditions devoid animals of natural conditions like sunlight, soil and green feed. Nutritional additives in the form of vitamins and minerals are therefore needed the most. Below is the recommended addition of Vitamin D3 in the feed of some animal species :

2019 Total Global Feed production is estimated at 1126.5 mn. MT p.a. On an average it is estimated that about 6-7 gm of vitamin D3 needs to be added for every 1 ton of feed which puts theoretical demand for feed grade Vitamin D3 at ~6750 MT p.a.. However, it is called ‘theoretical’ demand only as historically it is being observed that feed manufacturers adjust the quantity of feed additves added w.r.t. price change of feed additves. Because of this, although Vitamin D3 constitutes below 1 % of feed cost, yet demand is largely dependent on the price of vitamin D3 – when the price is low, demand is high whereas when the price is high, feed manufacturers adjust the quantity added and therefore volume of D3 sold actually decreases. This is the reason why Zhejiang Garden Biochemical, which is world’s largest player in Vitamin D3 market, sold 1942 MT of feed grade Vitamin D3 powder in CY2008 when its price was INR 238 per Kg whereas in CY2018, when price of Vitamin D3 skyrocketed to INR 4126 per Kg, it sold only 856 MT which doubled to 1775 MT in CY2019 when price halved to INR 2600 per Kg.

It is interesting to note here Zhejiang Garden Biochemical’s yearly sales volume in MT of Vitamin D3 Feed Grade Powder over last decade :

Green line in the chart above depicts the volume of feed grade vitamin D3 powder sold by Garden Bio each fiscal, which we can observe has largely remained in a range and fluctuated based on price of the product.

On supply side also same thing is there – when the prices skyrocket, existing players aggressively expand their capacities as also players who had exited in past but have idle capacity come in ; when the prices plunge weak players exit because of losses and market price makes a trough. When we look at last 13 years price data of feed grade Vitamin D3 the same thing can be observed – In April 2009 prices plummeted to a record low of then decade to touch INR 218 per kg (even in 2001 it was INR 575 per kg) post which it recovered to touch a high of INR 1990 per kg in Feb2010 after which it again went down gradually to hover around INR 600-700 from FY13 to FY17. Then, from FY18 it has had a sharp rise to touch INR 6100 per kg in August 2018 post which it has fallen down again to touch INR 1200 per kg in Feb2020 to recover to INR 1900 per kg in June2020.

To cite here an example, as against theoretical demand of feed grade Vitamin D3 of ~7000 MT p.a., we have ~8500 MT p.a. production capacity distributed amongst just 5 major chinese companies – Zhejiang Garden Biochemical, Zhejiang Xinhecheng, Taizhou Haisheng, Xiamen Jindawei and Zhejiang Pharmaceuticals. Here, we are not considering few small chinese companies who have small capacities to produce feed grade Vitamin D3. Also, we have not considered here the production capacities of DSM.

Hence, what we actually have is ~11500-12500 MT p.a global production capacity for production of Vitamin D3 (Feed+Food grades) as against global theoretical demand of ~10,000 MT p.a. (Feed+Food grade combine).

Over the course of next few years we need to observe the price trend as – first – feed producers themselves are under pressure because of worldwide corona pandemic – and second – new capacities of Vitamin D3 are coming up in china – majorly in CY21.

If we talk specifically for Fermenta’s feed grade market –— China, which contributes ~18 % to global feed production, is out of its reach as chinese producers themselves will be addressing that market. India, which majorly produces dairy and poultry feed and contributes ~4 % to global feed production – this might be simpler to address for the company. USA & Europe market which forms more than 40 % of global feed market are where company can focus on and compete with chinese players especially, Zhejiang Garden, which can compete aggressively on pricing. USA-China Tariff wars have still not touched this product and there has been no effect on chinese company’s sales due to that.

It is interesting to observe Zhejiang Garden Vitamin D3 (combine – Animal & Human) sales vis-a-vis Fermenta’s Vitamin D3 sales (combine – Animal & Human) over last many years in the backdrop of Feed Grade Vitamin D3 pricing :

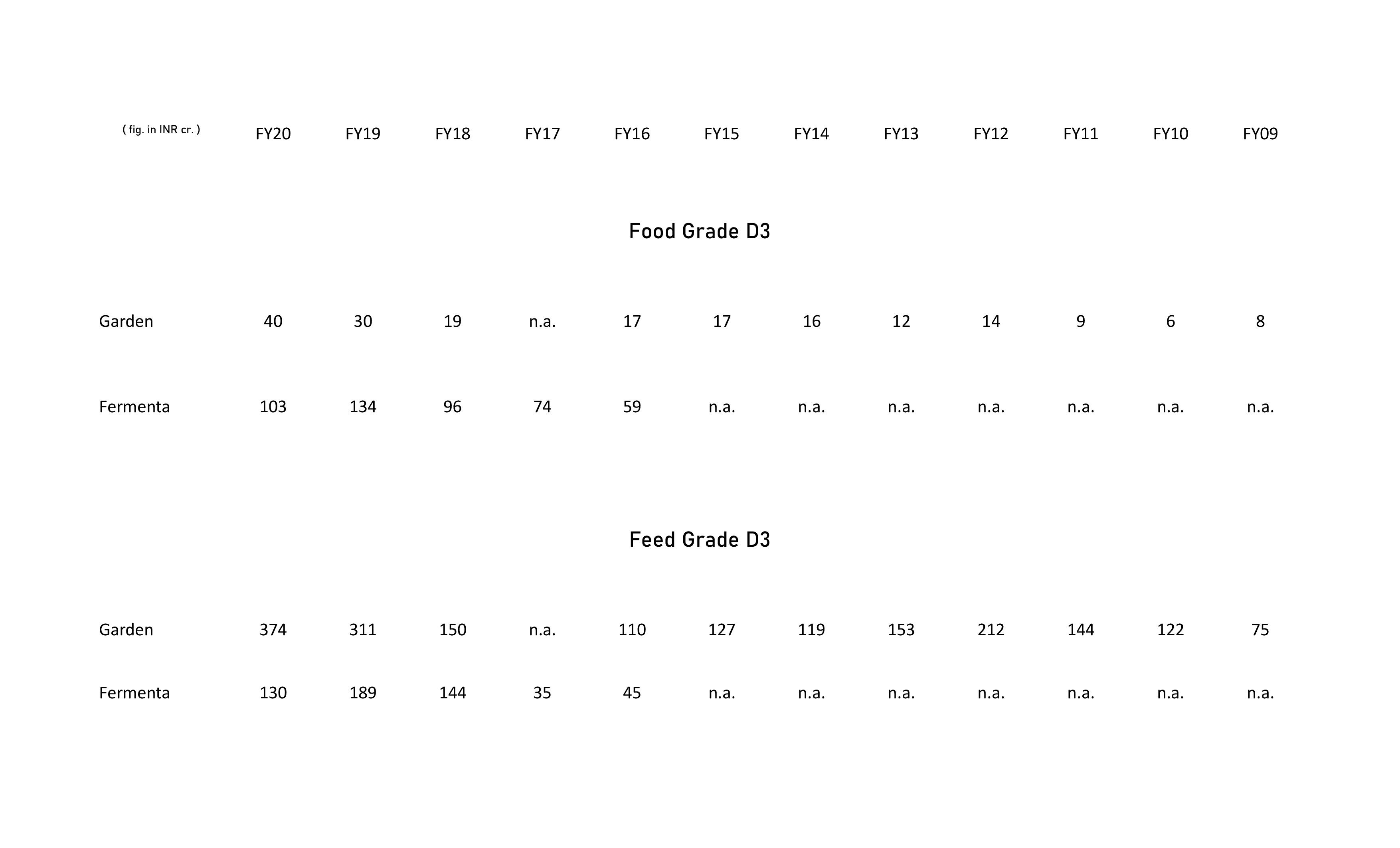

(Respective separate Feed & Food grade Vitamin D3 revenue comparison between both the companies is provided later.)

Starting from FY13 till FY18, Fermenta seems to have gained marketshare to become the second/third largest player in Vitamin D3 market (excluding DSM). From FY19 onwards Zhejiang Garden seems to be growing relatively aggressively. There might be three reasons for this :

– Zhejiang Garden seems to have cut on pricing as its costs are amongst world’s lowest,

– CEP certification for its product in March 2019 which might enable it to push Food Grade (Human) D3 sales aggressively in western markets. Fermenta got CEP certification in early FY17,

– Introduction of 25 hydroxyvitamin D in FY18.

FY21 seems to be crucial for Fermenta with regards to regaining of lost market share or atleast maintaining market share, especially in Food Grade Vitamin D3 space where, from the beginning it was very strong :

However, still Fermenta seems to be holding on to its second/third largest player status as Taizhou Haisheng which seems to be the second/third largest Vitamin D3 player in China after Zhejiang Garden is at INR 181 cr. in CY19 (FY20) while if we consider overall product mix of Carbogen Amcis BV (Dishman), which also is a major player in NF grade cholesterol, Fermenta seems to be bigger than both.

Fermenta’s future strategy for expansion also seems to be interesting wherein at the cost of just INR 60 cr. (4 cr. for Kullu and 56 cr. for Dahej), by just tweaking the product mix, company seems to be adding :

– 81 % additional capacity to its Food Grade (Human) Vitamin D3 products,

– 12 % additional capacity to its Feed Grade (Animal) Vitamin D3 products,

– 42 % additional capacity for backward integration for RM of D3,

– 55 % additional capacity in Lanolin derivatives which are by-products of backward integration project and might generate an additional revenue stream for the company because of their use in cosmetic industry.

Hence, optically this brownfield expansion at two plants, viz., Dahej and Kullu seems to be adding only 19.75 % to the existing combined capacities from 6708 MT to 8033 MT p.a., but, when we look in detail, by phasing out 11 % capacities of non-D3 related products, company is getting much stronger in D3 segment :

Here, we are not considering greenfield project at Saykha, Gujarat, which when implemented fully, will triple company’s Food Grade (Human) D3 capacity, will more than triple company’s RM (for D3) processing capacity, will enable a 50 % rise in its Feed Grade (Animals) D3 capacity and above all mark its entry in high end 25 Hydroxyvitamin D3 segment.

Regarding other nutritional products like Vitamin K, Minerals, etc., its foundation is getting built and for them making a meaningful impact seems to be some years away.

Historical Fiancials :

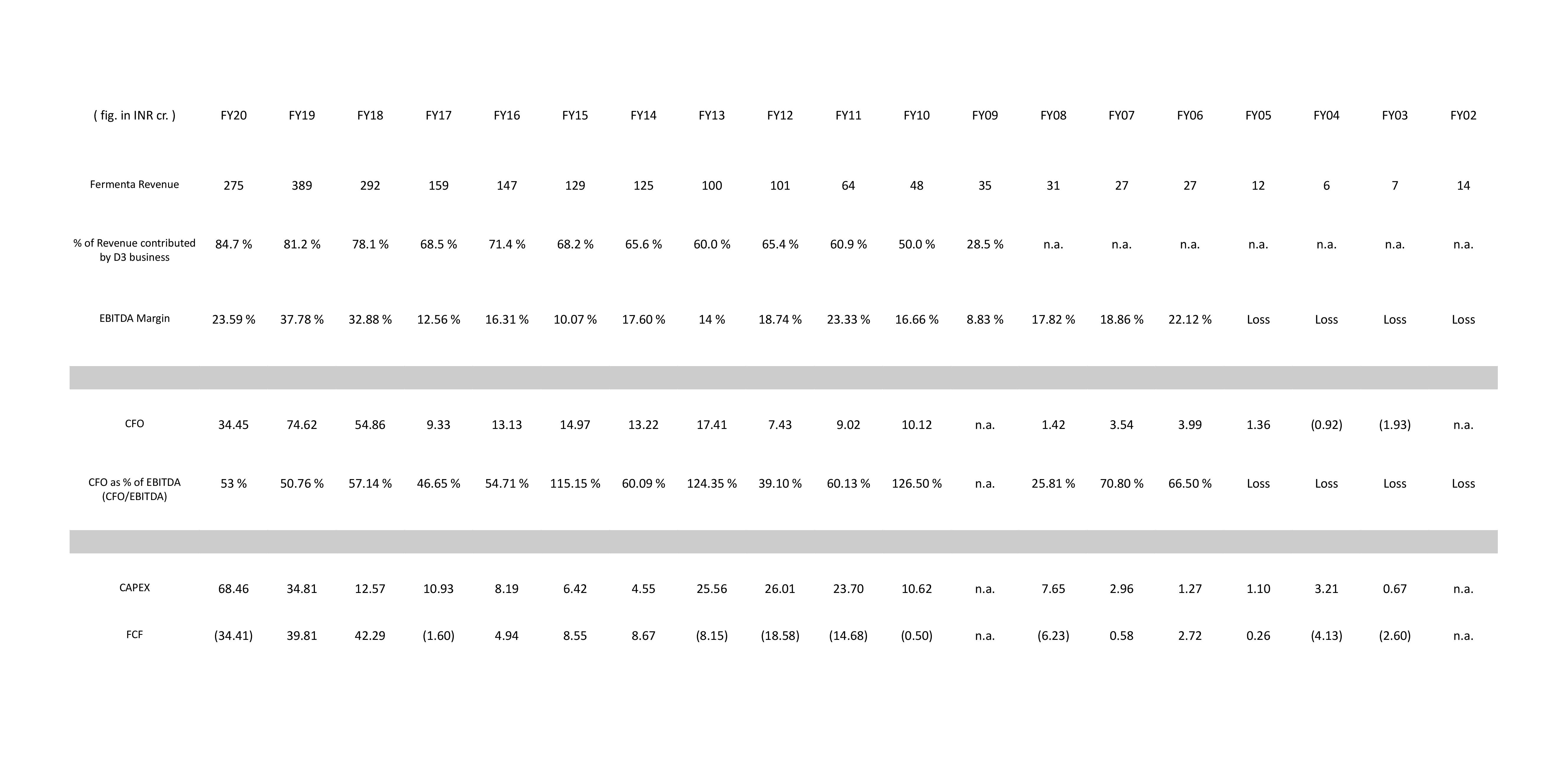

If we look at historical financials of Fermenta as a standalone entity, it seems a steady-state EBITDA margin of 16-20 % is what we can assume for the company and FY18 and FY19 margins of 30 % + that we see might be one off because of significant product price increase. CFO has been healthy at average 50 % + of EBITDA :

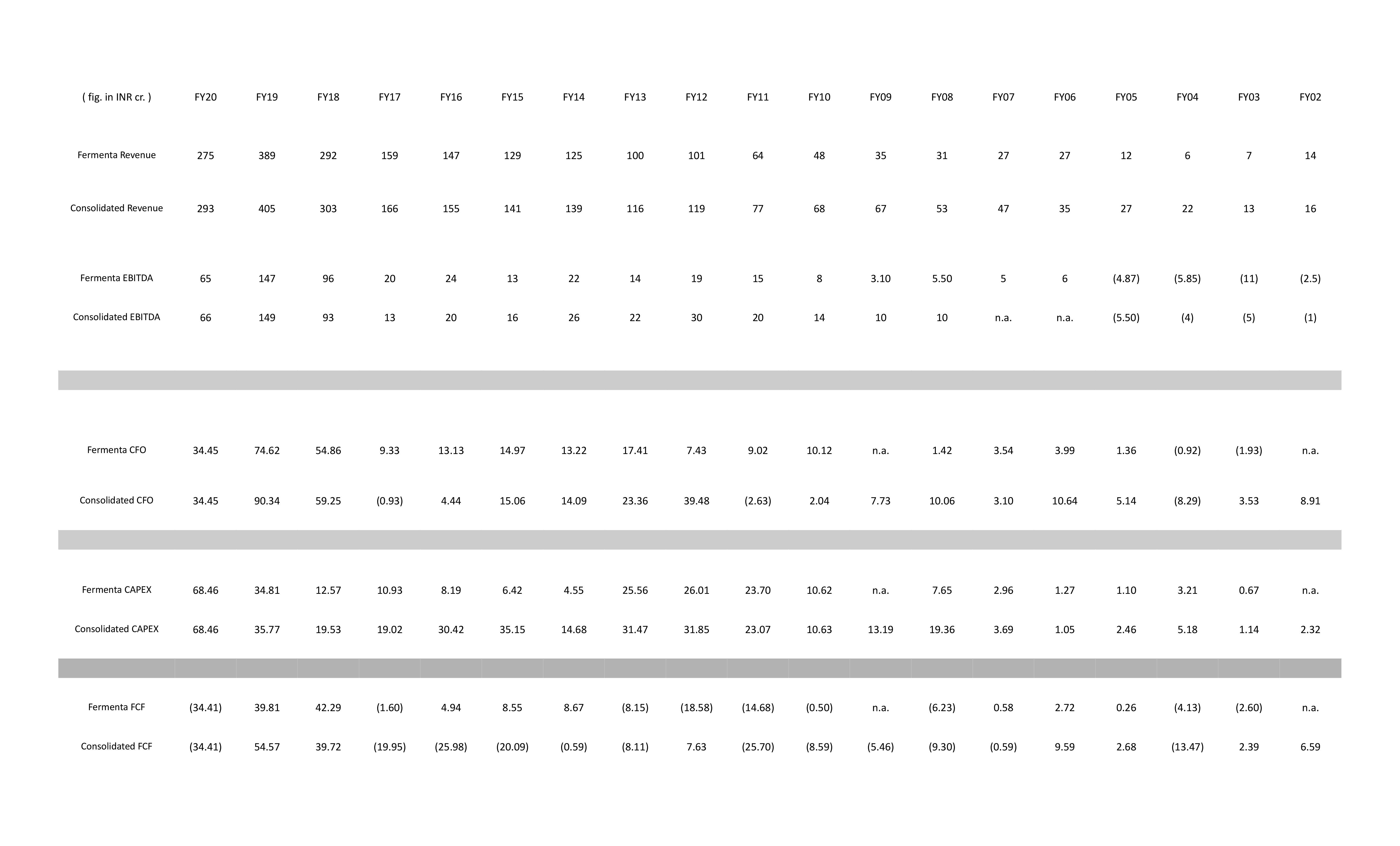

However, when we look at consolidated financials, the picture is different. Till the treasury income was generated, it was ok and actually its this treasury income which helped Fermenta to fund a greenfield project at Dahej but post that management’s venture into real estate and other things marred the entire picture :

It is good that management has merged Fermenta into listed DIL and trying to exit all other ventures. However, monetising real estate might be difficult now, especially after recent pandemic. Value of real estate holdings was most probably INR 300 cr. + before this pandemic ; however, value on paper actually means nothing till its practically realised. If Company is serious for monetisation, it might have to look at indirect monetisation of its assets wherein ownership is retained by the company itself but its management is given to someone else wherein company itself doesn’t enjoy the fruits of its holdings (which come in the form of rent, etc.) and transfer the property for a lumpsum amount for many years.

In any case, we seem to be somewhere near the 3rd or the 4th step (of 10 steps) of the lifecycle of wealth creation as company is interestingly placed in its operating segment, operating segment itself is quite promising, business can generate steady cash flows and on the other side still NSE listing is not done, Funds & PMS don’t have significant holding in this company, no equity fund raising is done yet at listed entity level despite INR 300 cr. + CAPEX lined up over next 4-5 years.

Key monitorables are scalability with reasonable margin, timely completion of projects, cash flow generation, monetisation of real estate assets and most significant is the management keeping its word of now on, no other ventures or focus other than Fermenta’s core business.

Discl. - Invested

[This should in no way be considered as any buy/sell recommendation of any kind. Here, only statistical facts and figures are provided which can only be used as starting point for further study of Vitamin D3 segment and its key players. This, and two posts immediately before this post in this thread, are part of general discussion and provide statistical facts and figures only for further study. No one should consider these as any kind of recommendation of any kind whatsoever.]

||||||||||||

Update as on 9th August 2020 :

Zhejiang Garden has last week raised INR ~975 cr. (as against its CY19 topline of INR 730 cr.) via equity issuance at 8.04xEV/Sales (TTM), 14.49xEV/EBITDA (TTM) and 17.61xEPS (TTM). There was widespread institutional interest and majority bids came at 25 % above the floor price.

Hi Maheshji,

Great analysis. Had some questions. U said fermenta’s competitor has raised 975 cr ; what u think will be the effect of such fund raising on industry capacities and vitamin d price ? What is the current status of vitamin d price ? U have said supply exceeds demand then what makes vitamin d price rise so significantly ?

Thanks in advance

Disclosure - Invested recently at average holding price of 320

With rgds to your first query, out of 975 cr raised, majority of the funds (55 %) are meant for expanding RM capabilities…Garden is the only company in china and one of the only 3 companies in the world which can mass manufacture lanolin-based NF cholesterol and new standards implemented by Chinese government ban the use of any other source derived cholesterol for D3 manufacture other than lanolin-based cholesterol starting from 1st July 2020 (US and Europe have already banned the same). Hence, with current expansion, supplying RM is also a goal for the company…

Theoretically, with current expansion, Garden is expanding its feed grade D3 capacities by 70 % and almost doubling its capacities for food grade D3. Other funds are going for expansion of 25-hydroxyvitamin D3 capacities which only two companies in the world can manufacture in large quantities - DSM and Garden. However, because of Environmental issues, one of the plants are going to close down and company is planning to shift production from 2nd plant to current greenfield plant because of logistical benefits – hence, post this expansion what will be actual expansion in Feed and Food grade capacities will need to be seen over the course of next few years.

In any case, when a company who is leader in an industry (more than 35 % marketshare) is expanding by deploying funds more than its current topline (topline with product prices at near historical high), we need to monitor the trend closely. Secondly there are couple of other manufacturers in China who are expanding their D3 capacities – by CY21 the picture will be clear and we will be able to gauge effect of all such expansions on D3 pricing. Important thing to note here is that all these majorly relates to only feed grade D3 price as China is controlling 85 % of the world capacities for feed grade D3.

Q1FY21 avg feed grade D3 price has been ~2821 INR vs 3025 INR per kg of Q1FY20. On 10th August 2020, Garden seems to have doubled its product quotation for export to INR 5400 per kg ; however, pricing in the market is wide between 1500 to 4500 INR per kg. Some chinese manufacturers have announced maintenance closure for 1-1.5 months till September 2020 and demand is expected to be strong from now on as customers are willing to cover their demand till Q1CY21. All depends on pricing and let’s see how the trend goes.

Chinese companies control ~85 % of global production capacities for feed grade VD3. When price goes low they withdraw supply from the markets and therefore create scarcity thereby compelling prices to go up significantly. Then they come with supply thereby stabilising price and making it to go down. Except Garden, almost all other manufacturers have significant capacities for other vitamins too other than VD3 and VD3 forms only a small portion of their overall sales mix. In contrast, food grade VD3 prices are relatively stable and devoid of wild fluctuation that are observed in feed grade VD3 prices. However, feed industry constitutes more than 80 % of VD3 demand with food and medicine segments contributing the rest.

Rgds.

Discl. - Invested

Thanks a lot Mahesh for such detailed reply.

Regards

Dhrumesh

Hello Mahesh,

Great job, keep the detailed analysis ,this is helping all of us!!!

Could please comment on the pricing for Vitamin D3 for human? Hows that in Q1 FY21 vs Q1 FY20 and also as on today.

Also, with respect to Fermenta, we hope it will be able to cope up with the upcoming situations (any dirty play by Chinese) and compete well, considering they are almost backward integrated for their raw materials.

How do you see the potential of “Multi-Vitamins” and any update if Fermenta has already started producing/selling it?

Hope overall future potential is looking good for Fermenta with growth hungry management.

Thanks

Hafizul

Disc - invested

Food grade VD3 price is still not available for Q1FY21…however, in Q4FY20, it was relatively stable at INR ~1790 per kg vs Q4FY19’s INR ~1855 per kg…this is against feed grade VD3’s significant price fall to INR ~1400 per kg in Q4FY20 vs INR ~3100 per kg of Q4FY19.

To add, Food Grade VD3 prices were stable at INR ~890 per kg even when feed grade VD3 made its historical low of INR ~230 per kg in FY08 and over the period of FY08-FY17 when feed grade VD3 prices fluctuated wildly between INR 230-1300 per kg, food grade VD3 prices were devoid of such wild fluctuations and remained stable at INR 1200-1400 per kg.

They are competing with chinese companies since beginning…however, chinese companies focus has been on feed grade VD3 ; and if we run an approximate price derived volume check then it seems Fermenta food and feed grade VD3 volumes seem to be almost 50:50…We need to monitor Garden’s food grade VD3 focus post CEP certification in 2019…Unless there is some global general restrictions on all chinese products, chinese dominance on feed grade VD3 market seem hard to compete by any player…what Fermenta could do is continue its focus on Food grade VD3 and succesfuly venture into 25 hydroxy VD3 for which there is still not much competition…

Saykha plant has not started yet…Fermenta’s venture into overall Nutraceutical segment by expanding its production to other vitamins and minerals need to be monitored closely…however, in any case it is some years away as Saykha plant is going to be commissioned in 3 phases spanning over 5-7 years. So, to bet on this venture at this stage will not be logical for an investor thats what i feel.

Discl. - Invested

How does one track these vitamin prices?

( Disclosure not invested)

best way is to subscribe to some feedinfo service like Vitamins China E-news or boyar.cn…otherwise look for web searches to track prices.

Rgds.

Thanks a lot Mahesh!!!

Looking at the Investor presentation, it looks like Multi-vitamin will be launched by Q3 FY21…is it not correct or I am missing something?

FBL management keeps saying they are the only producer of VD3 in India - but Dishman Carbogen(DCAL) also does that I think…can u pls clarify the fact here----is it like FBL is the only producer of APIs of VD3 in India? and others are formulations players, who buy from FBL?

Overall, can u pls summarize the potential of FBL for next few years, keeping in mind the increased demand growth due to increased awareness among people, more so after the Covid-19 incident?

Do you see any risk? I did not see management getting involved in any fraud in past, although they had ICDs which is qualified by Deloitte in Audit report. Does management has to capability to capitalize on the opportunity of demand growth and take the company to the next level?

I think, there is entry barrier to this business , considering niche technology and long gestation period, and thats the reason we have 3-4 players in the world, please correct me or add more. is there any risk like say some bug players like Divis or DRL or Auro comes to this business and destroys small players like FBL?

Thanks in advance, sorry for too many queries.

Disc - invested

Whether management can walk the talk that needs to be seen. One thing we need to understand that in presentations of such SME-type companies there will be lots of boasting but when it comes to actual realty, things might be different. Rather than focussing on Fermenta’s other ventures like Vitamins other than D3 as well as minerals, it is better to concentrate on positioning of Fermenta in VD3 market and its potential thereon ; other ventures if and when starts and successful could be an added bonus.

DIshman’s netherlands subsidiary is majorly involved in D3 business ; hence, Fermenta management says that they are the only manufacturer of VD3 in India.

Have already posted all the facts and figures so far in this thread…to analyse and judge the potential of a company and an industry ; that work each individual can best do as from which angle I analyse the company and industry, there might be other people who analyse the company and industry differently and have their own calculations which might be right. So, it is best for an individual to study each company and industry well and build his/her own conviction.

As far as I am concerned, I am not betting on significant demand rise in VD3 because of just Covid…Its the positioning of Fermenta in the industry and its venture into 25 hydroxyvitamin D3 that seems interesting to me.

So far management has done well. It is not as professional and with deep knowledge as Garden, but it has not let its position in VD3 industry getting loose. I don’t see many players emerging in this industry so that itself is a positive sign. How management executes future expansions, especially in 25 Hydroxy that needs to be monitored closely.

Small industry size itself is a major entry barrier, I don’t see big players you mentioned entering into manufacturing of this product. There are overall 10-12 players in the industry – majorly concentrated in China and not 3-4 as you have put out. Out of them, ~7 are active and others are passive with capacity to manufacture, especially feed grade VD3.

Rgds.

Discl. - Invested

Thanks Mahesh, appreciate your detailed inputs on all queries.

I hope promoter takes appropriate steps - list on NSE, sell off real estate and use the funds for expansion of core Vitamin, Nutraceuticals business and convert the opportunity/demand of the industry into revenue/profit/ improve return ratios.

Overall, I am pretty optimistic about the prospects of this company, this is small in size but company has the plan to exploit the opportunity , sustain, grow in such a niche area with higher entry barrier (moat). They planned to have 1000 crore revenues in next 5-7 years, which they can do ahead of time with the Nutraceutical industry estimated to grow at 20% in India, as per Deloitte market research.

Disc- invested.

Hi Mahesh,

Thanks for sharing your deep insights on the company. What is the source of your insights around the average realizations that the company has been getting in food and feed segment? and how can one track these?

Don’t you think the pricing is too volatile for comfort and hence its really tough to put some value to the company?

Having invested in this stock earlier and later exited, one thing i realized - its super tough to keep up with price changes. Markets are always ahead of you. and when prices are good, the information is pushed out while the bad news comes only when things are down under. And if one is not aware of the same or can’t handle the wild volatility/swings, one will panic at wrong times and can incur big losses.

You mean to say Zhejiang Garden Food and Feed segment average realisations right…They are taken from Annual Reports of Zhejiang Garden, its two IPO prospectus. post IPO equity placement documents, Covid-19 impact announcement filed by the company with stock exchange, etc.

If you want to track the pricing, food grade VD3 price tracking on a continuous basis is difficult and for that you need to have a constant vigil on industry articles from varied sources like Vitamins China E news, feednavigator, boyar, chinese companies announcements, etc. or need to have paid subscription service to feed and food additive news sources. Feed grade price tracking on a continuous basis is relatively easy wherein China is a major vitamin supplier around the world and in varied articles on chinese financial websites regarding chinese listed vitamin companies, pricing and all of all vitamins are given almost every month…alternatively u can also refer feed additive websites like china feed onilne or Vitamin Today on Wechat…

Most authentic source I have found is filings of companies.

You are right to an extent Ayush but you yourself being a veteran in stock markets as also an avid company researcher, you very well know which mid- or small- cap companies’ business is devoid of volatility ![]() we need to keep constant vigil on their business and assign worst case scenario value in best phase and best case scenario value in worst phase ; just as we have to do in cyclical stocks…

we need to keep constant vigil on their business and assign worst case scenario value in best phase and best case scenario value in worst phase ; just as we have to do in cyclical stocks…

I will tell you my understanding and my thesis and you see if you can extract something out of that…

what attracts me here is the positioning of the company in an industry which is unlikely to have major competition in foreseeable future…As you must have seen in my posts above in this thread, there are just handful of companies outside China which are into this business – DSM, Dishman and Fermenta are major out of them – all other companies with 85 % of global capacity are concentrated in China – and here we have this company Fermenta whose VD3 business sales is 44 % of Zhejiang Garden VD3 business sales with Zhejiang Garden largest player in the world controlling 40 % + marketshare of the industry…and this relative size is up from just 12 % of 2009 to 44 % in 2020. So, if Zhejiang Garden is controlling 40 % marketshare then Fermenta is deemed to control 15 % + global marketshare of the industry…

Secondly company’s moves are in right direction — major future expansion in RM, Food Grade and 25 hydroxy – just to cite here an example, DSM is pushing hard to replace use of feed grade VD3 (D3 500) with 25 hydroxyVD3…as on date, only two companies in the world can manufacture 25 hydroxy in meaningful quantities – one is DSM and other is Zhejiang Garden (also Dishman to an extent, but not sure of its capacities) ---- Zhejiang Garden started manufacturing 25 hydroxyvitamin D3 in CY16 and in CY19, DSM signed a long term 10 years agreement with Zhejiang Garden to exclusively sell its entire output of 25 hydroxy at a fixed price to DSM…price of 25 hydroxy is ~INR 5 Lakh per kg and is stable at this level since many years…

Now, my assessment is once Fermenta starts manufacturing 25 hydroxyvitamin D3 and in case it is successful to produce it in meaningful quantity, it might be able to find a ready market for its product – since DSM has locked the price of the product under long term contract, 25 hydroxy might be able to give a great stability to Fermenta financials…its worthwhile to note here that out of INR 530 cr VD3 business revenue of Zhejiang Garden, 117 cr is contributed by 25 hydroxyvitamin D3…also, there are not many companies attempting to produce this product – only one other company in china is attempting to produce this product which means this product is unlikely to have major competition in the times to come…

Now, coming to the main point of valuing the company – what i did is valued this company on steady-state basis with valuation multiples of Zhejiang Garden public issuances taken as minimum…Fermenta has always remained a 50:50 company as far as Food:Feed grades VD3 sales are concerned — we have precise realisation data from Zhejiang Garden ARs and prospectuses about Food Grade VD3 from CY07 to CY16 as well as latest of Q1CY20…Food Grade VD3 price has seldom dropped below INR 1000 per kg and has always remained in the range of INR 1200-1800 per kg (this is when Feed Grade VD3 prices were majorly in the range of INR 230-700 with for a brief while going above 900 to touch 1200 per kg)… in Q1CY19 and Q1CY20 also price of Food Grade VD3 is rock steady at ~INR 1800 per kg…

so, if we assume INR 1500 kg to be steady-state Food Grade VD3 price and take into consideration just expansion at Dahej and Kullu (80 % additional capacities for food grade VD3), then on a steady-state basis company’s food grade VD3 sales can be assumed at a minimum INR 135 cr. p.a…

Now, Feed grade VD3 prices have fluctuated wildly between INR 230-5000 per kg…hence, we will assume just INR 1000 per kg (as against current price of ~INR 2200 per kg) product pricing for that which gives us 70 cr p.a. from Feed grade sales on a steady-state basis…

Hence, from FY22 onwards, we can have VD3 business of Fermenta turning out minimum INR 205 cr, revenue on a steady-state basis…

If we analyse other products of Fermenta like Enzymes, Phenyramidol, etc. over last 10 fiscals, they have turned out a minimum revenue of 45-55 cr. each fiscal …hence we will assume 50 cr. to be the sales of other products on a steady-state basis…

this brings us to total revenue of Fermenta from FY22 onwards to be at minimum 255 cr. p.a…

Here, if we assume an EBITDA margin of just 20 % on a steady-state basis then it will turn out an EBITDA of minimum 51 cr. on a steady-state basis…

Zhejiang Garden issuance has never happened below 14.5 EV/EBITDA (here we are ignoring other multiples which are on a higher side like EV/Sales at minimum 4 and maximum 18)…

Taking 14.5 ev/ebitda as base – we have minimum EV of 740 cr. for Fermenta —add to this minimum 150 cr. discounted property value (60 %+ discount to pre-covid property rates) which takes us to minimum EV of 890 cr or a market price of INR 250 per share…

This is how I assigned value to this company when I entered this stock…here, Saykha project contribution, if any would be a plus and success of 25 hydroxyvitamin D3 venture would be a bonus…not to mention here, prices of feed and food grade VD3 which we have assumed very low and even currently ruling at double our assumed price (feed grade)…

In addition, if company can extract any long term contract for any of its product like 25 hydroxyvitamin D3 as Zhejiang Garden was able to with DSM then it might catapult Fermenta into the big league straightaway…

Now, a company which carries so much potential and is still trading near to its minimum value deserved attention ; this is how i entered this stock…I lost on the opportunity to buy it much lower like you because it took me many months to extract all data and have a grip on the industry structure…once i was convinced then only i entered this stock…

still, i must say i have not gone overboard on this company as far as allocation is concerned…this is because it carries certain genuine risks…

There are 4 risks that concern me…first is the aggressive capacity expansions of chinese companies which will come into production next year…how much is that because of relocation that we will be able to know only in subsequent years…

second is Zhejiang Garden’s CEP certification and rising food grade sales — Fermenta’s strength is food grade VD3 that we shouldn’t forget…

third risk is company’s real estate monetisation seriousness…although management has said many times, but unless this actually happens we have to be vigilant…here i would also like to mention that i feel if entire assets are monetised, this company might find many investors getting attracted to it which could drive its rerating…

fourth risk i see is working style of management which lacks high corporate governance standards…although this comes alongwith any sme-style investment but if one wants to see this company trade at premium multiples, this thing has to improve…just to cite here recent examples , ICD given , moratorium taken, extention window used for declaration of Q1FY21 results, etc. are what i am pointing to.

You are right…if an investor is going to panic by seeing significant downturn in stock he should never enter this stock…if downturn is because of wild fluctuation in product pricing an investor should never get perturbed atall…if downturn is because of management blunder of loosing its positioning in the industry then an investor needs to get extremely concerned…however, it will require a very foolish management to loose the advantage and positioning that the company enjoys currently in global VD3 market…

Tracking of pricing is not that difficult as I explained you previously in this post,atleast weekly or fortnightly we can easily track the prices…food grade VD3 price is relatively stable so what we need to check is only feed grade VD3 pricing and its actually feed industry only where 80 % of global VD3 demand is afterall…

Question is what is our goal of entry into this company ?? Is it to take short term advantage of high product prices and therefore good short term cash flows…if it is this goal then investment here seems very risky to me as an investor will immediately panic if Feed grade VD3 prices fall to INR 1000 per kg from current INR 2200 per kg…

If our goal is to have a nutraceutical company in pf which enjoys very good positioning in global VD3 industry and if we see deployment of cash flows as an opportunity which can make long term wealth creation happen then only we should touch this stock,

Having said all these, this I dont feel is a buy and forget kind of investment which can be bought at any valuation…we need to give significant stress to valuation when we are analysing this company.

Rgds.

Discl. - Invested

https://divisnutraceuticals.com/products/human-nutrition/vitamin-d/

Various products by Divis…

Thanks for your detailed reply. Agree with your points.