For HUL,just take a look at the how the margins have grown in the past decade from 12-13% to 25% currently,while the sales growth has been a measly 6-7%.

This is not the end as the management after integration of GSK Consumer’s business wants to expand margins further by 8-10% in the next few years.

Adjusted for DDT,HUL has paid over 90% of the earnings as dividends.

It has benefited immensely from the Corporate tax cut and DDT removal will mean higher dividend per share.

It is probably trading at more than 50 times next years projected earnings,what multiple one is comfortable with depends on their time horizon,currently momentum and scarcity and are driving up prices.

For the high dividend payout,the reason I would focus on is that the business requires very little incremental capital to grow,the fact that MNC’s want to boost their cash payouts will mean very little if capital is taken out at the cost of core profitability and business growth.

On managements guidance to expand margins further,I would give them the benefit of doubt especially after GSK’s products get put on Lever’s platform,they have improved margins from 12% to 25% which is quite incredible,but I agree that it cannot go on perpetually.

The FMCG industry has always been extremely competitive,the intensity of competitive pressure can vary from product to product and category to category.

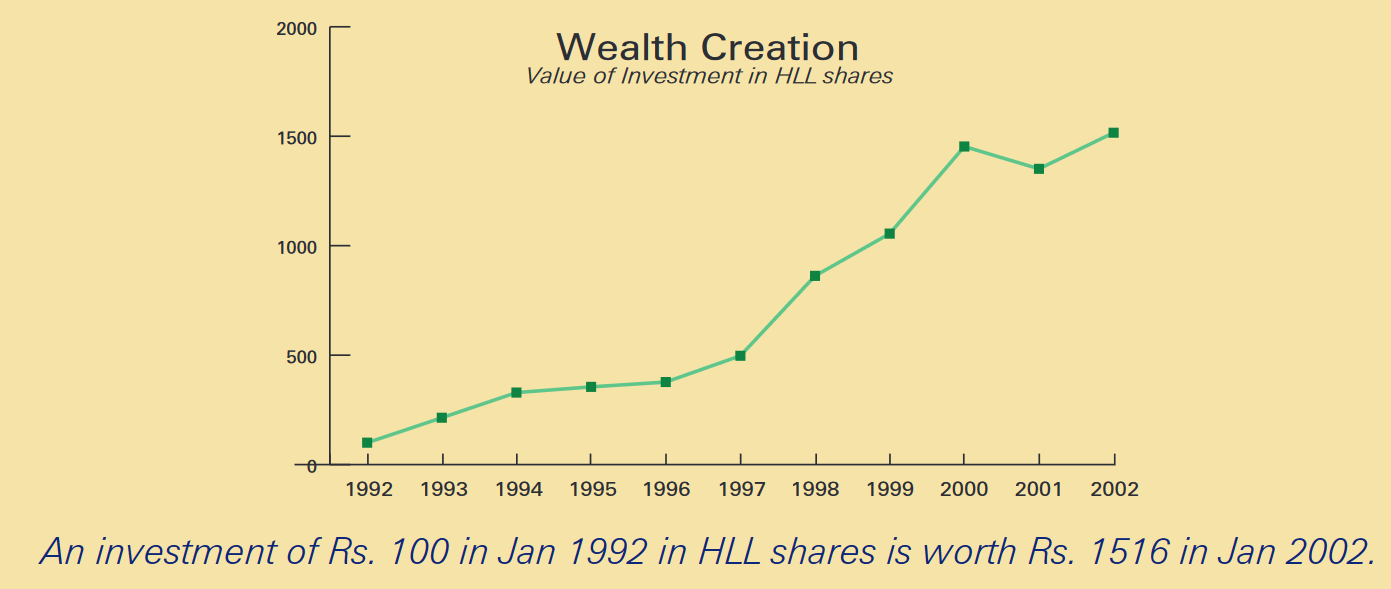

Finally Stats can hide a lot more than they can reveal,here is the return for HUL from 1992 to 2002,a growth of 31% CAGR excluding the dividends.

The market capitalization of HUL has crossed 5 lakh crore now,if someone had told me this would happen I would have never believed it,all this has happened with very little drawdowns.

What happens next,how big this bubble gets and will it burst or when it’ll burst or not I have no clue.