Above article is about how reduced search cost are eroding value of brands.

2 Likes

2 Likes

Good amount of innovation happening in the toothpaste industry led by Colgate. Colgate has also developed a recyclable tube (made from HDPE). Nothing yet for the Indian market though - still it’s interesting to see Colgate continuing to innovate

6 Likes

Emami Ltd now trades at 52 week low (Rs 245 with P/E of 32)

Last quarter results 144 vs 138 Cr looked promising, any expert views on this FMCG?

ROCE has decreased so has P/E

profits are shrinking and it used to be a high growth FMCG story

I used to hold a small portion of emami a while ago and exited it when it was 320 range and the numbers were poor when other companies were able to do well. I think the pledging is weighing on this stock. These days I feel we are better off betting on winning horses than these turn around stories.

As long as there are structural issues with 2 of their biggest brands- Boroplus , Fair and Handsome…growth may be really hard to come by.

They are trying their best to make amends, have hired the BCG also. Lets see what happens.

Disc : had sold all my Emami holdings @ 420 or so.

2 Likes

1 Like

If you were already tracking, what % of current sales of Dabur comes from sanitiser and what level it can grow to? I assume the first is 0% if they dont have any santiser products earlier. But what is the kind of stanble market size (after current scare and panic buying stage)

Yes, Dabur has entered this category in this opportune time and so revenue contribution is nil.

Historically in India the sanitizer used to be a very small category. According to a report, " The Global Hand Sanitizer Market size was valued at $919 million in 2016", and I expect the most contribution was from developed countries.

In India, there used to be only two well-known Sanitizer brands: Lifebuoy and Dellol. But, many companies have jumped into the market now and I can expect the market size to increase multiple times (!) and become closer in size to the hand wash market size in this high-demand scenario. This market size can reduce after the paranoia gets over but may still remain at-least double the size than before the paranoia. In that market, Lifebuoy and Dettol is still expected to dominate, but the products from Dabur, Savlon, Himalaya etc. will still be expected also accrue meaningful revenue from this category.

2 Likes

Like the nimble management being able to quickly roll out the product basis market requirement. Speaks a lot! Though given the small market size, could turn out to be more of a gimmick at this point

I won’t say this as a gimmick. There is real need for quality branded (trusted) sanitizers in the market & existing players are not able to make amends. Lot of unknown companies are listing their Sanitizers in the online marketplace which people are buying in desperation without being sure about the quality. Fake street products are rampant too in the unorganized market.

I believe it is a real responsible act by Dabur to use their resources to fast tract this product, so that people can get their hands on a trusted brand.

And, they did this in urgency unless they wouldn’t have launched it under front-line Dabur brand. They usually launch such hygiene products under fem brand (e.g. hand wash), which not many are aware to be from Dabur stable.

Actually, Dabur launched fem Safe Handz sanitizer in 2011 but discontinued it after low demands. I believe they didn’t relaunch it because what people need these times is trust and fem don’t yet enjoy that.

https://www.adgully.com/dabur-debuts-into-hand-sanitizer-market-with-fem-safe-handz-46380.html

2 Likes

Excellent observation and great learning to understand branding. They would intentionally launch it as dabur because they would want this brand to resonate with country people with the product they need most at the moment. Indeed, smart branding move. The product not only adds to revenue but also acts as a mascot of the company and what it stands for.

13 Likes

Good report on FMCG by HDFC Securities

6 Likes

Just as the Covid-19 outbreak intensified in India, Dabur advanced the launch of its hand-sanitiser brand Dabur Sanitize . Similarly, earlier this month, it launched immunity-boosting tonic Dabur Tulsi Drops , which was earlier set for a June launch.

In line with this nimble-footed launch strategy, the company has now decided to launch a range of single herb c hurnas which include immunity-boosters like Giloy Churna , Amla Churna and Ashwagandha Churna . The other products in this range are Hareetaki (Harad) Chura , Neem Churna, Arjun Chhal Churna and Brahmi Churna .

Malhotra believes that in the post Covid-19 world, the importance of personal hygiene and ayurveda-backed preventive healthcare will grow in the consumer mindspace in India and international markets.

I have decided to invest lump sum amount in blue chip to earn similar returns.

The bluest of blue chip is HUL.

So, I though, I will invest in HUL once it come down and again I will earn handsomely.

So, I look back at 10 year track record of HUL and this is what it look like.

HUL share price on 16th April 2010 - 227

HUL share price on 14th April 2020 - 2350.

Return of 26% CAGR over last 10 years.

Yippee.

But if I go back 10 more years, this is what I found.

HUL share price on April 2000 - 222.

Now, let’s calculate return again with assuming investment made in 2000.

Return of 12% CAGR over last 20 years.

Lesson learned -

- Being blue ship doesn’t necessarily guarantee great return.

- Timing of Entry into a company is far more important than it seems (though SIP expert don’t agree here)

- Exit is equally important as entry

- Blue chip won’t give astronomical return of small companies

- Go for blue chip if you want Average but stable return

- For great return, 20x - 50x of your capital over 10 years, go for small caps (preferably)

6 Likes

For HUL,just take a look at the how the margins have grown in the past decade from 12-13% to 25% currently,while the sales growth has been a measly 6-7%.

This is not the end as the management after integration of GSK Consumer’s business wants to expand margins further by 8-10% in the next few years.

Adjusted for DDT,HUL has paid over 90% of the earnings as dividends.

It has benefited immensely from the Corporate tax cut and DDT removal will mean higher dividend per share.

It is probably trading at more than 50 times next years projected earnings,what multiple one is comfortable with depends on their time horizon,currently momentum and scarcity and are driving up prices.

For the high dividend payout,the reason I would focus on is that the business requires very little incremental capital to grow,the fact that MNC’s want to boost their cash payouts will mean very little if capital is taken out at the cost of core profitability and business growth.

On managements guidance to expand margins further,I would give them the benefit of doubt especially after GSK’s products get put on Lever’s platform,they have improved margins from 12% to 25% which is quite incredible,but I agree that it cannot go on perpetually.

The FMCG industry has always been extremely competitive,the intensity of competitive pressure can vary from product to product and category to category.

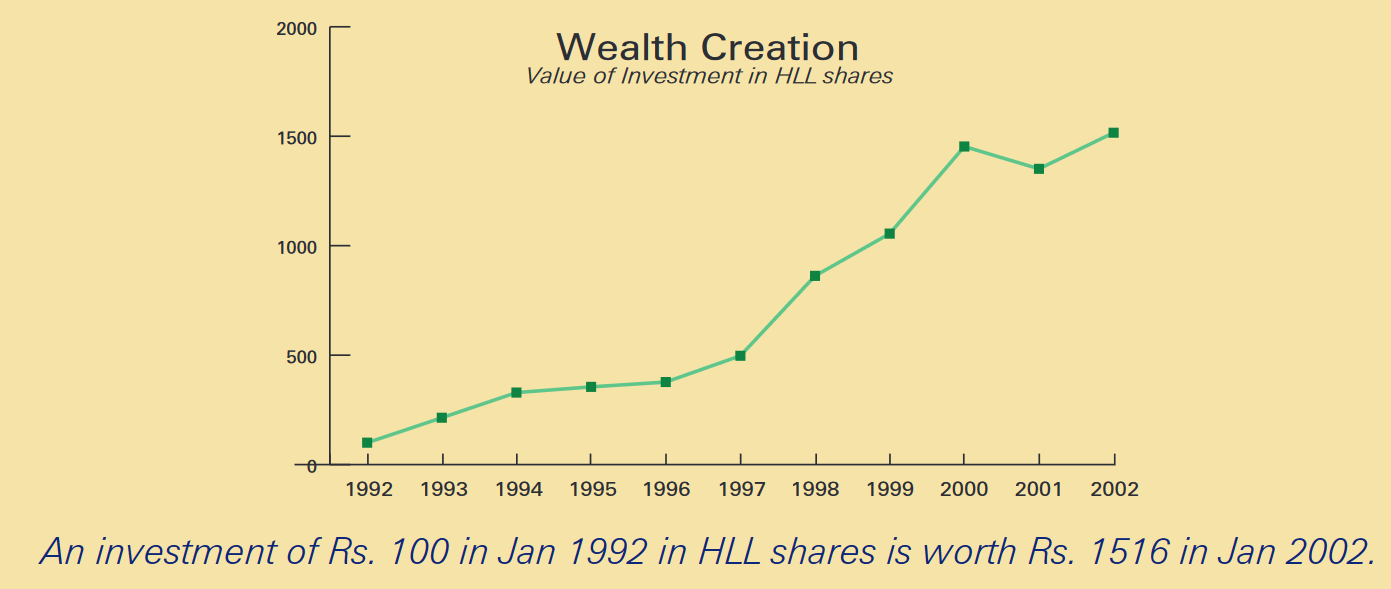

Finally Stats can hide a lot more than they can reveal,here is the return for HUL from 1992 to 2002,a growth of 31% CAGR excluding the dividends.

The market capitalization of HUL has crossed 5 lakh crore now,if someone had told me this would happen I would have never believed it,all this has happened with very little drawdowns.

What happens next,how big this bubble gets and will it burst or when it’ll burst or not I have no clue.

5 Likes

On one hand you explain beautifully the beauty of the company and its business and then again call it a bubble. Valuations are rich but the fundamentals supporting it are solid. It can be a case of stagnancy in stock return for significant time but what makes you call it a bubble?

Haha,the thoughts that go on in my head,sometimes I wonder if I am crazy:)

With regards to the bubble reference,the business is indeed excellent but I am referring to the market capitalization of the company with regards to its profitability,how momentum is pushing it further higher and higher,this tends to happen with stocks that are in bull markets.

The management has also cleverly used their stock as currency(thereby diluting their stake) and acquired GSK Consumer in an all stock deal rather than paying cash,this same management made an open offer about 6-7 years ago when the stock was trading at 35 times 1 year forward earnings taking their stake to 75%,at that time the consensus was to tender the stock to Unilever PLC at Rs 600 per share.

The market cap is Rs 516,000 Crores,If you had this money would you buy the entire company?

What will happen if the company does not deliver on expectations…the consensus is that there will be a time correction but I don’t know and I think it’s very dangerous to assume that one can predict that outcome with certainty.

I like the company but I am not in love with it.

2 Likes

Something similar happened from 2000 to 2004

Sales actually went sluggish and there was heavy competition from Nirma and sache shampoo concept

Stock went from 56 (1998) to 200+ (2000)

Then it remained in (160 - 280) for next 10 years

Price remained stagnant

And even today, after such drastic price increase and flattish sale, risk of stagnation is there