Recently, I got to study Fairchem Organics and I composed this article to provide an overview of the company.

Fairchem Organics: Emerging Oleochemicals Leader

A few months back, Fairchem Organics (“Fairchem”) demerged from Fairchem Speciality Chemicals (now Privi Speciality Chemicals) and got listed. There is not much analyst coverage of this company. A few days back Moneylife printed an article titled “Fairchem Organics: Exceptional Growth.”

Fairchem’s products are classified under oleochemicals. Oleochemicals are green replacement for petrochemicals. Oleochemicals are derived from vegetable oils and constitute 7.5% of the speciality chemicals market in India. They are used as food additives, plastic additives, pharma additives and surfactants. Oleochemicals worldwide demand is likely to grow at 7.57% CAGR between 2021 and 2028.

Fairchem: Emerging Oleochemicals Leader?

In summary, Fairchem Organics is an established, fast-growing, low-cost manufacturer of certain oleochemicals. Fairfax India Holdings, backed by the billionaire Prem Watsa, is the major promoter of Fairchem. The company completed its capacity expansion from 18K MTPA to 45K MTPA between FY14-FY16, and to 72K MTPA in FY21. Within FY22, expansion to 120K MTPA and forward integration will be complete.

History: Mind the Names

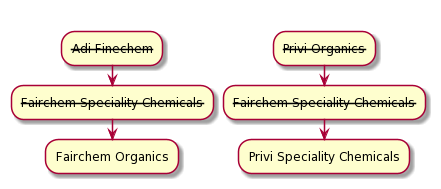

Back in 2016, there were two companies: Adi Finechem (listed company) manufacturing oleochemicals and Privi Organics (unlisted) manufacturing aroma chemicals. The end-markets of both the companies have been fast growing. In 2016, Fairfax India Holdings acquired controlling stake in Adi Finechem, and bought and merged large part of the Privi Organics business into it. The resulting entity was named Fairchem Speciality Chemicals.

Oleochemicals and aroma chemicals businesses are very different. So, the two businesses parted ways. After various activities of mergers, capacity expansions and demerger, the end result in 2021 is two companies:

- Fairchem Organics (listed), focused on oleochemicals, is promoted by Fairfax.

- Privi Speciality Chemicals (listed), focused on aroma chemicals, to be controlled by the promoters of the erstwhile Privi Organics; 48.8% stake to be bought from Fairfax.

Since Fairchem Organics is demerged recently, its pre-2020 results are not accessible via the usual means.

The investor presentation does depict the highlights of the results from FY17. The pre-2016 results of Fairchem Organics business, when it was Adi Finechem, are the pre-2016 results of what is now Privi Speciality Chemicals. Between 2017-2020, the results of Fairchem Organics are (with likely small discrepancies) the standalone results of what is now Privi Speciality Chemicals.

High Entry Barriers

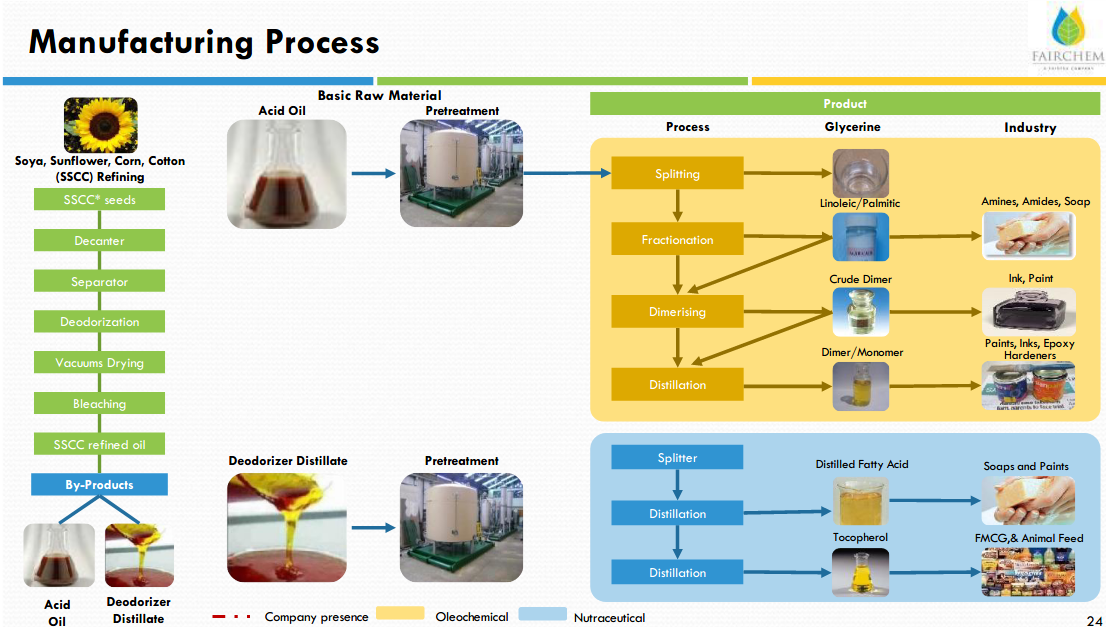

Fairchem has one-of-its-kind manufacturing using by-products of vegetable oils (namely Acid Oils and Fatty Acids), creating Waste to Wealth. Over the past several years, they have perfected the technology to convert inconsistent raw material quality into consistent quality output. Whereas other oleochemicals manufacturers use vegetable oils, Fairchem uses by-products of vegetable oil—this gives them a distinct price advantage.

Fairchem has been manufacturing for 25 years. Customers include Asian Paints, Huber (erstwhile Micro Inks), Arkema, BASF, ADM, and Cargill. They use imported equipment such as Short Part Distillation from UIC Germany, and Fractionation from Sulzer Switzerland.

Fairchem is one of the few manufacturers of Linoleic Acid and Dimer Acid in India, which are the major part of the overall revenues and having a large addressable market size in India.

(Source: Company presentation)

Market Recognition for the Listed Peers

Fine Organic is one of the largest manufacturer of oleochemicals in India. Its current market cap is more than 4x Fairchem Organics. Galaxy Surfactants has 60% market share in surfactants derived from fatty acids. Godrej Industries has 13% revenue from oleochemicals.

Fine Organic is into food additives and Galaxy is into household products. Their products cater to a different market compared to Fairchem.

Fine Organic’s PE ratio is as high as 70. It is one of the few small caps that performed well during 2018-20. Galaxy Surfactants has a PE ratio of 35.

Risks

-

New promoters:

Even though the company has done well for the last 3-4 years under the new promoters, yet the governance, strategy, cash deployment and investor-friendliness have to be monitored going forward.

-

Recent demerger:

Detailed information is not available, for example, regarding client concentration, current capacity utilization, current and future revenue mix, and R&D focus areas and expenses. The Moneylife article said 50% of their revenue comes from top 5 clients, which is a client concentration risk (I could not verify this independently).

-

Raw materials:

Fairchem calls itself an Oleochemicals and Nutraceuticals manufacturer. However, Nutraceuticals revenue is declining from around 33% of the total revenue in FY13 to 3% in FY20, likely due to the high price of raw materials. In Nutraceuticals, the company produces Tocopherol, which is used in natural Vitamin E. This product of the company is intermediate and therefore does not command high price. Company has been unsuccessfully trying to shift to better-margin products.

The company faced the issue of unavailability of raw materials in the past, for example due to drought in the countries from which these are imported. Raw material availability of soybean oil by-products in India is low. Company is trying to shift to other raw materials like palm oil by-products to reduce risk of unavailability.

-

Forex:

Forex risk is limited since a large part of the raw materials is imported and finished products are exported. Also, the product prices are correlated with raw material prices.

-

Technological:

If a competitor develops new and substantially cheaper manufacturing technologies using altogether new inputs for making various kinds of resins for making paints, printing ink, hardeners. The likelihood of this happening is low.

Financials

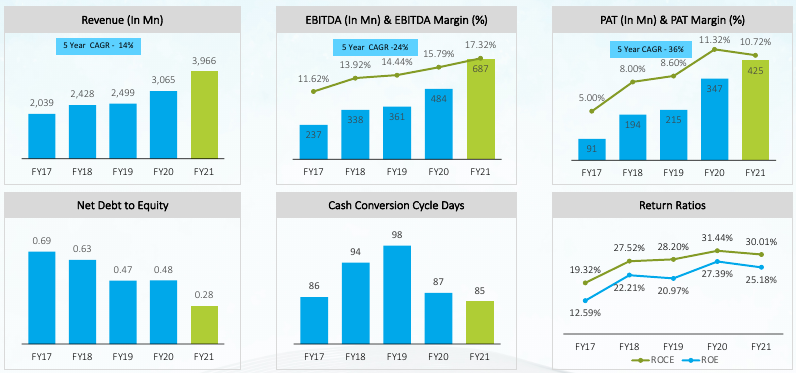

The company has low debt. PAT margins grew from 8% in FY18 to more than 10% in FY21. ROE consistently grew from 22.2% in FY18 to 25.2% in FY21.

(Source: Company presentation)

Capacity expansion from 45K MTPA to 120K MTPA and forward integration will cost around Rs 100 crores, most of which will be paid via internal accruals.

Good Upside Potential

In the last five years, Fairchem’s revenue has been growing at 14% CAGR and profit at 36% CAGR. Fine Organic revenue has been growing at 11% CAGR and profit at 13% CAGR. Galaxy Surfactants’ revenue has been growing at 9% CAGR and profit at 24% CAGR. Both the revenue and profit growths of Fairchem are higher than Fine Organic and Galaxy. EDITDA and PAT margins are similar to Fine Organic and higher than Galaxy.

For Fairchem, PAT of Rs 150 crores seems to be achievable after the completion of capacity expansion to 120K MTPA. At PE of 30, the market cap will be Rs 4500 crores. The current market cap is around Rs 2000 crores. Fine Organic is currently trading at PE of around 70, Galaxy at 35.

References

- June 2021 Investor Presentation.

- FY20 Annual Report of Privi Speciality Chemicals

- Mergers, demergers: July 2016 Merger Investor Presentation and FAQ. May 2019 Demerger Transaction Overview.

Disclosure: Invested 3% of my portfolio, currently with small profit %.