In past few years active vs passive style of investing has been a hot topic of discussion in the industry. Globally as well as in India Number of active funds, fund managers underperforming the benchmark indices has forced many investors to switch their portfolios from active funds to passive funds, which is evident from the fund flow towards index funds & ETFs. For a retail investor, Index investing is a predominantly safer way to invest in long term by avoiding the risks involved in active fund management or stock picking.

Although the awareness about the passive investing is increasing, the majority retail investors are unaware about index funds and particularly, factor based or strategic indexes. As per the current AUM data only 22% of Equity investment is in index funds, and approx. 1% is in factor-based indices or strategic indices. Passively managed strategic index funds offer a great opportunity for a retail investors to overcome the downsides of capitalization weighted index funds.

The major shortcomings of capitalization weighted indices are:-

- i. Concentration:- Few large cap companied dominate total returns of Index. ( In case of Nifty 50, top 10 companies constitute approx. 50% index)

- ii. High Volatility and drawdowns

- iii. Expensive valuations:-Overvalued stocks are overweighted and Under Valued stocks are underweighted.

Factor based portfolios designed using different weighting methods can be used to eliminate or mitigate the shortcomings of capitalization weighted indices/ portfolios.

Although the factor-based index investing is comparatively new in India, Globally factor based investing has been studied and implemented for decades. The purpose of this thread is to understand factor-based investing and resources available in India for factor based investing or smart beta investing.

Factor Definition: -

For those who are unaware about the Factor based investing/ smart beta investing,

factor based investing is simply about defining and then systematically following a set of rules that produce diversified Portfolios.

Factor selection:-

In past few decades hundreds of factors have been discovered and examined by academics and practitioners. To determine if a factor can be considered for execution, it should fulfill the following criteria

-

- Intuitive/ Economically sensible :- There must be a behavioral or logical risk based explanations for existence of persistent risk premium.

-

- Persistent returns:- Factor returns must hold across long period, various economic regimes and has not disappeared after it was documented in academic literature.

-

- Pervasive returns:- Factor returns must hold across countries, regions, sectors.

-

- Robust:- Factor returns should not significantly change with small change in factor definition.

-

- Investable:- It must be possible to capture the factor returns in efficient way after implementation costs.

There are only handful factors which fulfill the above mentioned criteria, namely: Market Beta, Size, Value, Momentum, profitability, Quality, Low Volatility. Factor risk premiums are calculated by using long/short portfolios. However, the index investing or passive investing is generally based on the long only factor portfolios.

- Investable:- It must be possible to capture the factor returns in efficient way after implementation costs.

Weighting schemes:-

Various weighting methods are used to create a portfolio by combining either active risk &/or factor signal with or without market capitalization. We will briefly look at the various weighting schemes for reference.

Capitalization weighted portfolio:- Stocks are shortlisted based on factor signal and then the weights are based only on market cap of the shortlisted stocks.

Capitalization scaled portfolio: - Weight of stock in portfolio is determined by multiplying factor score by it’s market capitalization

Active risk constrained optimization:- Stocks weights are determined by combination of factor signal and active risk consideration.

Signal Tilt:- Weight of stock in portfolio is determined based on factor score & is independent of market capitalization. Weight from stocks with low factor score is transferred to ones with higher factor score.

Equal weighting:- Stocks are selected based on factor signal and equal weight portfolio is formed.

Signal Weighting:- Stock wight in the portfolio is determined based only on factor signal.

At present the strategy or factor based indices in India are based on capitalization scaling method.

Multi factor Portfolios:-

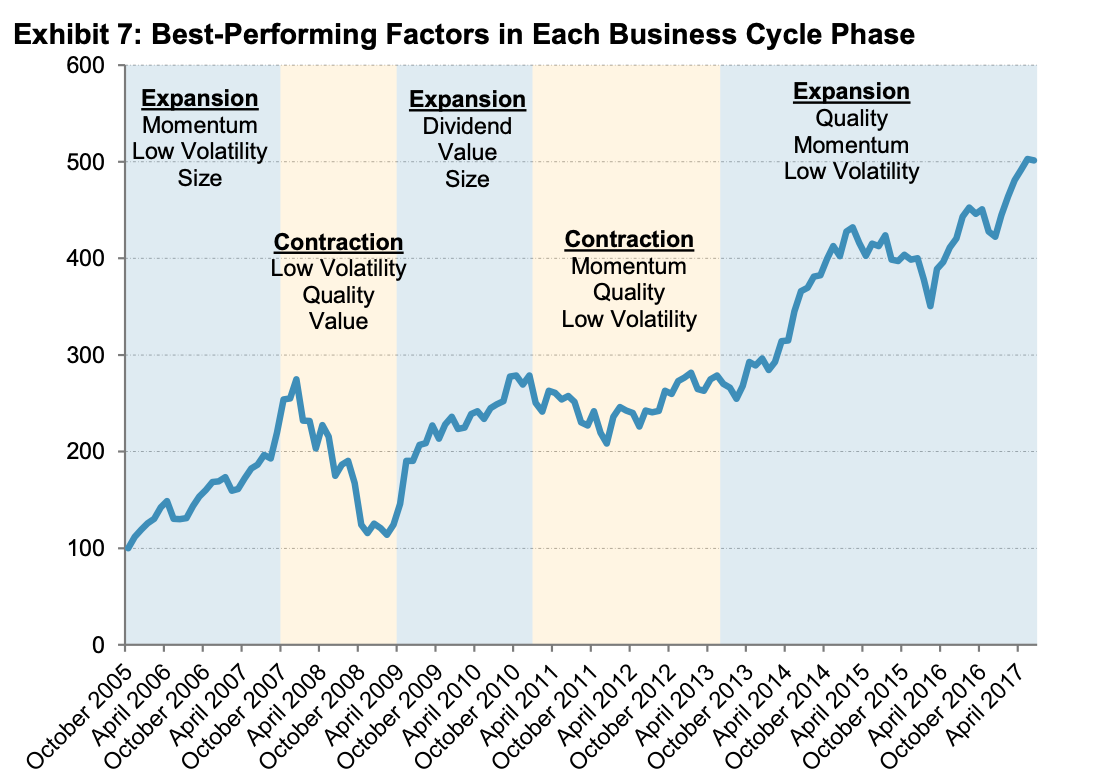

The individual factor portfolios are constructed based on factor signal and weighting methods. From historical performances of the individual factors, it can be observed that the factor performances are cyclical. Factor portfolios can underperform Market cap-based indices for short duration. The cyclical performance of the factors can be observed across different business cycles, market cycles and investor sentiment regimes. Therefore, it is advised to create a multifactor portfolio to reduce the risk of underperformance in shorter timeframe, active risk reduction, better risk adjusted returns, information ratio etc.

There are two methodologies used for construction of a multifactor portfolio:

-

- Portfolio Blending:- In the portfolio blending method Individual factor portfolios are constructed and these portfolios are combined to create the multifactor portfolio. The weights of an individual factor portfolios can be based on equal weighting, risk weighting etc.

-

- Signal Blending:- To form a signal blending portfolio , individual factor signals are combined to create a composite signal.

Various individual investors, fund managers, PMS were able to earn risk premium of factors. It is difficult for a retail investor to study the various characteristics, risks & opportunity costs associated with factor selection, Weighting methods, portfolio construction methods. Examining and evaluating each unique combination with systematic analysis may prove challenging for an ordinary retail investor.

Factor based indices can provide an easy to implement solution to simplify factor investing for retail investors. Let’s look at the current resources available in India for the implementation of passive investing. We will also review the passive investment based on Broad based Indices along with strategy (factor based) Indices.

Ideally the ETFs are better instruments for implementation of passive investment, however in Indian market majority ETFs suffer from liquidity issues. Due to lower liquidity, higher bid-ask spreads, higher capital required for basket creation, it is practically difficult to build and rebalance multifactor portfolio.

We must rely on index funds for implementation of factor portfolio.

Building portfolio with available Index Funds:-

At present there can be four approaches to build a diversified portfolio.

-

Broad based indices:- Form a portfolio with the help of single total market fund or portfolio bending using different index funds based on Large, Mid, Small cap indices. This portfolio diversifies across only market capitalization. There is no exposure to strategic, factor-based indices.

-

Single factor portfolio: - Invest in single factor index. Various index funds & ETFs are available on Quality, Low Volatility, momentum, value, alpha, ESG, dividend factors, for numerous stock universe. T

his portfolio has higher concentration risk as the entire portfolio is based on a single factor. -

Multifactor portfolio:-

i. Port folio Blending:- Create a portfolio with use of different individual factor indices.

NSE has launched several indices based on various factors and using different stock universe. Due to unavailability of all factor indices within any single stock universe, it is difficult to consider Nifty indices for portfolio blending, and it also creates risk of overfitting. S&P BSE has launched indices based on Momentum, Quality, Low Volatility and Value using same underlying index (stock universe). Except for S&P BSE Momentum, index funds are available for other factors. In current scenario, the ideal combination for monthly rebalanced multifactor portfolio using portfolio blending technique can be created with the help of following index funds.- Nifty 200 Momentum 30

- S&P BSE Enhanced Value Index

- S&P BSE Quality index

- S&P BSE Low Volatility Index

- Nifty 200 Momentum 30

(It has been observed that the value factor has given lower returns and shown higher volatility compared to other factors and benchmark index. However due to negative long-term correlation with other factors, it has helped in improving performance of multifactor portfolio.)

ii. Signal Blending:- Invest in a multi-factor index. At present index funds & ETFs are available for only one multifactor based index, i.e., Nifty Alpha Low Volatility 30.

-

Combination of Broad Based Indices and factor indices:-

As mentioned above factor Indices in India are formed using capitalization scaling method, which obviously has capitalization bias. By combining the factor indices & Small cap indices, exposure to higher market capitalization can be neutralized.

If capitalization bias is not a concern for an investor, a combination of Large & mid cap fund along with multifactor index or individual factor indices can be used.

Every alternative has obvious pros and cons which will affect active returns, drawdowns, volatility, information ratio, risk adjusted returns. Historically the individual factor portfolios (based on Quality, Low Volatility, momentum, value), and multifactor portfolios have generated higher returns than broad based indices on a longer (typically above 10 yrs) timeframe.

Risk in factor based investment:-

- Short term underperformance: - Individual long only factor portfolios may underperform benchmark indices in short duration under different microeconomic events.

- Reduction in risk premium: - Globally it has been seen that the risk premium of factors reduced after publication.

- Crowding: - Crowding results from higher number of products offered or higher capital invested in single factor. It may negatively impact risk premium.

- Costs:- The county wise &/or individual tax brackets, implementation costs, expense ratios, tracking errors, direct taxes resulting from the turnover of monthly balanced portfolios may result in reduction of active returns.

- Capitalization bias:- Index funds are based on capitalization scaling models which results in high capitalization bias.

Benefits of Factor investing:-

- Historically proven track records of active returns across global markets and different economic regimes.

- In India the strategic factor indices follow the cap on individual stock weight and on sectoral weight, results in limiting the high capitalization bias and overweight of overvalued stocks.

- Better Risk adjusted returns compared to market returns

- Better information ratio.

- Avoids portfolio concentration risk

Resources:-

Equity smart beta and factor investing for practitioners by Ghayur, Heaney, Platt

Your complete guide to factor based investing by Berkin & Swedroe

https://www.niftyindices.com/reports/research-paper

Nifty Passive insights:-

https://www.niftyindices.com/Nifty_Passive_Insights/Nifty%20Passive%20Insights%20Quarterly%20Update%20-%20April%20to%20June%202022.pdf

Factor Risk Premia in the Indian Market : -

Factor Performance Across Different Macroeconomic Regimes in India: - https://www.asiaindex.co.in/documents/research/research-factor-performance-across-different-macroeconomic-regimes-in-india.pdf

An Index Approach to Factor Investing in India: -

Factor Indices in India: Factor Exposures and Style Analysis :-