Assystem technologies GMBH took over SQS Germany open offer .Expleo solutions ( erstwhile SQS BFSI india) came as a free catch , without any payment as a consequence of take over of SQS Germany.

Now SQS Germany was delisted & name changed to Expleo group containing several entities in Europe, UK ,USA & Germany

In india the delisted or unlisted erstwhile SQS Germany is present as Expleo technologies India Pvt limited at Pune & Bangalore.

.

Now coming to listed entity the erstwhile SQS india BFSI , name changed to Expleo solutions is headquartered in Chennai . 6 Fully owned overseas , subsidiaries of this listed entity is present in UK ,

USA, Europe, Singapore etc .

Globally the listed & unlisted entity functions under a single Expleo brand umbrella, though revenues are shared. Annual turnover is around 2 billion USD

To make matters simple, there are 2 entities under Expleo branding, the listed is Expleo solutions listed on BSE & NSE. This listed entity has 6 fully owned overseas subsidiaries.

The unlisted or rather delisted entity is the erstwhile SQS Germany , present in Germany, Europe,UK ,USA.

Also this unlisted entity is present in india as Expleo technologies India at Pune ( 3000 seats) & Bangalore.

Balki, Would your research not indicate that these should be merged and delisted OR merged and listed. Based on how EXPLEO globally looks at it ?

A hypothetical question/comment but based on your deep dive insight in the stock thought let me put across…

Now the listed entity Expleo solutions catering to BFSI segment is doing well, while the unlisted entity Expleo deriving 50 percent revenue from BFSI is doing well, while the balance 50 percent from Non BFSI segment is impacted due to covid induced displacement in automotive ,arerospace , travel, Retail etc.

Now the focus is on ramping growth.

All decisions will be taken by PE investor Ardian .

Possibilities of delisting Expleo solutions in future or IPO of unlisted entity Expleo may take place in future or both the events can occur in future .

Thanks for your continuous efforts, much appreciated and a big thanks from the investor community.

Since most of you touched on the numbers, ratios etc… Since I am not good at those and I rely on others to scrutinize and post their findings on numbers. I am trying to understand what is the edge this business has , please read this it will give some good overview about the latest buzz in the industry DEV OPS based testing. link, very simple to follow

I am still trying to understand the triggers. The edge this Franchise has and the reasons for not to invest. I have started with FY21Q3 call, I have this habit of listening to the audio and following the transcript (Former will give some impression about the promoters how they are responding - it is like the indicator for Fundamentals based investing {like charts for technical guys} )

I am still trying to connect the dots with regards to synergies of this PE, for example in Sequent scientific once Carlysle taken over they immdiately did three things

Hired a specialist consultant to find the opportunities for them to grow (Growth)

Hired management consulting firm (Fine tune the processes )

Brought in a subject matter expert on animal pharma onto the board as a Director (Technical Know How )

I am trying to understand what are those changes happened since 2017 (since Adrian took over ), as I said I have just started I don’t know much. I have noticed a new Group CEO Mr. Rajesh Krishnamurthy appointment , please add if you have more data points on these lines so that we can try to connect the dots and see how it will play out. For me these are the trigger to watch out for.

Capabilities - Usually software testing (aka QA) is very under rated, there is this popular opinion anyone can do this job(but not anymore). In the recent call I can see the management strategy is to have less resources with skill set of dev ops based testing (more automation - less resources )

But there are some niche areas in testing not everyone is specialized, like

Security risk assessment testing (Few days back we had ransom call for pipeline attach in US )

Penetration testing - Recently just before our project sign off IT sec. foot their foot down and said show us the proof for both of these ? So we had to go out and hunt for such specialized players

We need to do more scuttlebutt with the employees who are working from the lower level to mid level what are those unique capabilities that they have

One more thing I have noticed is they are not a pure testing based company anymore so they are now working on the entire life cycle of software development

Risks (Reasons for not to invest )

From the call I felt like Mr Balaji was not confident when asked about why are you sitting on the cash either you give it or use it for in organic opportunities, from his response I felt like he is not given a free hand to decide and he is tied by the group management (This is purely my guess I may be wrong here )

I am yet to find what is that unique edge that they have , they listed on their site that they are into many different verticals like aviation (definitely this is Niche ) etc… but we need to understand more

In India attrition is too high, there is huge shortage in specialized skills like DevOps, unlike previous generation (20 years from today ) the current generation have plenty of options to choose from (no immediate pressure to work from family , grown up with all the comfort , feel free to disagree with me : ) ) . I am saying this with complete responsibility, I used to work continuously for weeks or months during delivery ( I am sure there are many still working) but often we hear from the onsite co-ordinators and the project managers based in India, these youngsters don’t give any damn if we ask them stay back a bit we have critical delivery. So all in all we have to see what is the attrition rate and the revenue generated by each employee

1)I presume that PE investor Ardian has done due diligence & evaluated the risk reward ratio , before buy out of SQS Germany at 60 percent premium to market price & creating Expleo brand umbrella

I presume that cash on the books will be used to drive growth & to double the turnover in coming 3 years , instead of giving dividends, buyback etc. Yes Balaji Vishwanathan, MD has no role in taking the call on utilising the cash in books, it will be decided by the parent .

World wide, Expleo brand functions under a single brand umbrella using common office space & front staff.( There are no entities listed or unlisted or subsidiaries,as far as the client is concerned, though revenue is shared between entities )

Devops & Agile methodologies are trending while watermark template is obsolete.

Expleo brand umbrella was created to nurture growth & the group is focused on doubling turnover in coming 3 years.

Rajesh krishnmoorty ex Infosys group head was brought in to drive growth.

coming to insiders ,Rajiv kucchal , director of Expleo & ex Infosys group head & venture capitalists hold 75,000 shares of Expleo , while Nihar Nilekani,son of Infosys director, Nandan Nilekani hold 50,000 shares.

Expleo has acquired Moore house consulting UK,so their services can be used within the group,in addition to existing line of business of Moore House

Past 5 years has shown subdued topline growth for Expleo solutions. Despite this it has managed consolidated EPS of ₹40 for past 4 years , the lowest EPS of ₹24 was managed during the height of brexit & forex losses.

The coming 5 years are favorable for IT sector due to digitalization being a necessity, rather than an option. So anticipate hefty growth ahead.

History of indian entity

Without due diligence, VA Ashwani Kumar & his wife Vanaja Arvind from Madras , started Reliant trading services for dealing in computer consumables, which then forayed to software testing in stages , creating Thinksoft global , which went for an IPO.

World wide ,Thinksoft global was competing with SQS Germany , forcing the latter to outsource work from the former , resulting in buyout of Thinksoft by SQS Germany & change in name of Thinksoft to SQS BFSI india.

Final take , The listed entity Expleo solutions derives nearly 100 percent of business from BFSI segment, though this quarter it is also in execution of Robotic process automation for non BFSI client & similar orders are likely. The non listed entity derives 50 percent from BFSI segment, which is doing well, while the rest 50 percent is derived from non BFSI segment of automotive & aerospace which is impacted.

Expleo results on March 20. A live investors concall will be conducted probably on 21 March around 4 pm. You may listen live to the concall or record the concall ,if you are at work & get a glimpse of what the future holds.

French PE investor Ardian , founded 25 years ago,manages funds over 100 billion USD & is one of the leading PE investment firm in Europe. It manages various funds ,real estate & fund of funds.It also manages airports as well as holds & runs a portfolio of 150 companies. Expleo is one of them.

Therefore I presume, that Ardian has done due diligence & Risk Rewad Ratio , before buying out SQS Germany & creating the Expleo brand umbrella

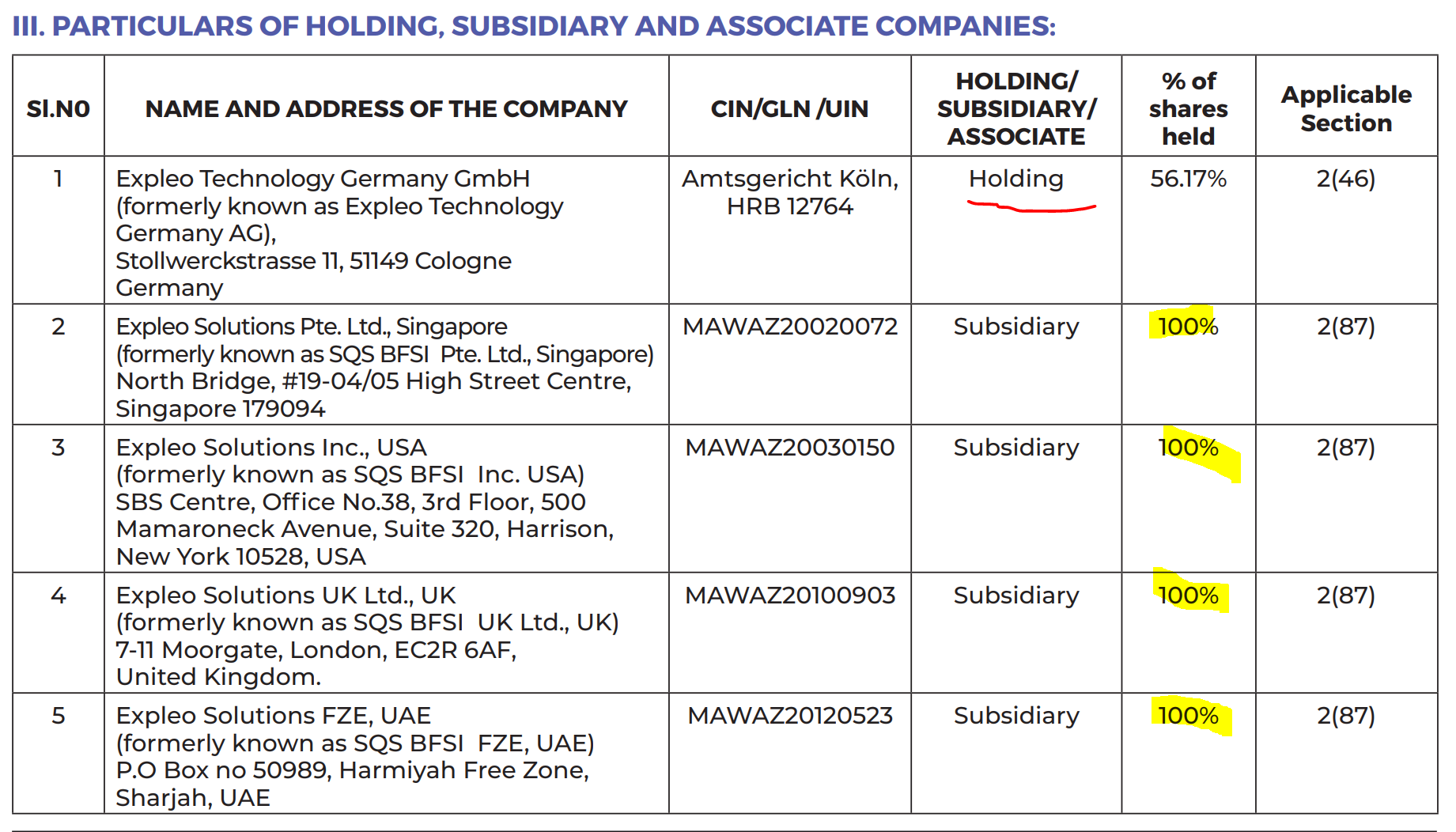

@Balki , how come the standalone and consolidated revenue numbers are same ? Am I missing something here ?

From the AR I can see there are four subsidiaries , 100% owned by Indian listed company. Standalone income is only from Indian entity and consolidated should include India + 4 Subsidiaries

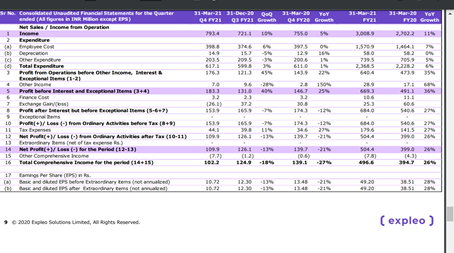

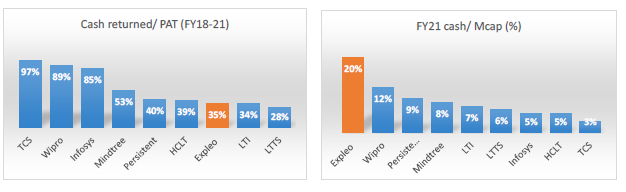

They are sitting on Rs140cr cash which is 20% of M cap. Its very surprising the dividend has not been paid for the last three years especially their peers have increased payouts substantially to 100% of PAT.

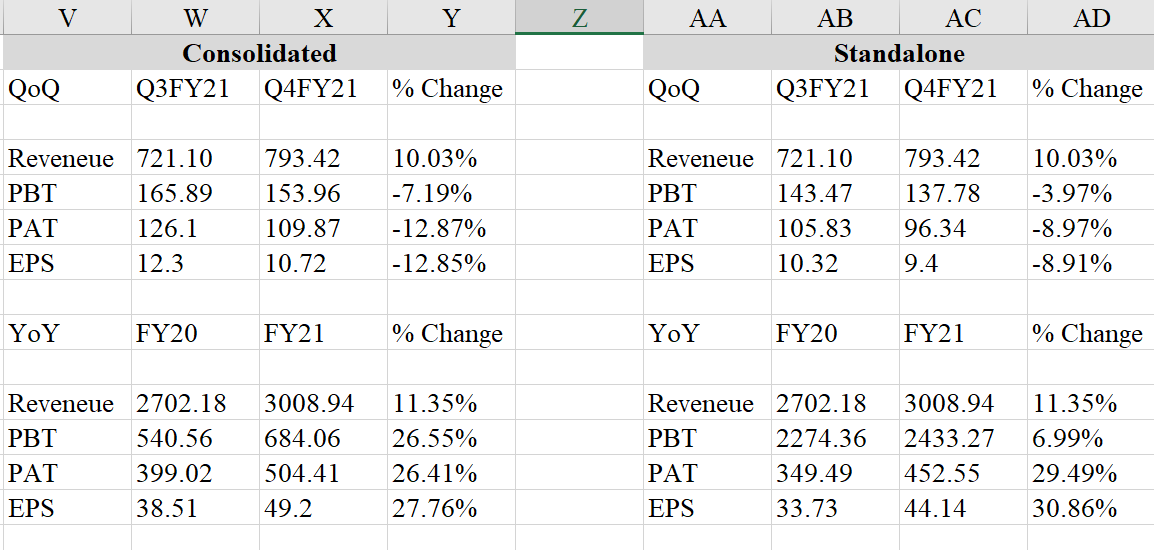

Operational performance seems to be good both QoQ and YoY

QoQ 10% revenue and 40% PBIT

YoY 11% revenue and 36% PBIT

YoY EBDITA at 24%+ from 19% earlier

Exchange loss(forex) has made this look optically down on Q4 level

with close to 50cr PAT and much higher cash flow generation on yearly basis - mkt cap of sub 700 Cr is kind of opportunity if peers (smallcap IT) are to be compared - rerating has to happen. Cash adjusted EPS will be much higher around 60.

Remember Resources are Raw material in IT setup, per press release strong head count addition of 250+ over last 2 Qtr and similar addition for next 2 Qtr - company is effectively increasing headcount by 500 (need to adjust for attrition) - practically 1.5X of FY 20 Base. Without pipeline there is no hiring. Digital business share in revenue is growing well with > 26% now(from 15% in FY 20)

Offshore mix has increased, will help margin front more.

Mgmt commentary is key later today to reassure on growth and sustainability of numbers!

I checked headcount numbers and active clients for last 16 quarters. The headcount at end of Q4FY21 is its highest ever. Given the multiple salary hikes IT guys have had in last few months, this is certainly very interesting for the future.

They are sitting on 130 cr cash.

Even in the con call, the MD wasn’t forthcoming what they plan to do with this cash.

Whether that will be used for dividend / acquisition

Was there any mention of the recent mega-deal win requiring recruitment of additional 150 work force?

on results, there is ₹2 cr forex loss , otherwise consolidated EPS would have been higher by 20 percent.

Around₹140 cr in cash. No dividend paid for past 2 years , while a buyback in lieu of dividend at ₹550 per share was done prior to 2 years & prior to that they were paying₹24 dividend every year for past 4 years.

The MD in concall , asked investors to bear with them for another 2 quarters, after which a decision will be taken on usage of this cash for acquisition, dividend or buyback .

.MD also mentioned that, As per sebi order, a dividend distribution policy will be formulated in 6 months.

5 ) in my personal view, the cash may be used for buyback, without promoter participation, to increase promoter stake , while dividend might come after dividend distribution policy comes into effect.