Dear Vineet Jain, you have asked plenty of questions, for which I will give brief & specific reply

IT consists of software development & testing. The world, Both BFSI & non BFSI segments run on software & typically 20 to 25 percent of software development budget goes to testing.

Software testing is expected to grow at a CAGR rate of 13 percent to USD 60 billion in 2026 from USD 40 billion in 2019 . There is space for all & the pie is shared by big & small as well as system integrator companies.

Contours of QA are rapidly changing from manual testing to digital testing & Agile , even though certain clients insist on manual testing. For Expleo ,Manual or traditional testing constitute 20 percent & balance is in digital mode.

Iam , not a software engineer, but have taken pains to study the Business of Expleo . QA ( Quality assurance is to make the system effective & efficient. Typically automated testing is done to save time & money & include performance testing, fixing bugs , security of the system. QA also includes technology transfer, validation, documentation, product quality assurance & improving product lifecycle by updates. Typically u have CMMI ( capability maturity model integrated) from level 1 to 5 & TMM ( Testing maturity model) from 1 to 5.

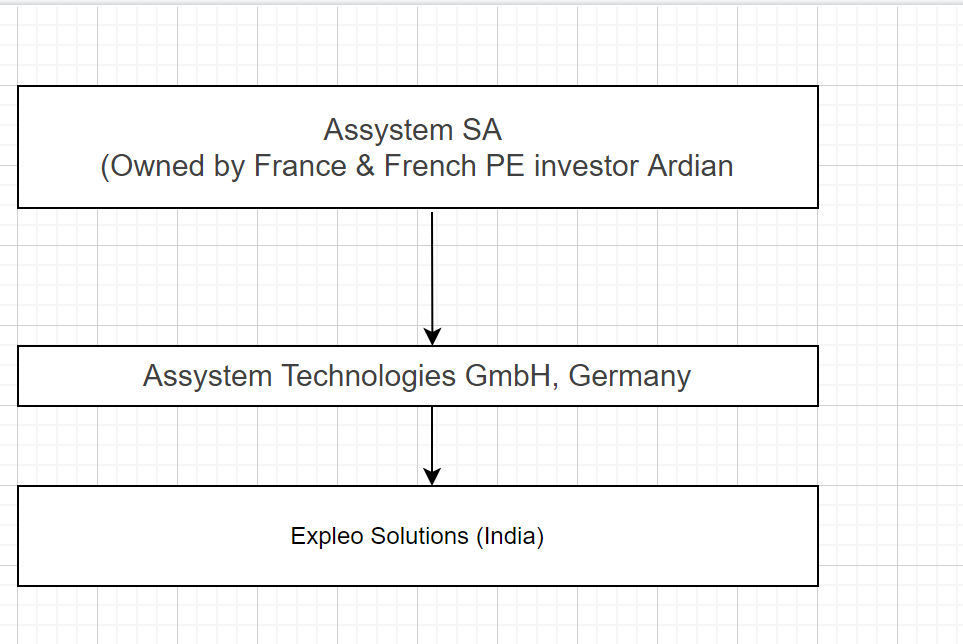

Now ,Expleo gets large projects, which continues over 2 years as well as piece meal work , which gets over in a quarter or two. Similarly repeat clients as well as new clients are mined .

Testing is usually outsourced , though certain system integrators have their own dedicated testing units . The most here, is that all end customers , prefer , testing & validation by an independent dedicated specialist, than testing & validation by the developer of the software.

Paradigm shift, implies new applications like 5G & internet of things, Artificial intelligence application, Robotic process automation, Cloud computing,Data analytics, block chain application for crypto currency, security surveillance etc ,all of which requires QA & validation & improving product lifecycle by updates as well as cutting costs.

Hope I could answer at least a few of your queries.U can get to the web site of Expleo for moats & updates.