Hey guys,

I read through the AR 19-20 and latest QY results, wanted to share my notes here to get your opinions. I will first talk about the standalone and later move on to the consolidated.

Product Segments

Automotive

They sell batteries for a 4W, 3W, 2W and recently E-Rickshaw under different brand names through their distributor network. And sell batteries to OEMs too. They supply to both the new entrants to Indian market, Kia and MG.

They also include the Home UPS, Inverter Batteries and Generator Batteries in this segment.

Industrial

Here they serve batteries for heavy duty applications like:

- Railway, Telecom, Solar

- Power and Infrastructure Projects

- Industrial UPS

Submarine

They are also the sole supplier of batteries to the Indian Navy.

Financials

For the year FY 19-20

Numbers

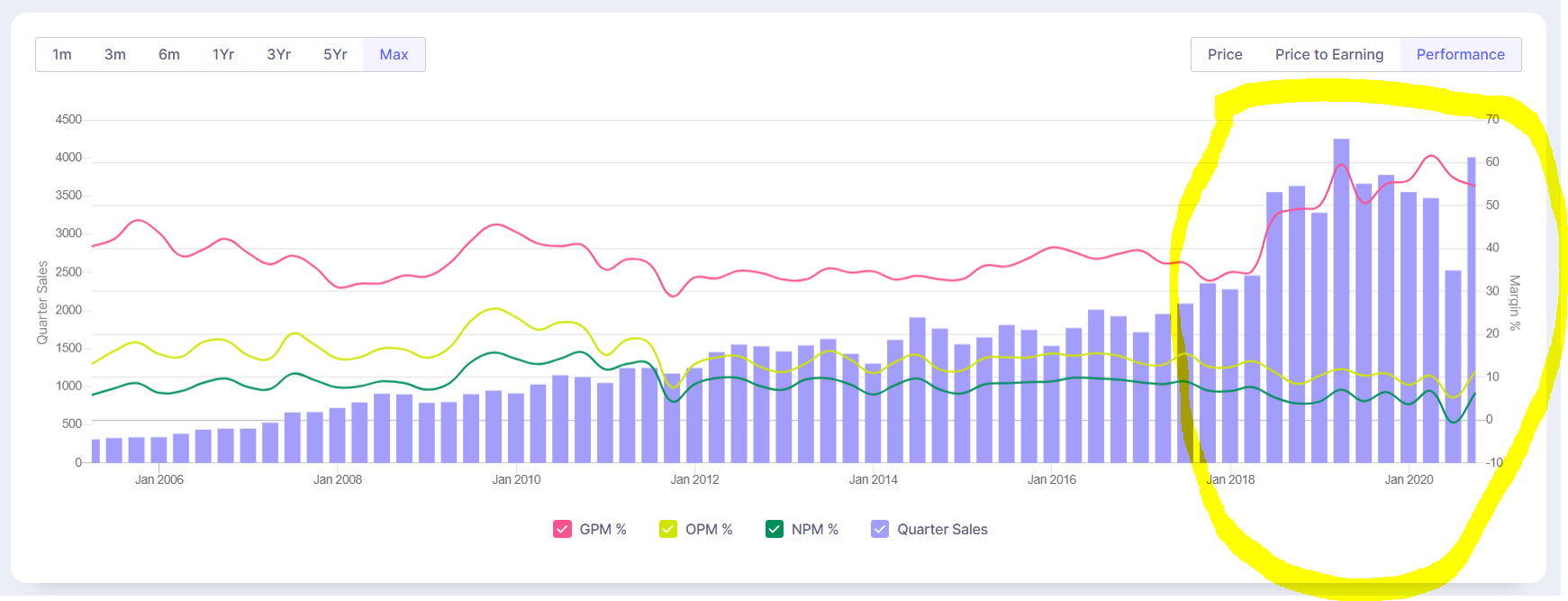

Sales: 9857 Crs

Operating Profit: 1367 Crs (13.86%)

EBITDA: 1111 crs (14.51%)

Interest: 11 Crs

PBT: 1035 Crs (10.5%)

PAT: 826 Crs (8.38%)

Growth

(in CAGR)

Sales: -6.9% 1Y, 9.14% 3Y

Profit: 2.13% 1Y, 6% 3Y

EPS: -8.4% 1Y, 5.97% 3Y

Ratios

ROE = 13.11%

ROCE = 16.44%

ROA = 10.04

The numbers were bad during Q1’21 because of the lockdown, but have bounced back decently during Q2’21.

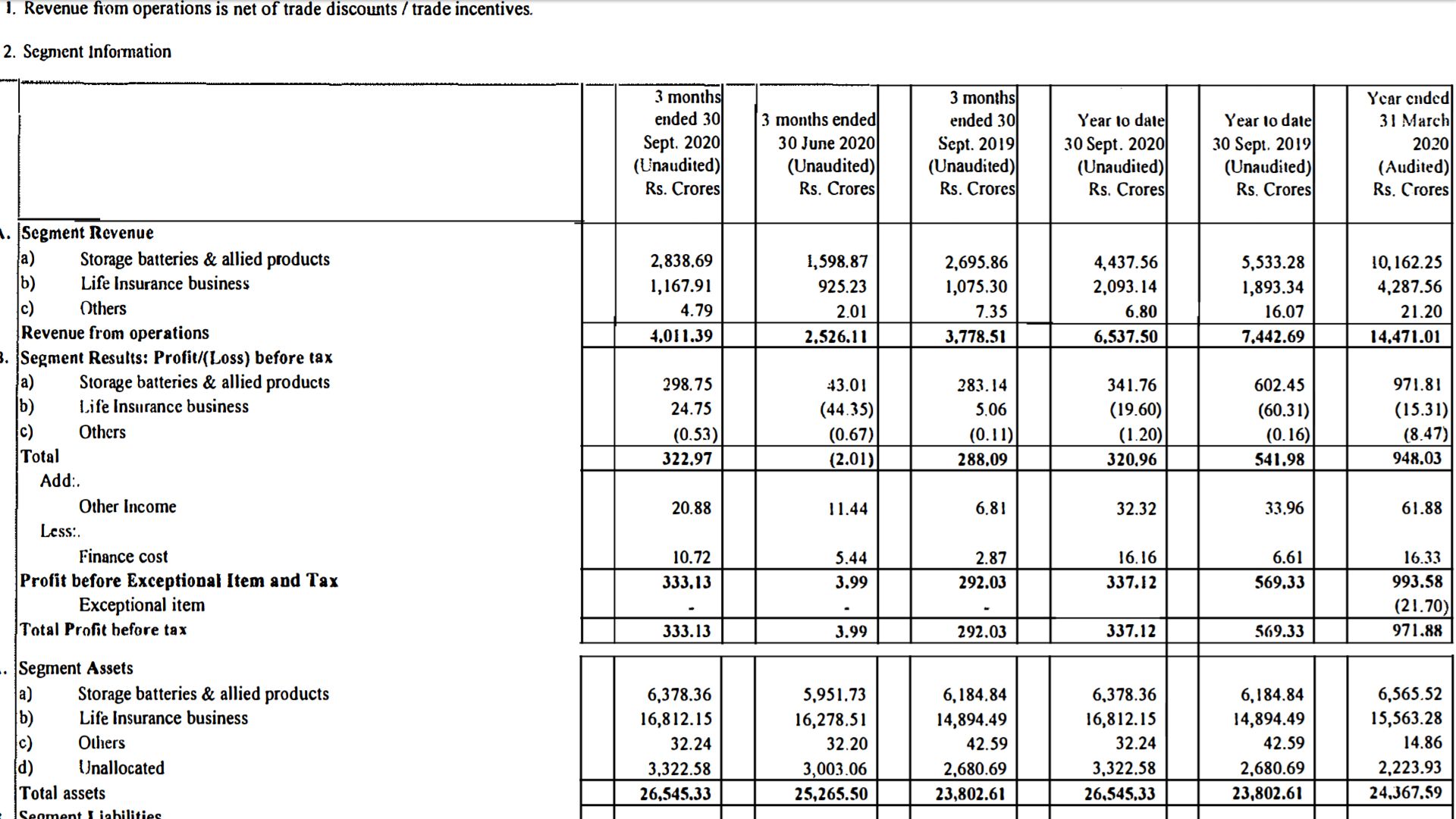

Consolidated

Main reason I didn’t give the numbers for the consolidated report above was because of their Life Insurance business. I didn’t know how to value a Life Insurance company properly, so I looked up online and had to study the business separately.

From the annual report,

AUM: 15700 Crs

Premium Collected: 3220 Crs (10.37% up from previous year)

From ELI’s latest Public Disclosures,

Shareholders Funds: 1850 Crs

Policyholder Funds: 15549 Crs

Embedded Value: 2540 Crs

Expense Ratio: 25.30%

Premium Income Distribution

First year = 17.5%

Renewal = 79.6%

Single = 2.8%

As far as I’ve seen all the numbers are not very big but decent. Embedded Value is growing slowly. Since the Premium income does not belong the shareholders, it must be stored in the Policyholders funds until it’s not further required, which means the LIs would take some time to show profits.

Other Notes from AR

- Exide Leclanche Energy Private Limited, a new JV established to to take a leading position in the lithium-ion battery market in India.

- Invested in CSE Solar subsidies to construct, operate and supply solar power for various manufacturing facilities of Exide.

- Anticipating the stricter emission norms due to the new BS6 engine, the company initiated the development of the advanced EFB and ISS batteries in technical collaboration with Moura Battery of Brazil.

Comparison with Peer

On comparing with it’s closest peer, Amara Raja Batteries:

- Sales hasn’t grown much for both of them especially in the last 3 years.

- Low debt for both the companies

- Exide has better 2W, 4W market share while Amara Raja has better telecom and UPS share.

- Better ROCE (21.88%), ROE (18.08%)

- 24.00% decrease in promoter holding in Amara Raja compared to 0% in Exide

Key Audit Report

- Assesed the provision for Warranty Costs based on historical product failures

- Assesed the estimation of deferred revenue from the customer loyalty program

- Consolidated report included the key audit matter of “valuation and impairment of investments” of ELI where the evaluation methodology was assesed.

One trivial thing which caught my eye was:

In Note 20 Non Current Provisions (Standalone), the provision for Compensated Absences was increased from 31.92 Crs to 36.44 (around 5Cr increase). Is this normal?

My views

Good

- With increasing focus on EVs and Renewable Energy, India along with the world is moving towards a more electric future and I feel Exide has the potential to capture the future demand.

- Low debt, high promoter holding and positive Cash Flow from Operations for atleast 10 years.

- Leading market share in automotive industry.

- Life Insurance business can give an edge against Amara Raja.

Bad

- Topline and Bottomline growth in single digits.

- Amara Raja seems to have slightly better growth and capital efficiency (only thing bothering me in AMRJ is their low promoter holding).

- Life Insurance business has tail risk.

Disc: Invested.

Also thinking of dividing future investments across Exide and Amara Raja.

P.S This is my first post here in ValuePickr and since am not from finance background please point out if there are any mistakes.