Exide-Is Turnaround on the cards?

Just a brief as the Industry will be well known to members here due to Amara Raja.

Exide Industries is a leading manufacturer of lead acid batteries for automotive, telecom, traction, UPS, naval, and motive power markets, Its a duopoly market, Exide a major player with Amara Raja fast catching up and sufficient space for both to grow in the industry, further the growth in replacement market in Automotives is high, importance of distribution in this industry is relevant (Exide having a good hold in both areas and also original Equipment segment). Further with its launch in the home UPS segment around two quarters back with focus to consolidate and increase the presence here, the theory of the inevitable need of an UPS (sufficient addressable market) also plays here. No doubt the company will have to fight harder in this segment.

Well the hammering of Exide on the bourses is knowna may be a few weeks before one could have justified it through an excellent comparison with Amara raja.

But a few things have changed due to which my attention drifted towards the industry leader. Some may argue why to look here when we have Amara Raja, which is no doubt undervalued as compared to Exide and is perfectly playing on the duopoly theory mechanism envisaged by the members at the forum.

I will compare the cause for dismal performance of Exide (mainly which has lead to the hammering and according to me foremost would be its comparison with Amara Raja) and what has changed: -

Concern: - Pressure on margins due to a spike in the lead prices and currency devaluation

Recent development: - Exide Industries Ltd will raise prices for replacement auto batteries by 5-6 percent due to rising input costs, a company source with direct knowledge of the matter told Reuters on this Friday.

Concern: - Amara Rajaas better technology advantage due to Johnson Tie-up leading to higher battery Life and recommendation from suppliers in the replacement market and also market gain in telecom and OEMs. The point to note here is it is the replacement market which will mainly drive the growth of this industry till order from OEMs and Telecom pick up, in short till the gloom over economy settles. If OEMs pick up it will benefit Exide more due to larger presence.

Recent Development: - Exide Industries has entered into an additional Technical License and Assistance Agreement with Shin-Kobe Electric Machinery Company- Japan (Shin-Kobe) to implement new manufacturing processes for automotive batteries.

Under this Agreement Shin-Kobe will provide Exide the technology and extensive technical support and assistance to enable the company to manufacture quality automotive batteries in its various plants in India. This new technology would enable Exide to not only manufacture superior quality batteries but is also expected to result in cost reduction. Shin-Kobe Electric Machinery Company is a leading manufacturer inter alia of automotive and industrial batteries and part of the renowned Hitachi Group and is a wholly owned subsidiary of Hitachi Chemical Company, Japan.

Concern: - Reducing Market share

**Recent Development: - **Well all the members would agree that market share depends on better product (recent technological tie-up will help), Distribution Network (being a leader the company does have good presence) and Management aggressiveness. For the Last point I will like to draw the attention to Mr. Mukherjeeas Interview after Q3 results and Emkays report on Jan 24.

The response of Mr. Mukherjee to a CNBC reporter

Q: I believe you have had higher marketing costs as well in order to regain the kind of market share that you have lost. Where does market share stand at for Exide now at the end of this quarter?

A: We are slowly regaining the market share and this quarter as well we had regained some market share. It is on the positive direction. We will Endeavour further in the coming quarters to get more market share and get back to our original position which we are quite confident of but it will take its own time.

A point from Emkays Report: )- * The company has gained around 800 bps replacement market share in last three quarters, but at the cost of margins as increase in cost heads were not passed on completely. But now can be passed to some extent due to the price increase.

Concern: - The ING SAGA

Recent Development: )- The one anomaly I donat understand is the market is betting huge on the opening up of the insurance sector and it literally wants the insurance sector to open further. Various reports have been published reflecting how the opening up of the sector will benefit insurance company (Recent IRDA decision to allow insurers exposure to equities up to 15% /faster online insurances etc. etc

Now when Exide sees some bright future ahead for the insurance sector and buys the remaining stake in ING. It is hammered.

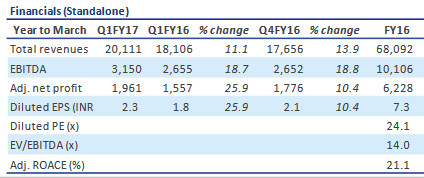

A cursory Look at the Financials of Exide and Amara Raja

The data appears rosier for Amara Raja but figures of Exide arenat bad. Well the focus is not on figures. But to only get an idea and be aware of not getting into next Opto or Arshiya.

**Technicals: - **

First time I heard of something like 50 DMA etc., was at valuepickr from Hitesh sir/Hemant Sir/ Tony and all.

So not getting into it but after some searching some technical experts are suggesting a good upward movement with strong support at around Rs. 120-125 (which may be wrong).

PS: - I have holdings in Amara Raja and I am interested in Exide due to/may be short term gain opportunity.

I would request all the members to discuss this opportunity at the forum so that we can take a wise decision.