Exide Life Insurance business : Embedded value: 1657 in Sep 2015 -> 1870 in Mar 2016 (+12%) -> 1935 in Sep 2016 (+3.5%)

Amara Raja has come out with subdued nos. with higher sales and lower OP, NP which mgmt has partly attributed to demonetization and rising lead prices.

Would be interesting to see how much Exide is affected due to this.

Disc: Invested

Any upside move expected in exide?

Does anyone have Outlook about coming results. Is it worth to enter at the current price. If Any info please share

With high lead prices, Exide’s owned lead smelters may be margin accretive for the company.

Lead price fall : Amara raja & Exide will be in focus.

Lead prices has fallen 11% in last one month from the peak of $2368 per ton to $2099 per ton.

In last two days it has fallen 6-7%.

Exide and amara raja could be in focus as they have taken 10-12% price hike to mitigate earlier lead price increase. (Fwd)

FY17 Q4 and full year results

Dividend of Rs 0.80 / share announced.

Need to understand details of the result from the management commentary in the concall.

Exide Life Insurance today said it has registered a 27 per cent growth in net profit at Rs 112 crore in FY-16, compared to the previous year.

While the new business premium of the company saw a growth of 36 per cent to Rs 863 core, over last year, it said the total premium income grew by 18 per cent to Rs 2,409 crore during the year.

The asset under management of the company also grew by 16 per cent to Rs 11,015 crore during the year, it added.

“We have maintained a consistent growth over the last five years since we became profitable…It has been very strong results, the company met its internal target and will continue to better its performance in the future,” Exide Life Insurance MD & CEO Kshitij Jain told reporters here.

“Our well diversified distribution network coupled with best in class protection, savings and investment plans, helped deliver this growth. We are pleased that this growth has been achieved with no increase in operating expenses,” he said.

Exide Life Insurance that commenced operations in September 2001, has over 15 lakh customers.

The company saidit has over 50000 life insurance advisers in over 200 cities.

Speaking about the life insurance industry, Jain expressed confidence about its growth, with the expected growth in the economy, increasing penetration, and rise in domestic savings due to decline in inflation rate.

Pointing out that the private sector enjoys roughly 30 per cent market share in the life insurance market with 23 private companies, he said Exide Life Insurance being the mid sized player enjoys 1 to 1.2 per cent market share of the entire industry and 2-2.5 per cent of the private sector.

He claimed that during the last year, private sector had grown bigger than State-owned Life Insurance Corporation of India in the individual business category.

from the FY17 AR:

Exide Life:

As at March 31, 2017, market consistent embedded value (MCEV) of Exide Life Ins was INR 2,051 crores against MCEV of INR 1,870 crores in the previous year.

AUM : 11000cr

Premium collected : 2400cr vs 2000 cr

PBT : 112 vs 88

Battery business

700cr capex completed in fy17 at Haldia plant for punched grid batteries. Remaining 700cr capex lined up for fy18.

My Take

Assuming a conservative 2x EV multiple for insurance business, the battery business available for 176 per share

Hi all,

Exide AGM meeting Tommorow …Hope Will get good news and exide will reach the all investors expectation.

Hi All,

Now the Exide Running At P/E 23… Is it right time to buy… ? Please suggest

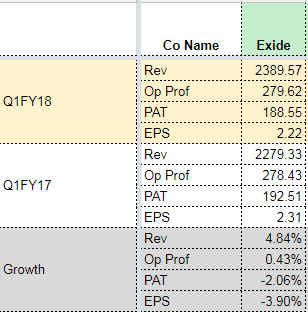

Q1 Results:

Hi ,

After this Q1 Result i expected the CMP will cross 230 but its drastically down…any how its just Q1…

Dada I saw this insurance liability+ investment liability of approx 9000 crores in the B/s. Remember reading earlier that warren buffet used to consider this as a a free float , which he used to make further capex and buying new businesses. If we now compare exide and Amara Raja , I guess exide has a huge plus .

Notes from AGM here → ValuePickr Kolkata - #160 by Pradyumn

Yes, the insurance business is definitely an optionality in Exide. However, what is concerning me is their inability to grow the topline. This is something which I think needs to be monitored closely.

Notes from Exide AGM

Gst neutral as of now in terms of price impact.

Substantial share expected from unorganised because of GST. Using Dynex brand.

7 technology partners. 2 Japan and us. 1 China and Australia

Entered erickshaw market. Using warranties there as a lure. 2.5 million by 2019. And 500000 electric buses. HUGE!

Power rates have substantially increased in some states. Which??

4-6% advantage of price cost by using smelters.

Big guys estimates like Johnson and Hitachi say electric vehicle not to exceed 12% of population by 2030.

Collaboration with American and U.K. Company for energy storage for solar batteries. Major thrust!!

Power excess because discoms don’t have finance to buy it!! So actually no excess.

Metro demand will come down. Tier 2-3 demand will keep strong.

Have got orders for Scorpene submarines. Order next month. Always in touch. Expect orders.

Last year market size in submarine 100 cr. this year size come down. Supply to others like Algeria Chile also. But not very big market. Technologically they have capacity. Very good margins.

Focus on after sales. Say that want to be best in after sales including FMCG. Is that possible??

Nothing final as of now for Exide technology US name dispute.

85% of organised market between top two. Current size of unorganised about 35-40%. A SUBSTANTIAL part should come in about two months?!!

New smelter plant at Haldia. Plants cater to 35% of overall lead requirement. Higher prices better for gaining market share.

Amar raja does have cost advantage due to factories in just two locations.

Business no longer like invest 100 cr and go off to sleep. Have to keep investing continuously. 150-200 cr maintenance Capex. But total expenses to be 400-500 cr average over years.

No plans to sell even part of insurance. Feel this is a sweet spot. So why share profits with anyone. No incremental capital required.

Solar batteries a major segment in future. Prepared for it. No need for more investment.

I have only one question: is this a business with long term tail wind? rest i am not bothered as that would be paralysis by analysis. Views against tailwind invited?

I dont think there is a simple answer to that question. The question itself can be broken down to try to understand what does long term mean. Assuming a period of 10+ years as long term, here are some of my thoughts

- Battery technology will change dramatically over the next years, with more focus on Li-Ion or other new age materials

- With more stable and certain power supply, use of inverters will fall and hence that segment of the business to drastically reduce

- Industrial failover systems will continue to use batteries as backup supplies

- Size and power density of auto batteries to increase significantly, so a auto battery 10 years down the line would possibly look entirely different from what it does now.

- With higher use of shared vehicles through Ola, Uber, Metro rails, overall usage of autos may reduce. Add to it, regulations or disincentives from auto use due to climate change.

In summary, Exide, and batteries in general, are a decent bet from a medium term perspective, but over the long term is very difficult to determine. As of now, for an industry which is not really able to mirror the auto growth in their topline, secular growth is not a given.

Nice thoughts Abhishek, I just have few observations here.

- Auto growth was muted during 2013-16, However we regularly read on revival of auto growth these days. Hence it is a huge positive for replacement sale.

- I am from a small village, from last 10 years we are hoping that we will see a day where we will get access to 24 hours electricity. But nothing significant has changed, we are still using inverters and I assume that we would be using the same for another 7-8 years. (Thanks to poor financial health of Discoms)

- We constantly read on auto sale comparison between china and India. If we can believe that we are going to reach there then this is one of the best story to invest in.

Kindly provide your thoughts.

FY17 annual report highlights

- In FY3/17, Exide commenced production at its new state of art manufacturing facility at Haldia with an investment of Rs7bn. It produces next-generation automotive batteries using new punched grid technology at this plant.

- The company plans to invest Rs7bn capex in FY18-19F to introduce robotics technology at the rest of its plants, so as to improve productivity and reduce cost.

Automotive division performance :

* Exide leveraged its first mover advantage by increasing its product presence in the e-rickshaw battery segment.

* It plans to focus on capturing market share in the unorganised commercial vehicles and tractor battery markets in coming quarters.

Industrial division:

* Exide launched advanced VRLA (Valve Regulated Lead Acid) batteries for telecom applications and started supplying to private operators such as Bharti Infratel and Indus Towers.

* Exide was chosen as a preferred battery supply partner for batteries to GE’s new diesel locomotive plant in Bihar.

Submarine division:

* Exide recorded impressive 39% yoy revenue growth in its submarine division in FY17. It exported two sets of submarine batteries to Admiralty shipyard, Russia and won the first contract for the indigenous Scorpene class submarine battery.

* Management is hopeful of developing new types of submarine batteries and is well prepared to meet future customers’ demands.

New technologies and products :

* Exide is the first to produce batteries using the new punched grid technology in India. It collaborated with the US-based East Penn Manufacturing Company for technical assistance. Battery grids produced using punched grid technology are highly corrosion-resistant, which results in longer battery life.

* Exide launched a range of batteries for e-rickshaw applications. It aims to offer e-mobility solutions for a wide range of applications such as e-vans and e-buses.

* The company has a long-standing technical cooperation agreement with Hitachi Chemicals Co., Japan for a variety of automotive as well as VRLA industrial range of products. Also, it collaborates with Furukawa Batteries, Japan for advanced maintenance free batteries for 4-wheeler and 2-wheeler vehicles.

* During the year, it signed a technology co-operation agreement for the design and manufacture of lithium ion products with Chaowei group of China.