Let me make the case why Excel deserves a study despite this.

Chlorpyrifos, the pesticide in the ban list, is made out of a chemical called DETC.

Question 1: Set DETC revenues to 0, how much is the rest of the company worth?

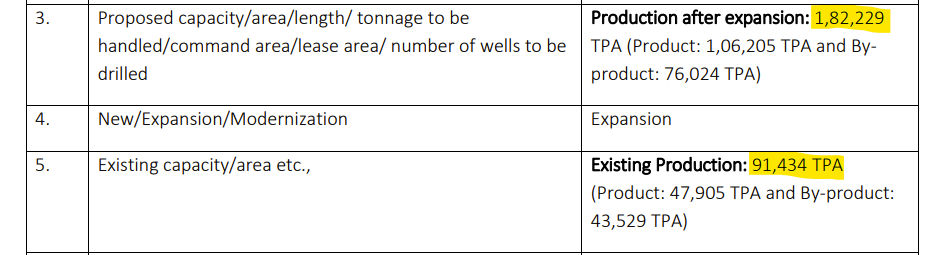

In 2018, Excel decided to expand capacities, doubling the fixed assets:

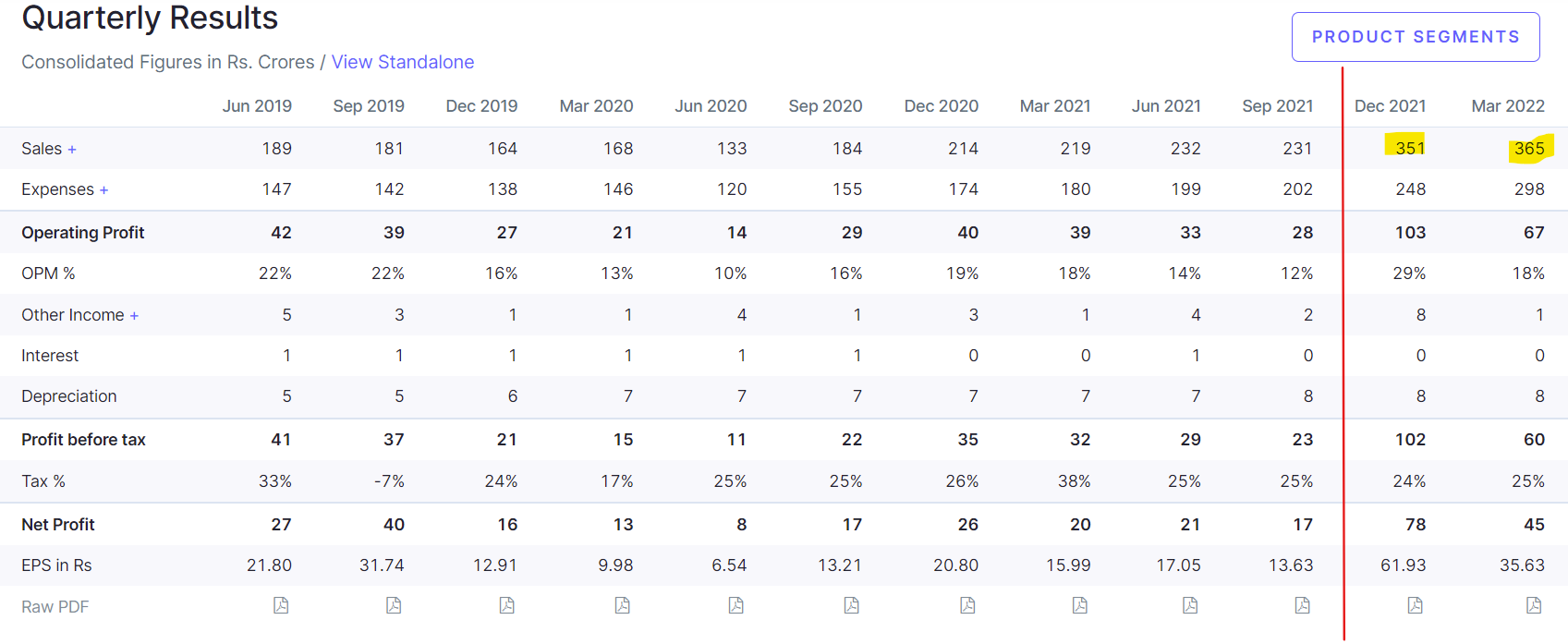

This came live in Q3FY22, and explains the jump in top line in the last two quarters:

Now let’s look at the plant expansion itself:

Before expansion, DETC which goes into Chlorpyrifos forms 31.8% of the chemicals produced annually. Post expansion, it forms 24.4% of the chemicals produced.

In addition, Excel produces some intermediates before DETC. Revising some basic chemistry, here’s how DETC is made:

Phosphorus Pentasulfide + Ethyl Alcohol → Intermediate + Chlorine → DETC

You can see Phosphorus Pentasulfide in number 3 on the table above. This process is also confirmed in their raw material requirement:

D. Spirit is another name for Ethyl Alcohol (has impurities added to it to prevent people from drinking it recreationally).

So taking P2S5 + DETC as DETC allied products, the total amount of DETC allied products before expansion forms 67% of the chemicals produced, and 49.87% post expansion.

This is a large portion of the pie, but in reality, P2S5 is used for other chemicals too, not just DETC so it’s up for discussion if you want to include P2S5 in the DETC pie.

A number of chemicals have also been added to the plant’s capacities including DMPAT, more PSCl3, a number of pharma intermediates and speciality chemicals that could potentially be low volume high margin.

Open question: can we work out the end uses and margin profile of everything else that isn’t DETC?

Question 2: Will Chlorpyrifos be banned immediately, or in a phased manner?

There are several articles that suggest the goverment’s move to ban chlorpyrifos could be brought out in a phased manner over 3-5 years. Other reports suggest the committee investigating the 27 pesticides have only just met to deliberate, and there are delays due to change in officials. In an environment where food security is crucial, will it be the government’s priority to have stability to the pesticide sector?

CRISIL thinks it will be phased, but I wouldn’t trust just one source.

Question 3: Is Chlorpyrifos the only use for DETC?

CRISIL also tells us that the management is actively selling DETC to non Chlorpyrifos uses:

Open question: Can we work out the TAM for DETC excluding Chlorpyrifos? Remember that is an intermediate, while the final pesticide is in the ban discussion. What are the other end uses, and the breakup of landscape?

Ultimately, this company is trading at a PE of 9, and the next two quarters should see growth on account of the new CapEx.

In addition to this, company is debt free and has investments of 500 Cr., 33% of the market cap and is even cheaper considering this.

Disclosure: I have a tracking position. There are hundreds of companies to understand, and not enough time to dedicate to all of them

I would have liked the new capex to have been a complete shift away from DETC, but it was planned in 2018, well before the ban discussion.

@harsh.beria93 as the resident agrochemicals expert, would appreciate your thoughts too!