Finally exited my position completely today after a long wait. Management seems to have no clue on what is happening with the business and the recovery timeframe. The MD keeps asking the CFO even when basic questions are posed to him on concalls which seems very immature.

1 Like

Depends on CV sales momentum and the uptake of CNG by fleet operators. Diesel prices may have been hiked by now but the approaching elections will likely override our stated free pricing mechanism.

The promoter sounds quite clueless about numbers. In every call, analysts ask projections for that year. Not a question, one doesn’t expect. How can one bungle up on that? There was no update on PV segment either. This company needs a capable management and then things will be very different.

1 Like

compressed biogas production in negligible in India… nobody will benefit !!

If GOI offers a MSRP and guarantees offtake, then all roadside trees, paddy straw etc will be used more effectively. Even wet garbage in cities would have a market

International LNG prices are coming down again… by next year it should be at pre-COVID levels… that is going to benefit EKC and all players in the CNG business.

For long term EKC is good as Hydrogen is also going to require Jumbo cylinders which EKC makes.

Not now but in long run it will.

but there are many competitors waiting for this opportunity like supreme and time technoplast.

2 Likes

He has always wavered with his guidance and gives extremely vague answers to questions.

1 Like

EKC is not selling hydrogen cylinders for trucks… its only CNG as of now…

1 Like

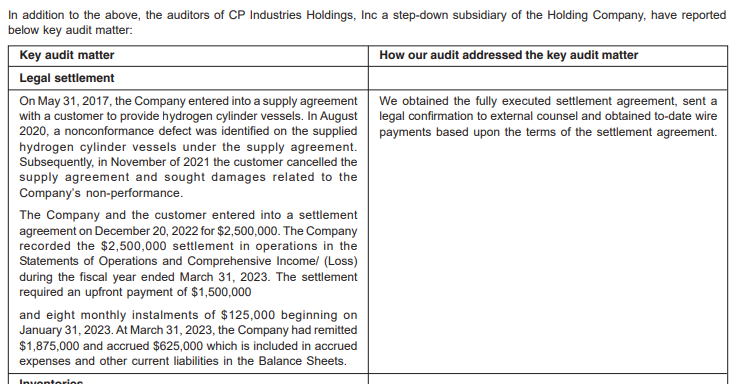

This is an extract from Annual report 2023. There is one more red flag. Supplied defective hydrogen cylinder to Customer.

This also exposes company’s flaw in QA/QC procedures. 300bar is very high pressure and can cause big accident.

My note: It is too heavy to end user to transport 300 bar pressure steel tanks. It can be used for hydrogen storage only. It can not be used in trucks and other automobiles. Tanks made of composite materials is better alternative.

2 Likes

Fully agree… steel cylinders will used for stationary H2 storage - similar to CNG cascades. EKC could not capatalise on the CNG demand which is a core segment for them… i doubt they will be able to supply hydrogen cylinders !!

1 Like

only from stock market point of view… have a look at monthly delivery volume of EKCL. pl note the free float is only 23%. Any comments

volume on 5th feb - 70 lacs !!

Steel cylinders are used in CNG fuelled vehicles. Your suggestion is that hydrogen vehicles won’t use steel cylinders. I would think you have deep domain expertise and understand usage trends well.

1 Like

I feel the results were excellent when compared to the previous few quarters

Revenue grew by 28% to 329 Cr YoY

EBITDA grew by 255% to 51 Cr

Margin at 15.6% vs 5.7%

Net Profit at 36 Cr vs -17 Cr loss

1 Like

Results were in line with expectations as per previous call. Seq revenue is up 10% and EBIDTA is up from 13.7% to 15.8%. Q3 Con call will give more details on composition, outlook and any development.

1 Like

Quarter on Quarter should have been better if the current price is to be justified. At growth rate of 10% annual EPS will be at best 12 implying a price of 120 to 150.

They had invested 50cr in the new plant and the current plants are itself 60% utilised. the story seems to be have been lost… huge opportunity lost.

even egypt and hungary projects not taking off. USA performance has been mediocre for many years.

Concall is a waste of time… for both investors and the management !!

2 Likes

Everyone is angsty when it comes to EKC and it is not because of the business, mostly it’s on account of the management. Promoter appears clueless on calls, shows little sense of numbers, has to be fed with data by colleagues, mostly gets back saying don’t have the number in front on me, etc.

However, the business is such that even a not so top-notch management can run it. It operates in a segment that has long-term tailwind albeit with some amount of volatility that is cascaded down on account of gas and oil price fluctuations.

10% seq (QoQ) isn’t bad, could have been better for sure, no one’s arguing that. From prospect wise, outside of favourable externalities like material diesel-CNG price differential investors hope something materializes in PV, Hydrogen segments.

2 Likes

Hydrogen is quite far away - for all companies. CNG is an existing opportunity which they are not able to capture… very poor management. like i said this stock have become a punter stock…