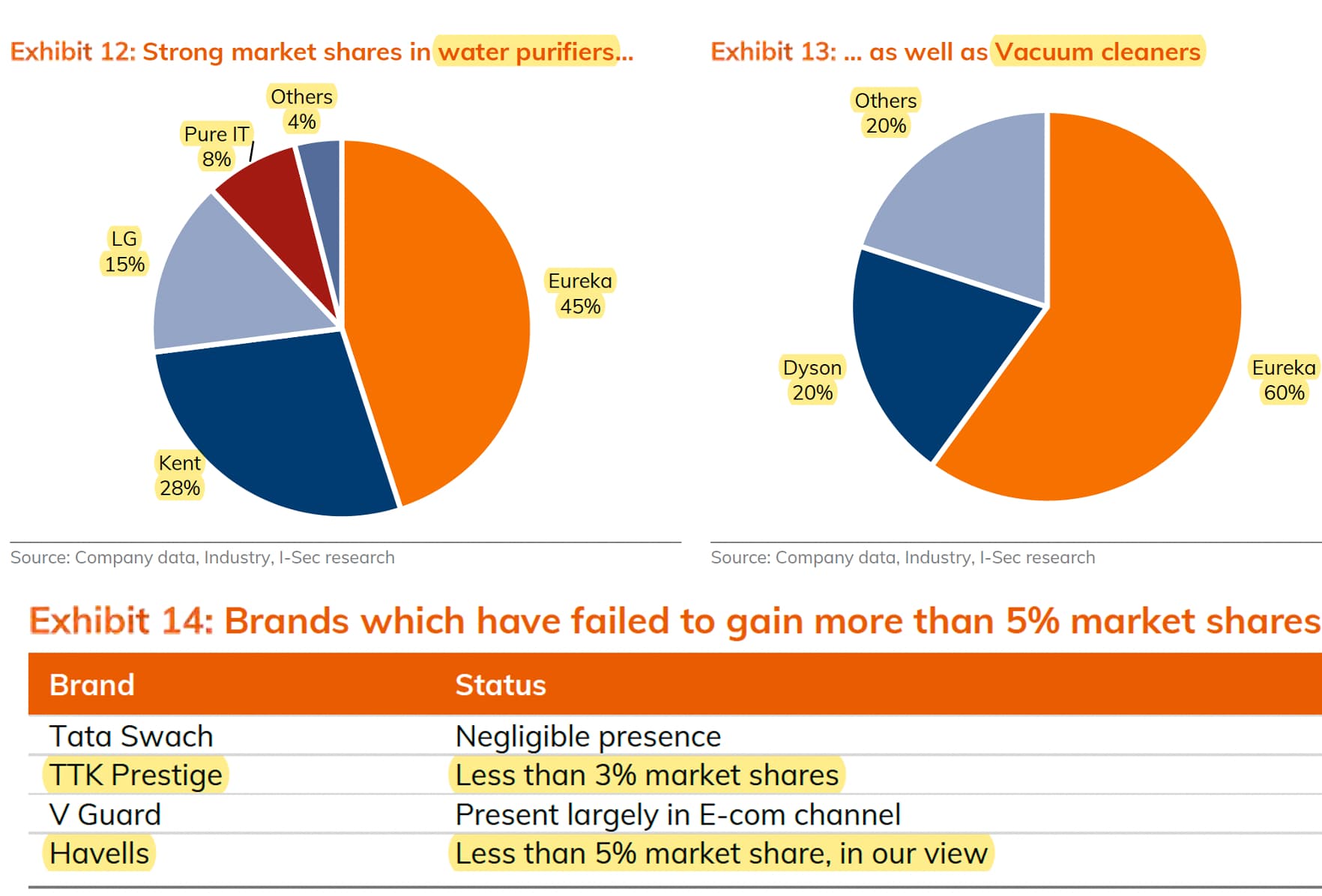

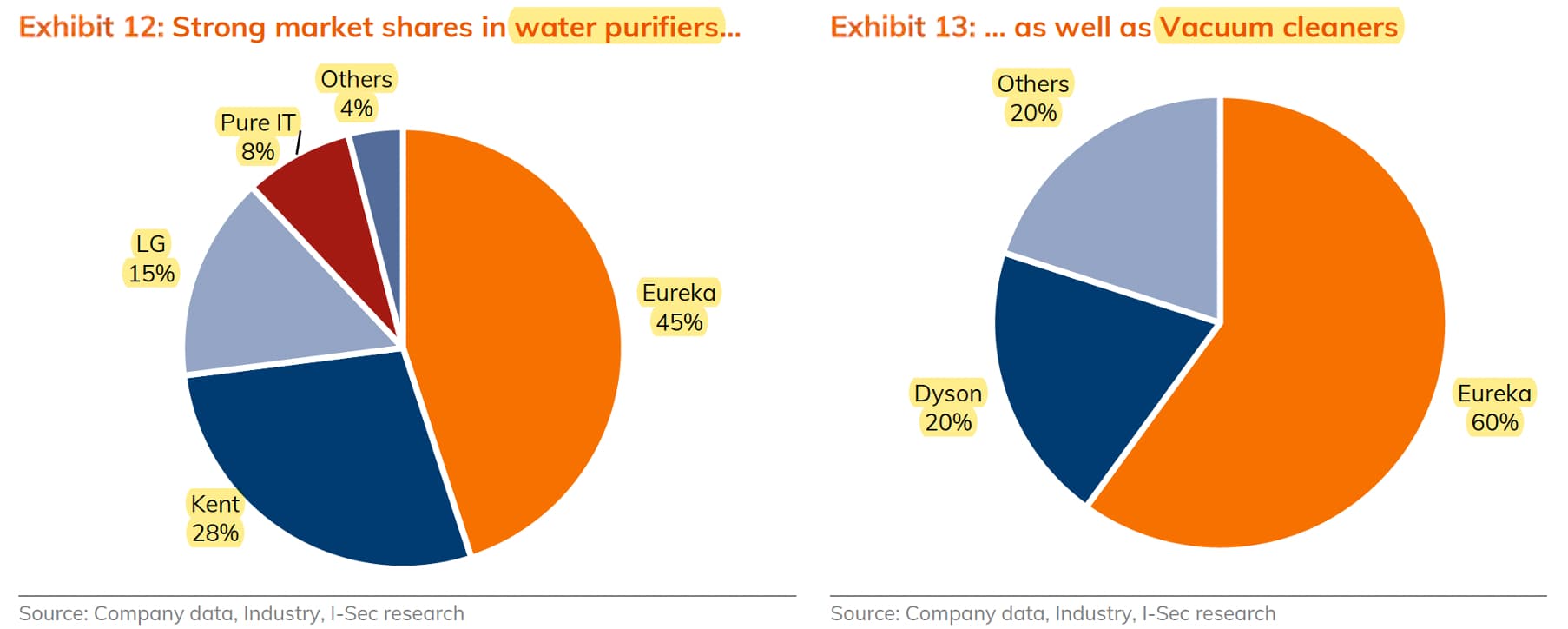

Eureka Forbes is an Indian consumer durables company selling water purifiers, vacuum cleaners, and air purifiers. They are market leaders in water purifiers (Aquaguard brand, 45% market share) and vacuum cleaners (Forbes and Euroclean brands, 60% market share).

History of the company (courtesy Kotak Institutional Equities):

Following the promoter change, Advent brought in Pratik Pota (ex CEO of Jubilant) who has turned around their operations. He completely changed top management, reduced their work force, reduced price point of their products, and drove volume growth.

Management change

- Private equity major Advent International acquired 72.56% stake in July 2022. Advent recruited Mr Pratik Pota, former CEO of Jubilant Foodworks, as new MD & CEO in August 2022. Mr Pota has added a high-quality team of senior management, who have been incentivized with a generous and inclusive ESOP plan comprising 14.9 mn stock options (8% of EFL’s current share count, and covering employees down to the manager level) awarded in 1QFY24 (generally with a strike price around the current market price).

Key Products

Revenue Bifurcation (FY24)

- Electric Water Purifier 42%

- Vacuum Cleaner 14%

- Service 36%

- Others 8%

Water Purifiers:

- Market leader with ~45% share and 65%+ mindshare.

- Sold over 8 million units; large portfolio (50+ SKUs).

- Recently launched rental/subscription models and tiered AMCs (Annual Maintenance Contracts).

- New variants launched at entry-level price points (~INR 6,499).

- Sub-brands include Sure and Select.

See the picture for understanding market share distribution (courtesy: ICICI Securities)

Comparison with Kent

- Kent RO sells its spare parts to distribution partners, who in turn are responsible for servicing activities; hence Kent incurs no service charges. As a result, service charges (14% of sales) are higher for Eureka and is non-existent for Kent. Eureka and Kent both make ~60% gross margins.

Vacuum Cleaners:

- Market share leader (~60%); sold under Forbes and Euroclean.

- Robotics and upright cleaners growing rapidly (>100% YoY growth).

- Retail channel breakup: Most sales happen via electronic shops. Electronic shops and e-commerce are on rise

Air Purifiers:

- Sold under Dr. Aeroguard and Euroair; facing declining market share.

Distribution & Service

- Extensive distribution: 20,000 stores across 2,400 towns.

- Robust service infrastructure: 8,000 engineers across 19,500+ postal codes.

- Increasing digitization: 80% of service interactions are now digital.

Strategic Highlights

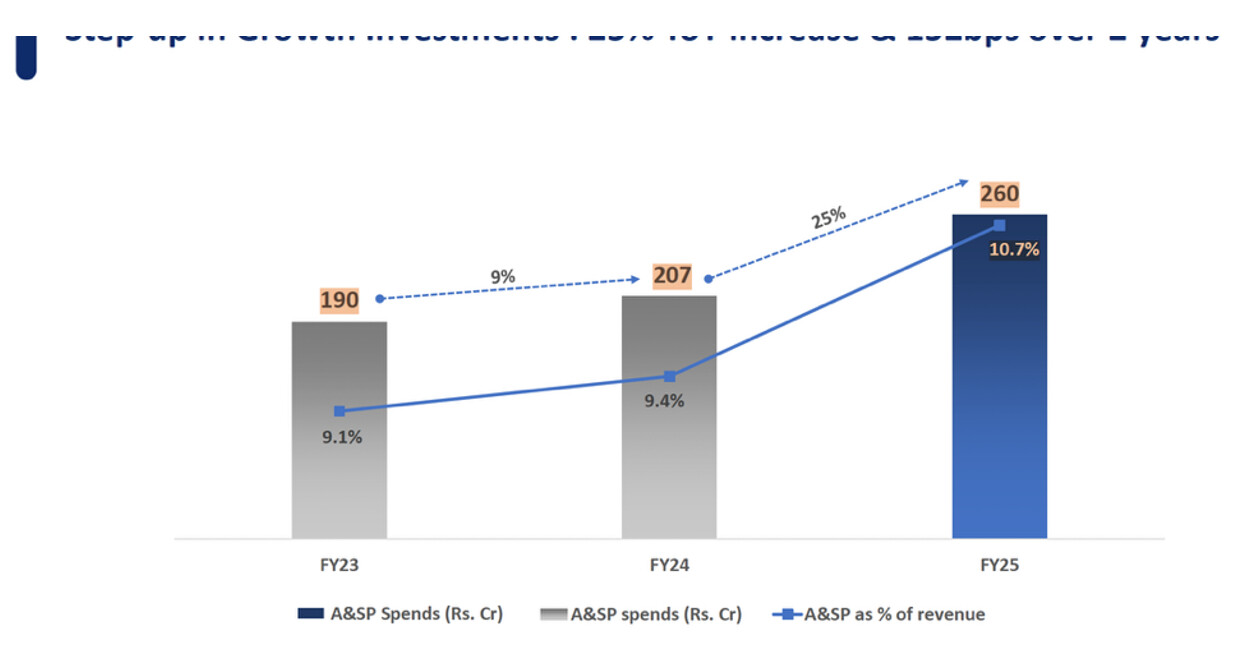

- Aggressive investment in advertising (9-11% of sales vs 2–3% peers).

- Continued cost-optimization via tiered services, extended filter lifespans, and digital service models.

- Focused geographic expansion in South India and Tier 2/3 cities.

- Rated AA-/Stable (upgraded Dec 2024); net cash positive position.

Financial Performance

- Gross margins of ~60%, significantly higher than peers (38-40%). Primary raw material include plastic, copper, and steel

- Asset-light business model with negative working capital and 100%+ ROIC.

- Capex requirement remains low (₹50–60 cr annually); strong free cash flow generation.

- Service revenue (including AMCs) forms 36% of FY24 revenue mix.

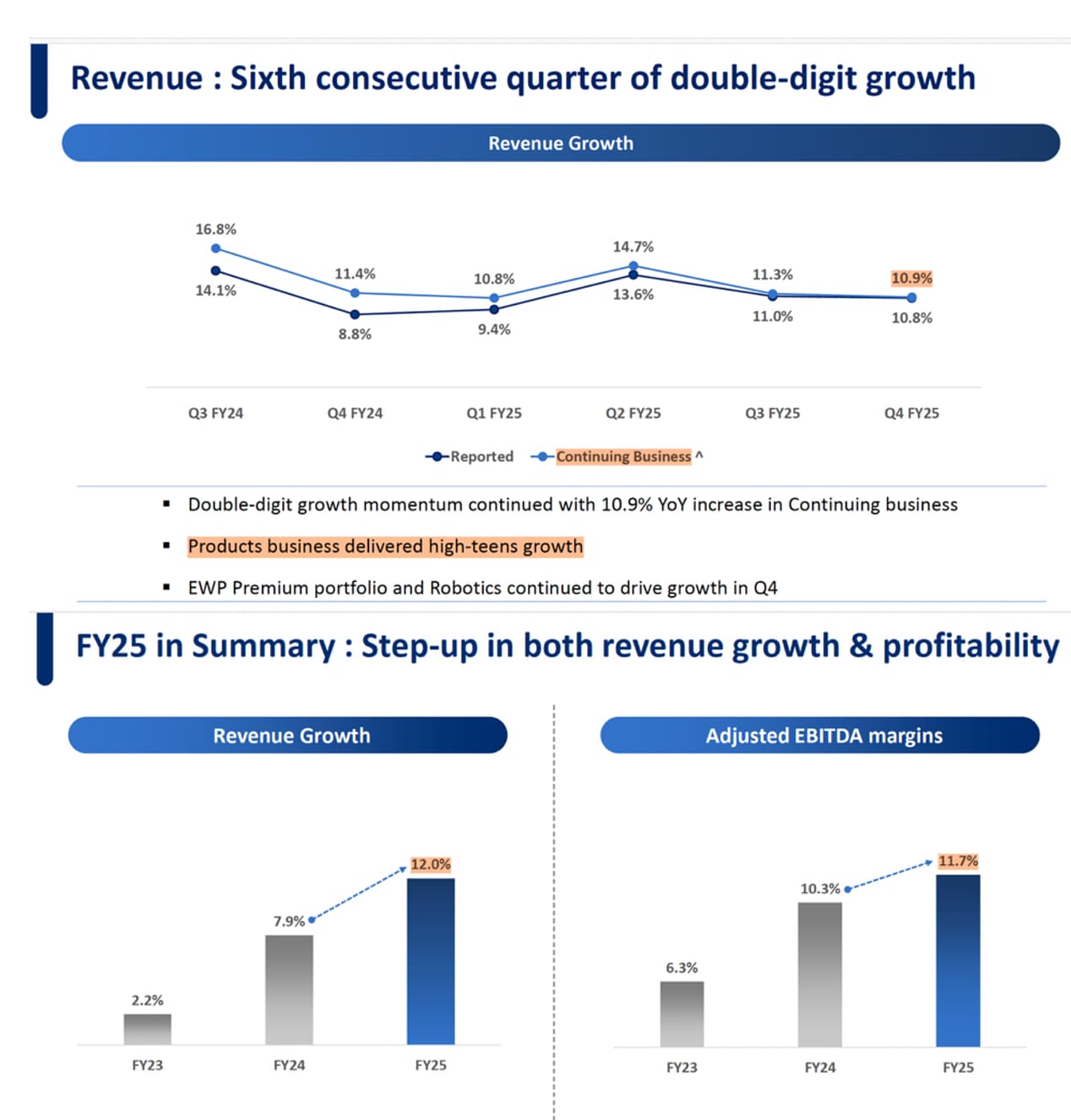

- 6 consecutive quarters of double-digit growth in product division.

Sharing my notes from their last few concalls:

FY24Q4

- E-commerce slowed down in Q4

- Launched tiered and segmented AMCs by offering AMCs at prices as low as 599

- New water filters have a QR code allowing customers to self-authenticate the filters

- Seeing significant increase in the proportion of AMC revenues coming from own online D2C channels with a significant number of these AMCs coming from customers who had lapsed previously and were out of warranty

- On-ground staff is on payroll of their business partners, and not on Eureka’s payroll

- Net cash surplus of 108 cr. vs net debt of 50 cr. in FY23

- ESOP charges were 34.5 cr. in FY24

- One-off charge of 15 cr. was due fire at their Delhi warehouse (insurance proceedings have started)

- Beginning to see initial commodity headwinds

FY25Q1

- High-teen growth in product business, led by double digit volume growth in water purifiers, price increase in water purifiers aided by premium innovations, and double digit growth in service business

- Double digit volume growth in water purifier with some price increase, muted volumes for vacuum cleaners with growth driven by price increase

- Reported continuing business growth was lower at 10.8% because AMC revenue recognition is staggered over the life of AMC (18-20 months), even as associated costs are incurred upfront

- 21% growth in ad spends

- Q2 is their strongest quarter (margins are generally lower in Q2)

- 45-50 cr. Capex in FY25

FY25Q2

- Continuing business grew at 14.7% (4 consecutive quarters of double digit growth) with product business growing by 20%+ (higher growth in modern trade + ecommerce)

- Increased their A&SP spends by 40% (vs 21% increase in Q1FY25)

- Launched aggressive buyback offers to drive replacements and upgrades

- Service charges reduced by 12% due to digital service requests (80% interactions are digital) and operating leverage has started improving EBITDA margins (11% now)

- Expanding AMC by offering lower priced ASP

- Seeing higher growth from ecommerce, South India, and Tier 2 and 3 cities

FY25Q4

- Product business growth continues in high-teens with broad based growth across channels and product portfolio

- Service business saw volume growth in FY25 and they are confident of sales growth happening in FY26 (both in AMC and filters)

- Saw a lot of strategic interventions to reduce cost of ownership

o Launched filters which only require replacement in 2-years

o Tiered AMC categories - Saw operating margin improvement to 13% in Q4 despite higher investments in advertising (see figure below, only significant increase is in advertising)

- Confident that their 60% gross margins will start translating into higher margins. Expect improvement in COGS as they have seen volume growth and can renegotiate with their suppliers

- Business requires low capex (50-60 cr. annually) and generates a lot of free cashflow

- Launched 30 products in FY25

- Robotics as a category is growing at 100%+ in last 3-years. Expect 80%+ growth to continue

- ESOP charges will be 5-5.5 cr. / quarter

Risks

- Advent is a private equity company and they are the largest shareholder, the nature of private equity is that they have to exit at some point. They had sold 10% in Feb 2024.

- With no identifable promoter, company will mostly be professionally run and professionally owned which comes with long-term business uncertainty.

- Eureka’s business model is keeping a large after-sales force which compresses their margins despite having very good gross margins. Kent outscores them on this front, its to be seen if Eureka can reach 20% EBITDA margins.

Disclosure: Invested (no transactions in last-30 days)