Q3 FY22 concall link:-

Revenue/Margins for Europe and Americas are dragging down the overall numbers. Till Europe and Americas start performing again, the company will underperform.

Disc:- Invested.

Q3 FY22 concall link:-

Revenue/Margins for Europe and Americas are dragging down the overall numbers. Till Europe and Americas start performing again, the company will underperform.

Disc:- Invested.

Hi

Thank you for sharing the Concall link. The general guidance seems mixed but fingers crossed the Q4 situation will be better. Related to this I had reached out to Mr.Amit Jain regarding my concern of the debt increase in the company. I was very impressed that Mr.Jain had taken the time to note my phone number and then called me to help discuss my doubts regarding the debt in the company. I was very surprised by the interest and intent shown by the management to assuage the concerns of a regular investor!

Could you please share what did you learn?

Hi!

Below points were shared -

Increase in debt in the quarter is due to increase in CAPEX and Dividend Payout.

Company is not aiming for debt free status, rather focus is on maintaining healthy debt ratios.

NCD of 50cr is long standing and is not related to any increase / decrease in debt.

Cannot provide guidance if debt in Q4 will be lower.

The entire acquisition of Creative Stylopack was done from internal accruals and hence debt is also high.

In general the feeling was that the current level of Debt is comfortable for the company. I am not sure if I agree with that notion as I feel all companies should look at paring down debt as and when possible. Also paying dividends instead of aiming for debt free is a debatable strategy. Please do let me know your thoughts!

I am of the same view that the company should try to pare down the debt instead of paying dividends. The lower interest outgo would improve profitability and hence EPS, thereby rewarding the shareholders. But I am not much concerned about the debt level, given it is manageable. IMHO, the main thing to watch out is if and when the company can improve the Europe and Americas margins. As per the management the margins have bottomed out (not factoring in any covid related issues), so need track if that is the case or not.

With respect to the company entering Brazil, the management mentioned they plan to establish manufacturing facilities there in the future. How far in the future that is, I am not sure. For me there are 3 questions regarding Brazil strategy:-

How much revenue bump they expect from this?

Will it margin accretive?

Will the expansion be funded with debt? (Seems so in my opinion)

Regarding the expansion into Brazil I found it little perplexing given the recent exit from the Manufacturing facility in Russia. Of course these are different markets and maybe it is feasible to address the Russian market from Europe or vice-versa but still it seems a little strange strategy. European margins they have been guiding an improvement since the closure of Russia plant but unfortunately the volatility in RM and drop in Personal Care is not allowing it to move up. Given all the headwinds faced in Europe however one can only hope that the only way is UP.

Good risk reward seen on charts with double bottom pattern. During concall, the management suggested another 1 or 2 quarters to be flat due COVID in China, inflation and war in the European regions. Inviting former members to share their updates & views as well.

Disc. Not invested, tracking.

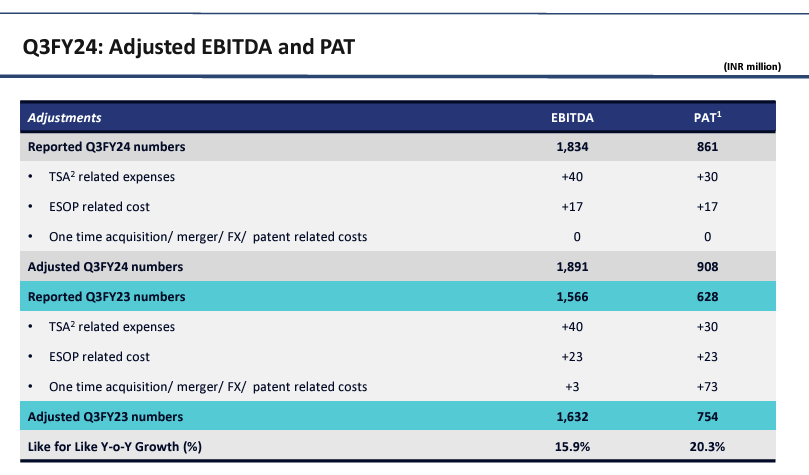

Revenue Growth: 8.6%

do not share volumes

EBIDTA Margin: 15.4% (perv q 15.7%)

Full year

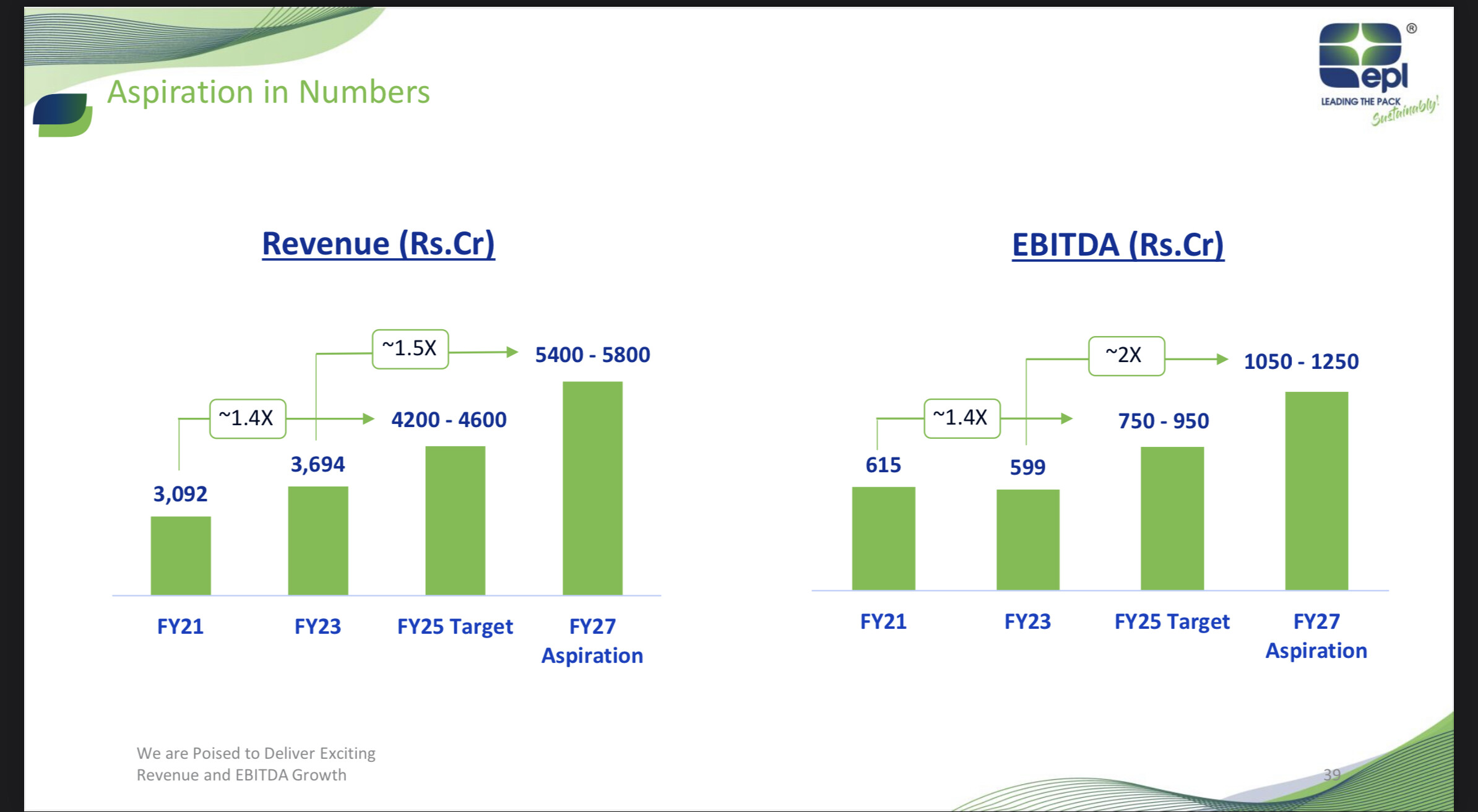

Ambition:

most sustainable packaging company in the world & deliver a profiatble double digit growth

Focus areas to improve bottomline

Brazil Revenues: should kick in from FY24.

‘‘Setting up the factory in Brazil has already been initiated. The objective of the formation of the subsidiary in Brazil is to set up a greenfield project for the packaging tube business’’

The fact is this that we have a long-term agreement with a leading multinational company on the back of which we will be making an investment in Brazil. We are not in a position to tell you the specific details of the quantum of investment; however, our intent is to set up a factory on the ground in Brazil. Our intent is in the full first year of production for the couple of years of production we will begin to make a reasonable margin on that business, but you will appreciate that these numbers are still being developed and I just wanted you all to know that we are going ahead with this project. -Anand Kripalu

Struggling to pass on increase in RM prices to their customers but trying hard to recover.

Disclosure: Invested

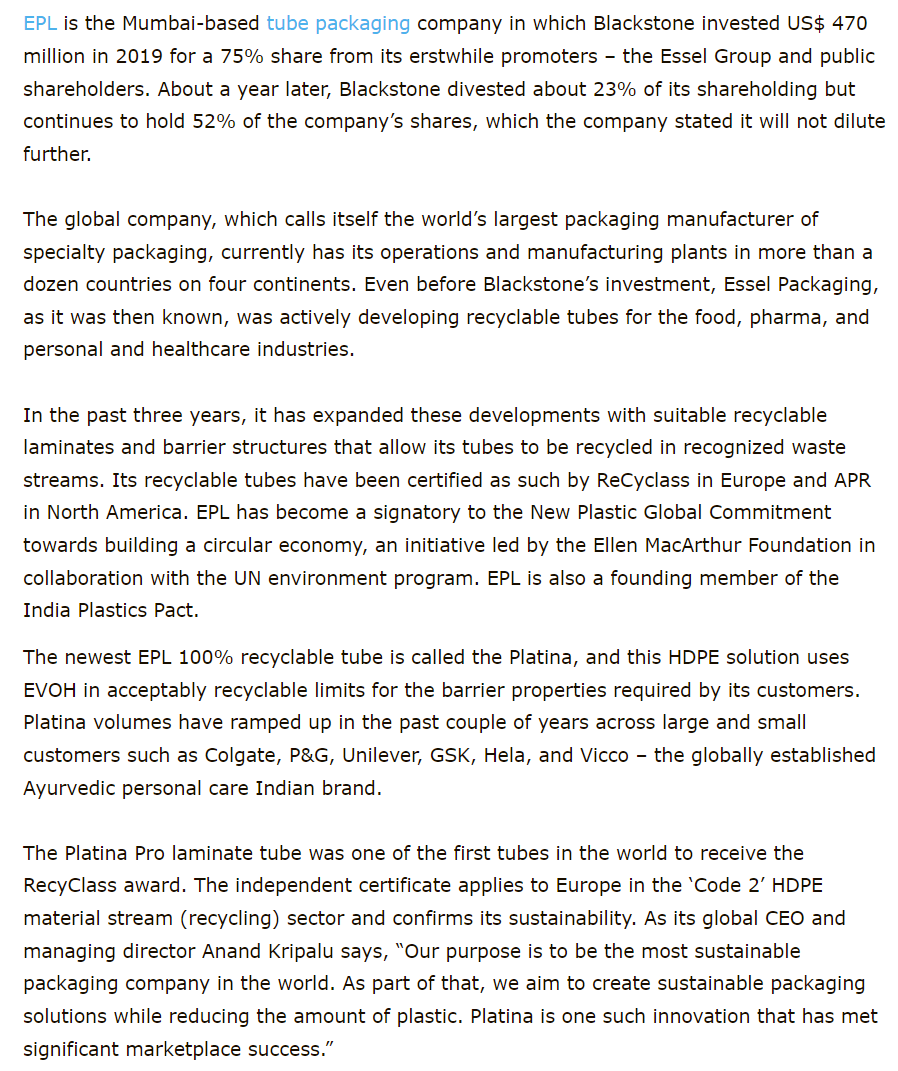

[Platina Pro wins Recyclass and APR certification for recyclability (packagingsouthasia.com)]

https://packagingsouthasia.com/supply-chain-function/design-marketing/platina-pro/

I made a presentation on EPL Ltd. at the VP Meet in Kolkata on 18.06.2023. I feel there’s a high probability of a turnaround in the business as supply side challenges ease, and we’ll be able to see better margins and return ratios in the next few quarters.

Posting a summary of my thesis and attaching the Presentation as well. Please have a look at the pdf for detailed understanding of the product mix, as I had explained that using the slides from the EPL Investor Presentation and Annual Report.

EPL Ltd. - Recovery and Beyond

About EPL Ltd.

Key Data:

Focus on Sustainability:

Future Guidance:

Brazil Plant:

Management Commentary:

Why I like EPL:

Key Risks:

Management interview post Q4 results - Anand Kripalu (MD & Global CEO) - EPL's Anand Kripalu On Revenue Outlook | Midcap Radar | CNBC-TV18 - YouTube

Regards,

Saurabh.

Presentation - EPL Ltd.pdf (1.9 MB)

Hi, recently both CFO, & CS of the company have recently resigned.

Makes me doubt there’s something fishy here (maybe, not sure yet)

Can someone more experienced or having insight help make sense of this?

Hi,

The incumbent CFO, Amit Jain, has been in the company for over a decade. He went from a GM level position to CFO, and has served under both, the Essel group management and Blackstone. The new CFO, Deepak Goyal comes from a Pepsico background, last served Oyo as the CFO, has good experience in FMCG and M&A.

*Deepak Goyal’s Background: *

Mr. Deepak Goyal brings in about 22 years of experience across various industries including Consumer, Financial services and Hospitality tech.

In his earlier assignment, Mr. Deepak has served as the CFO of OYO Vacation Homes, one of the largest vacation home rental businesses in Europe. He successfully navigated the business through COVID-19 crisis, improved revenue realization, optimized cost structures, and enhanced overall profitability. Deepak also led multiple M&A initiatives for the company.

Prior to OYO, Deepak had spent 15 years at PepsiCo across multiple roles including Strategy, FP&A, Controllership, Operations finance and Commercial finance. ln his last role at PepsiCo, Deepak was the Category & Commercial Finance Director where he spearheaded strategic initiative to gain market share in potato chips segment, while maintaining profitability.

–

Spoke to a friend who works at a senior position in Oyo. This is what he had to say:

"On Deepak’s feedback, have heard good things about him after speaking to 3-4 folks over the last couple of days. He is super informed, driven,high sense of ownership and details oriented and had a good rapport with colleagues and sub-ordinates alike. Overall a well rounded personality.

I haven’t worked with him directly as he was heading Finance here for the Vacation Homes business in Europe where I wasn’t involved much .

But have heard good things about him only. I believe he was let go because of our cost structuring mode these days."

Hope this helps clear all doubts.

One additional trigger will come post FY24 is that the TSA fee paid by Blackstone to the erstwhile promoter would go away and that would also lead the PBT to go up 16 cr

Essel Propack Limited Open Offer LOF_p.PDF (sebi.gov.in)

The agreement signed at the time of acq. was for five years which should end in FY24 as the acquisition happened in 2019.

Could you mention the page no. where the fees amt is written. (I was under the impression that it was 25Cr)