About Company:

Essel Propack(Mkt Cap 5450 Cr) established in 1982, is the largest specialty packaging global company, manufacturing laminated plastic tubes catering to the FMCG and Pharma space.

This company is the world’s largest manufacturer of laminated plastic tubes with units operating across countries such as USA, Mexico, Colombia, Poland, Germany, UK, Egypt, Russia, China, Philippines and India.

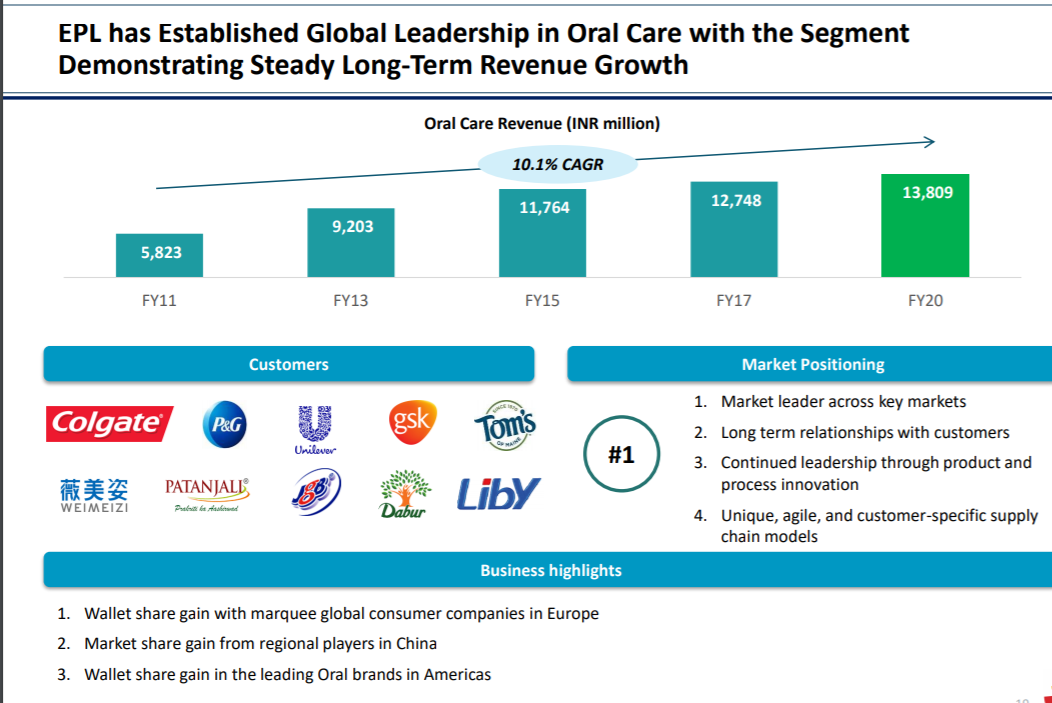

These facilities cater to diverse categories that include brands in Beauty & Cosmetics, Pharma & Health, Food, Oral, and Home. Some of company’s customers are mentioned in the below image.

The company offering customized solutions through continuously pioneering first-in-class innovations in materials, technology, and processes.

Employing over 2852 people representing 25 different nationalities, Essel Propack functions through 20 state of the art facilities and in eleven countries, selling approximately 7 billion tubes and continuing to grow every year.

What is the rationale for investment now?

- Management control has been shifted from the Promoter Essel group to PE firm Blackstone.

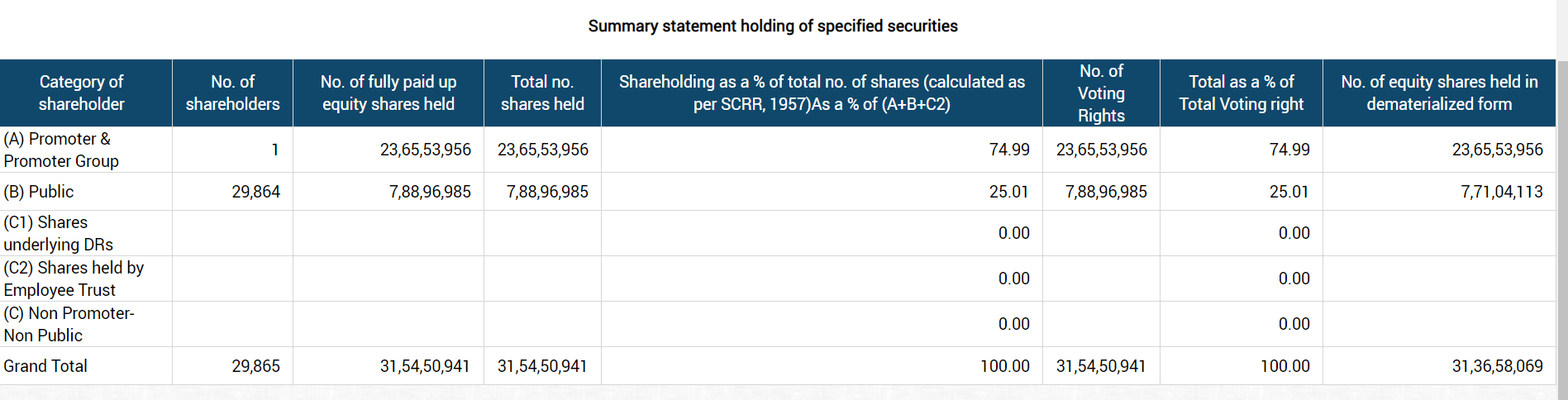

- Blackstone not only acquired the promoter stake but also increased the total share ownership to 75% which is maximum allowed limit via open offer. Below is the latest shareholding pattern from BSE.

- Blackstone is really committed to India. This is what happened after it acquired another Indian firm Mphasis.

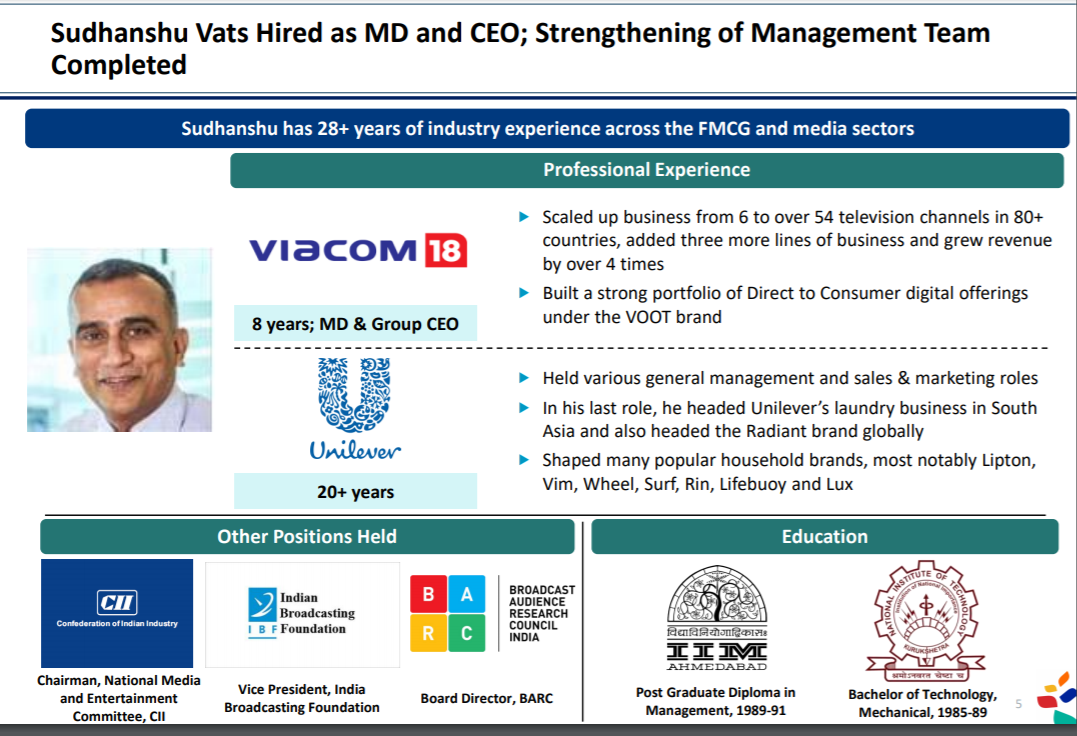

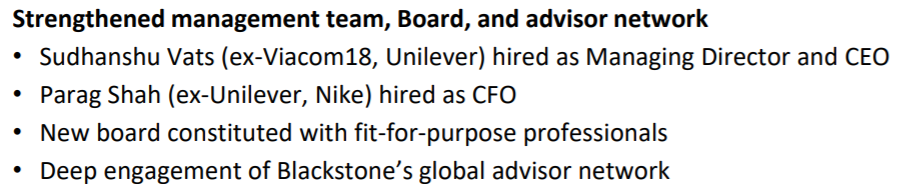

The same is happening with Essel Propacking business. - Blackstone has brought in new professional management. Below is the CEO details from the recent investor presentation.

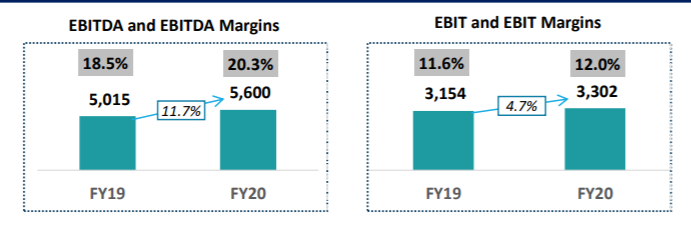

- Margins are impvroing.

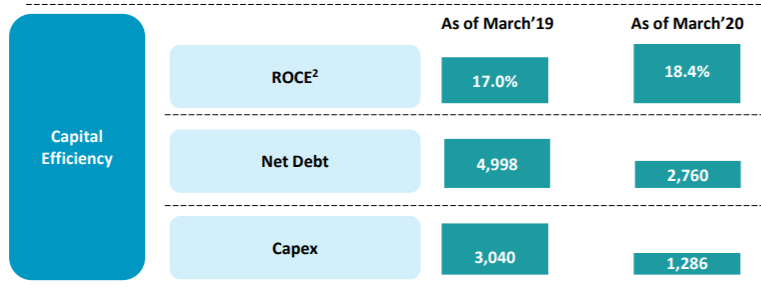

- Return on Capital Employed has improved, Net Debt has decreased and Capex has decreased.

- The company is pursuing various cost reduction initiatives.

- The company is having enough cash reserves to tide the current crisis comfortably.

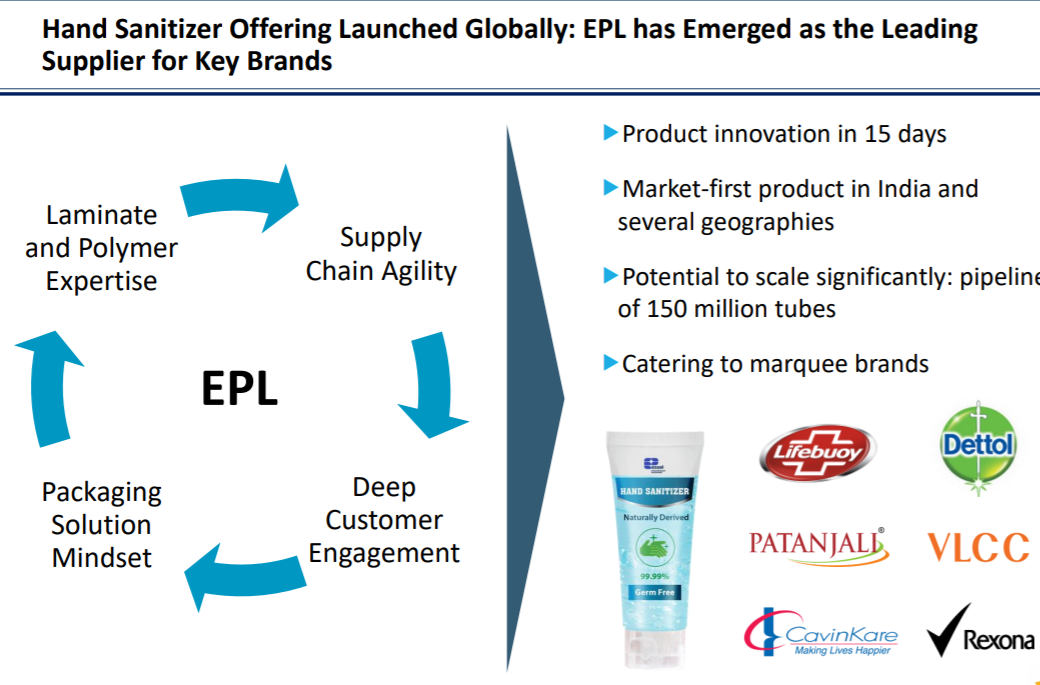

- It’s ready to innovate or to execute when the market demands a new set of requirements. I would not read much into this. But it conveys the company is not beyond the curve.

- Gaining market share in Oral Care.

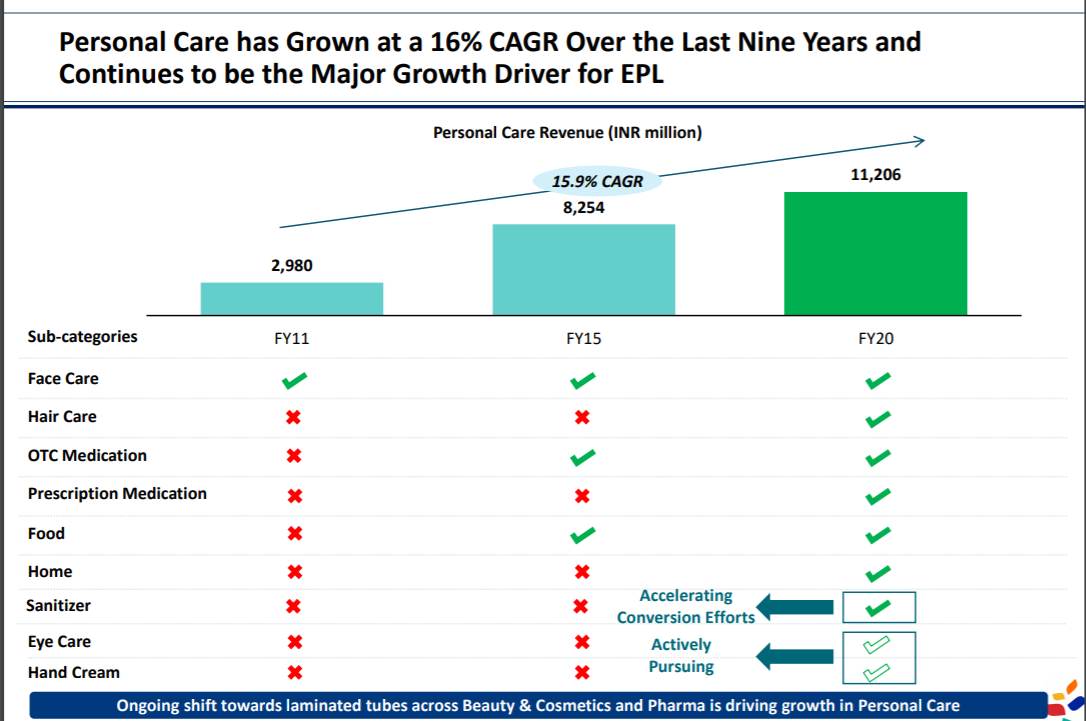

- Has been entering into new segments of Personal Care.

- The Company is conscious of sustainable ESG needs.

- The business nature of the company is resilient in nature.

- The management focus on “Capital Efficient, Consistent Earnings Growth” will create value for all shareholders.

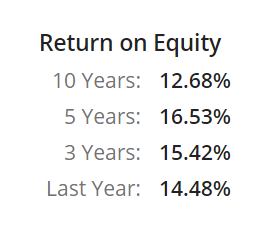

- RoE profile is Ok.

- New management increased the Dividend amount.

- Inventory Turnover is looking good at around 7-9 times.

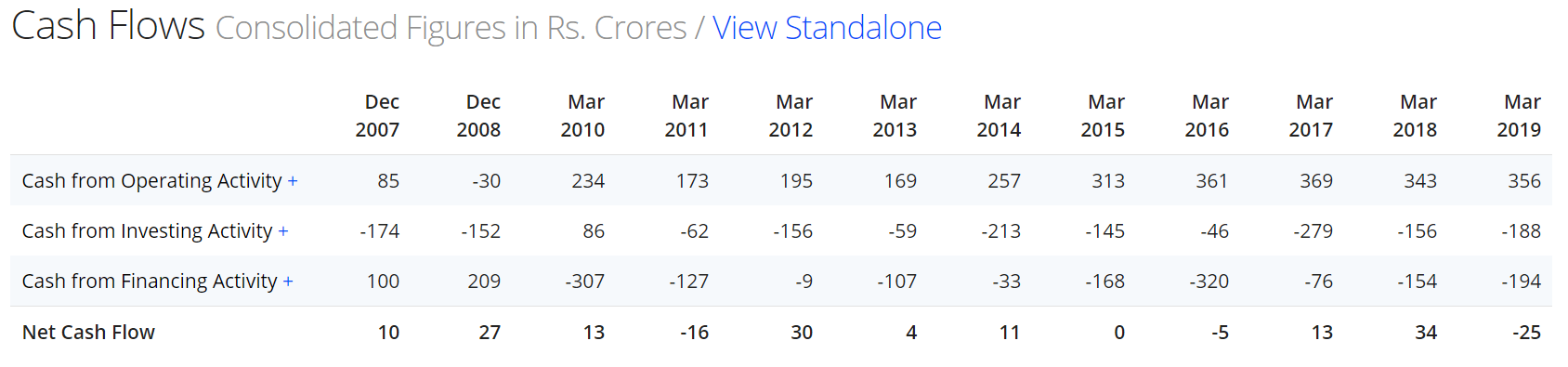

- The cashflow profile is looking good over the last decade.

- Do not see any significant risk to the Balance Sheet. It looks very healthy.

- The company will benefit from lower taxes announced in 2019 by FM.

- Not sure about this. But I am hoping the new management will change the name of the company from Essel Propack to something else considering the reputation of the Essel group. It’s just my wild guess.

I did not study much of the other worldwide packing businesses. Studied some about Indian listed firm Uflex. But it has some Corporate Governance issues. So didn’t pursue much after that.

Any thesis is incomplete unless we know the disconfirming evidence in advance.

Below are some negatives about the company:

- The Company is operating a B2B business. Sooner or later it’s the customer may exert more bargaining power on the company. Not sure about the depth and width of the company’s moat.

- The margin profile is at its peak. Margins are one of the important cylinders for growth to fire upon. This may dampen the growth prospects of the business once it cannot improve thereafter.

- Last 3yr Sales growth Less than 10%.

- Industry valuation multiple are not that great. It’s abysmal.

- The industry seems to be Cyclical in nature only.

- Not enough pricing power to pass on Raw material costs.

- Off late I am trying to stay away from businesses where the company got rated by CARE Ratings. This company has got some instruments rated by CARE Rating. I hope the new management will shift to CRISIL/ICRA soon.

Regards,

Ramesh

Disc: I have a 1% allocation to this business of my Direct Equity portfolio. I have been studying the business to increase it to around 5% after Blackstone acquired it. Till now didn’t develop enough conviction to increase the allocation.