Greetings,

I am a novice in investing and know few basics on investing.

Regarding Employee Stock Options Schemes, I want to understand the implications of an organization issuing stocks to its employees either as a discount purchase or free grants as incentives.

Let us say the Organization has 10, 000 stocks outstanding trading at 100. It has decided to grant 10 stocks as incentives and 10 stocks at a discount of 50%.

As a retail investor, what are the implications of these 20 stocks given to its employees by an organization?

Do the value of the market cap and intern share price reduce by [ 10 + 5 (50% *10) ] * 100 ?

What is the takeaway for a retail investor when the Org issues stocks under ESOS to its employees either as grants or discount purchase?

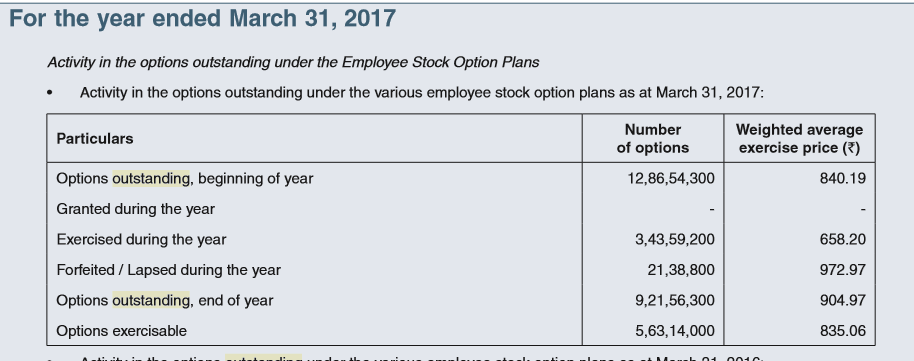

We wish to inform you that the Bank has allotted today 1695600 equity shares to the

employees of the Bank pursuant to exercise of options under its Employees Stock Options Schemes (ESOS).

The paid-up share capital of the Bank will accordingly increase from Rs. 5184130434 equity shares of Rs 2/- each to Rs. 5187521634 equity shares of Rs 2/- each.

The dilution effect is what shareholders will have to complaint about (meaning your ownership is diluted). On all future earnings that company decides to share, you will get lesser pie than you were till yesterday.

In this case, say you owned 100% of Company. After dilution you will be owning 99.935%. Say, company pays dividend of Rs.100000 out of its earnings (assuming that company’s profit remained same), you will be getting 99935 as dividend. You loose Rs.65 to the shareholders whom acquired the shares.

Dividends, Splits, Bonus shares are the typical corporate actions that will affect share price. Share price will not change when shares are issued (ESOPs, ESPP, Warrants) or acquired (Buyback).

Usually ESOPs are not issue. It is regulated and company cannot issue more that prescribed by regulations. “Rights Issue” are the ones that you have to generally worry about. Your actions and inactions will result in loss as a shareholder.

Further to add, the face value of the share is Rs. 2. This doesn’t give much sense. Actually you need to know price of the stock at the time of issue, expiry etc to determine how much you loose as a shareholder.

Long story short, ESOPs is usually not something to be worried about. Warrants, rights issue and acquisitions (non cash) are far worse sometimes than ESOPs.

Options once granted will be credited to demat account of receiver. To give you an example. 3 Years ago, the company would have given options to the employees. The share price then is say 1000. Now the share price is say Rs.2000 then employee would exercise the option. Otherwise the option is worth nothing.

This is more like an incentive and motivate employees to work better. This is how ESOPs work.

The discount part you said, is ESPP. It is usually capped at 15% discount to prevailing market price. The employee gets to buy the shares at 15% discount. He has to pay (85%) cash from his pocket so that he can acquire the shares at discount. This is to encourage employees to show commitment towards company.

ESOS should definitely be accounted during valuing a business. Mike Mauboussin has touched this topic in couple of chapters in Expectations Investing book. Please go through it as I found it helpful.

The reason I said you don’t need to be worried about this is because the incremental allocation as percent of outstanding shares is insignificant. I checked at HDFC bank. The options outstanding is close to 5% of total shares. So if you go by dilution effect, whatever value you arrive you can divide by 105%. All we are talking about here is “value” not “price” or market price of the stock.

Not all options will be exercised. Few of them will be forfeited making valuation complex.

Complicating further, this dilution method is not fair valuation since you will get proceedings from the ESOP which you have to add back in your valuation. This is chicken egg problem since you are valuing company which necessitates it to assume future price.

To summarize, your “incremental” dilution effect by this offering is negligible. If you go by “outstanding” options granted so far, dilution will be in the range of 0% to 5%(worst case)

In most cases, the “value” is more of an estimate. So if you do good homework valuing the company, then finally you have to consider these outstanding options.

The shares may have been issued as incentives, but the receiver can immediately sell them in the market and gain the current market price. Hence, it’s similar to issuing the equity at the current market price. So, this would transform the equation into: