CCI has approved Kubota stake high, Next step open offer will open very soon.

PR63-2021-22 (1).pdf (261.6 KB)

CCI has approved Kubota stake high, Next step open offer will open very soon.

PR63-2021-22 (1).pdf (261.6 KB)

Rakesh Jhunjhunwala stake in Escorts increases vs Dec 2021 quarter

As per recent filing👇

-Current holding 75 lkh shares

-Dec 2021 quarter 64 lkh shares

Absolute increase 11 lkh shares

As per my note open offer started from 14/3 to 28/3?

What action do shareholders need to take?

Thanks

76th AGM was held on 14th July 12 noon.

Medium Term Business Plan to be published sometime in Sept.

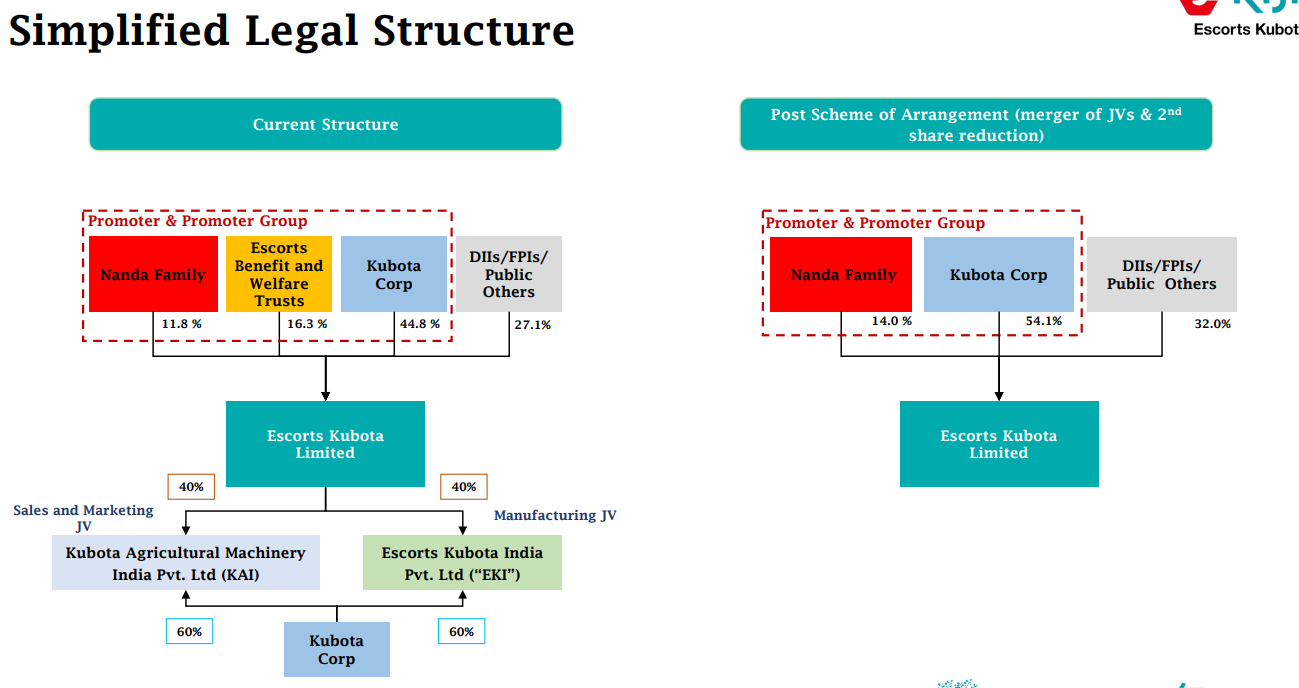

Escorts Amalgamation announcement with Kubota JVs

Summary:

Really bad numbers by Escorts. Big dent in margins & hence net profits. Another big downside candidate for Monday.

The company has shared the Escorts Kubota Mid Term Business Plan Presentation.

Some highlights:

Some unconfirmed news on the counter. I suspected this might be one of the next steps, since the Mid Term Business Plan details in the Auuunal Report were very generic for the Railway business, whereas for Agri they had mentioned definitely plans on capex. Construction Equipment business also am not sure, if they want to retain if Kubota is not having similar products.

We have to wait to see how this benefits minority investors or not. I would have preferred if they demerged this business, distributed shares to minority investors, listed it seperately and then sold the promoter stake to buyer. If its a slump sale, then the cash hoard just increases.

India’s Escorts Kubota mulls sale of railway equipment unit -CNBC-TV18 | Reuters

Now they are opening a NBFC to finance the Company’'s Products and Consumers. Interesting Escorts Finance revoked its NBFC license earlier and has changed that AoA and Memorandum to change the line of business, Alos it was renamed to “Invigorated Business Consulting Limited”

this is not a good development overall. usually, Manufacturing firms in AUTO and CD with finance companies end up pushing sales for their parent at the cost of poor loans at NBFC. off course it helps in short term, but eventually, the parent has to capitalize their NBFC from losses in agri. MMFL /L & T FINANCE BFL _2 W bajaj AUTO PORTFOLIO is a classic case

According to a recent article on Construction Times, the Indian mobile crane industry is poised for growth. Here are the key points:

Current Market Scenario:

Growth Trends:

Future Outlook:

(1) The Indian mobile crane industry will continue to grow in future… The Indian mobile crane industry will continue to grow in future. - Top Construction and Infrastructure Magazine.

(2) Construction Times - Top Construction and Infrastructure Magazine. https://constructiontimes.co.in/.

Escorts Kubota Q1 FY2025 Analysis: Key takeaways!!

Escorts Kubota Limited remains cautiously optimistic about the Indian tractor industry, projecting mid-single-digit growth for FY2025. The company expects a recovery in the second half of the year, driven by improved monsoon coverage, government assistance, better crop prices, and enhanced rural liquidity. However, challenges persist in certain geographies, particularly in South India.

Strategic Initiatives:

Trends and Themes:

Industry Tailwinds:

Industry Headwinds:

Analyst Concerns and Management Response:

Concern: Delay in greenfield facility implementation.

Response: Management is evaluating alternate sites and remains committed to capacity expansion.

Concern: Market share loss in South India.

Response: Plans to leverage Kubota’s strong presence and introduce new products to regain market share.

Concern: Export market challenges.

Response: Developing new products for key markets and remaining aggressive in export strategy.

Competitive Landscape:

EKL faces strong competition in the domestic market but aims to differentiate through product innovation and leveraging Kubota’s global expertise. The company is working on expanding its presence in the premium segment through the Kubota brand.

Guidance and Outlook:

Management expects mid-single-digit growth for the tractor industry in FY2025, with stronger performance in the second half. The company aims for double-digit growth in the railway equipment business.

Capital Allocation Strategy:

EKL is focusing on investments in new product development, capacity expansion through the greenfield facility, and potential co-branding initiatives with Kubota.

Opportunities & Risks:

Opportunities:

Risks:

Regulatory Environment:

The company is preparing for the implementation of new emission norms (TREM V) from April 1, 2026, which may impact product development and costs.

Customer Sentiment:

Rural sentiment is improving due to better monsoon coverage and government initiatives, but liquidity pressures remain a concern.

Top 3 Takeaways:

Hi @Avigyan_Mitra,

I see you have updated results summary for many companies I’m tracking. That’s an immense value addition to those scrips. Thanks for your efforts.

I see you have posted for ACE as well, which is in similar line of business as Escorts. From your concall summaries, it looks like ACE is very optimistic and Escorts is cautious about next few quarters. What’s your opinion?

Sanghvi movers, which is in renting out cranes, posted a muted results and their guidance for next quarters are also not great.

What should we infer?

An investor should always be an optimist but the analyst in you, must always be skeptical about things. My advice will be to study the business environment of the said scrips and check whether these companies are operationally capable to operate in this business environment.

Self research and judgement is priceless.

Thank you so much for your kind words. Good luck.

EKL-Tractor-and-CE-Consolidated-Sales-volume-from-April-2023-to-August-2024.pdf (escortskubota.com)

For Post Amalgamation comparison, compnay has shared a statement showing consolidated monthly wholesales volume of Tractors and Construction Equipment from April 2023 till August 2024 including wholesales volume numbers of the amalgamating companies.

| Tractors | Construction Equipment | |||

|---|---|---|---|---|

| Month | Domestic | Export | Total | Total |

| April 2023 | 9,266 | 313 | 9,579 | 486 |

| May 2023 | 10,409 | 463 | 10,872 | 458 |

| June 2023 | 11,222 | 580 | 11,802 | 522 |

| July 2023 | 6,917 | 409 | 7,326 | 495 |

| August 2023 | 6,439 | 395 | 6,834 | 587 |

| September 2023 | 11,334 | 747 | 12,081 | 627 |

| October 2023 | 14,550 | 563 | 15,113 | 659 |

| November 2023 | 9,503 | 403 | 9,906 | 557 |

| December 2023 | 5,731 | 405 | 6,136 | 792 |

| January 2024 | 6,782 | 368 | 7,150 | 554 |

| February 2024 | 7,269 | 440 | 7,709 | 670 |

| March 2024 | 9,355 | 533 | 9,888 | 734 |

| April 2024 | 8,492 | 347 | 8,839 | 465 |

| May 2024 | 9,906 | 380 | 10,286 | 458 |

| June 2024 | 11,011 | 234 | 11,245 | 459 |

| July 2024 | 6,540 | 423 | 6,963 | 491 |

| August 2024 | 6,243 | 409 | 6,652 | 393 |