| Main Products | Main Customer Industries |

|---|---|

| Welding Consumables, Reclamation Consumables, Arc Equipment, Industrial Gas Equipment, Environment Products, Cutting Systems | Shipbuilding, Petrochemical, Construction, Transport, Offshore and Energy Industries |

| Bullish Arguments | Bearish Arguments |

| Technology and Market leadership position in Welding Equipment industry | Low liquidity stock - higher impact cost in case of larger trades - entry & exit becomes difficult |

| Products command a premium due to higher value-add | Industrial slowdown & lack of capital investments could impact prospects |

| Parent, Esab Holdings UK, is one of the top two globally in welding technology -12% market share | Competition from unorganised sector, cheaper imports and international competitors setting up base in India |

| Strong Balance Sheet together with its technology leadership puts it in a better competitive position to face adverse business cycles | Volatility in raw material prices -raw materials constitute 60% of sales |

| Debt-free, Consistently RoA and RoE >40% , Free Cash flow/Sales >7% | |

| Barriers to Entry | Interesting Viewpoints |

| Brand - Esab is the strongest welding brand | Consumables demand has good correlation with Steel consumption. Industrial and Infrastructure activity pickup are key triggers. |

| Customer relationships - Long term relations built on trust and customised optimal solutions for each client | Wind Energy sector growth @ 25% plus - wind tower manufacture requires extensive use of welding equipment and recurring welding consumables expenditure. Each MW of wind power consumes 700 Kg of weld metal and 600 kg of weld flux |

| Disincentive to change supplier - welding consumables generally constitute 2% of fabrication costs but a weld failure can be catastrophic | After-market business segment comprises more than 30% of sales . Strong focus to build this segment rapidly |

| Technology - Esab has industry leading expertise & products -esp in critical applications |

4 Likes

This sector looks lucrative now. Anyone tracking this?

yes, it looks lucrative and market leader in fabrication technology.

Anyone tracking this company lately, it has been on a significant run for some time now, while its peers haven’t performed that well.

1 Like

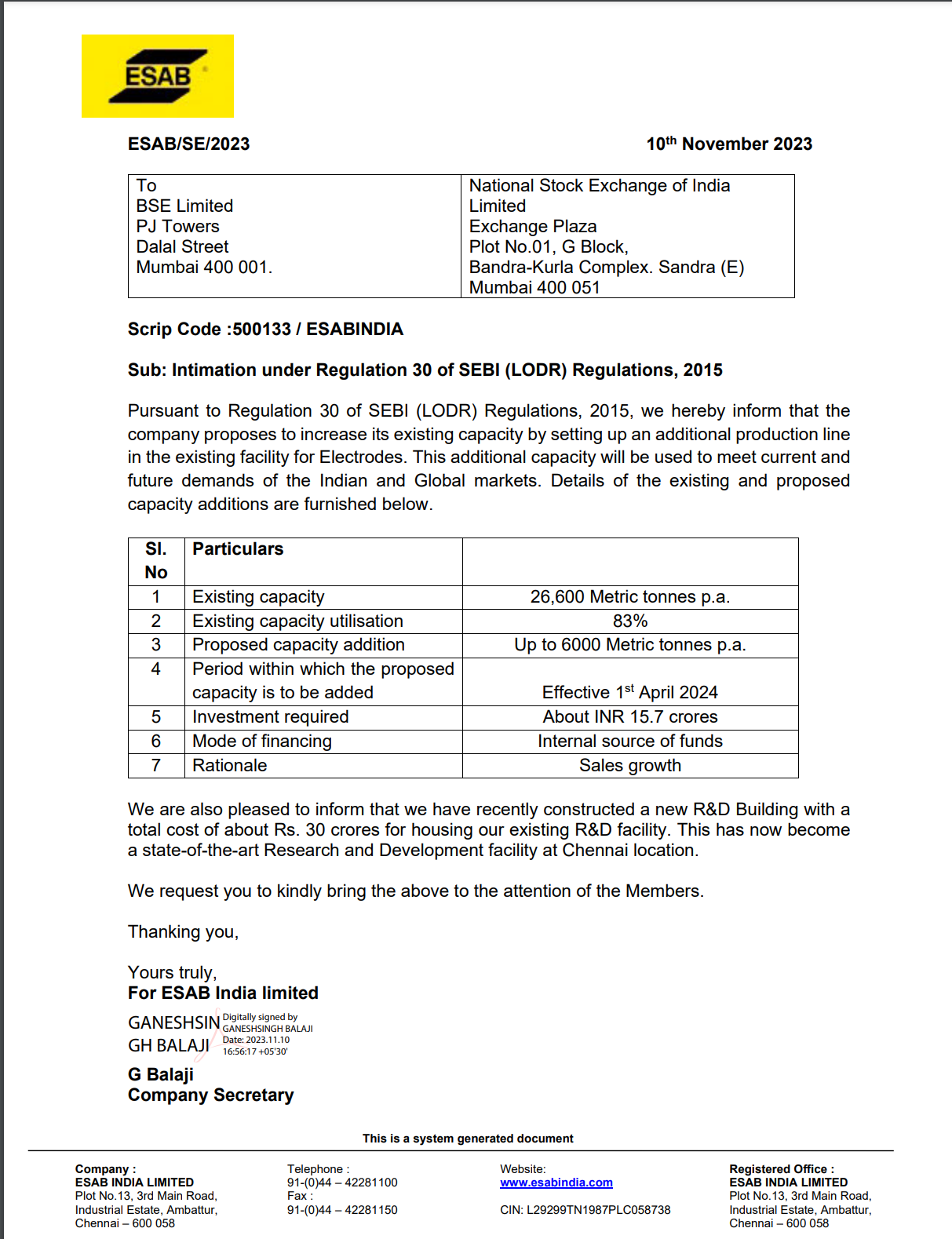

ESAB India is planning to expand their production for electrodes. They’re going to add a new production line to make more of them. This is because they need to meet the growing demand for electrodes in India and around the world.

Here are some details:

- Right now, they are 26,600 metric tonnes of electrodes each year which is using about 83% of their current capacity.

- Company wants to add another 6,000 metric tonnes of capacity which they plan to do this starting from April 1, 2024.

- Costs will be around around INR 15.7 crores, and they’ll use their own money to pay for it. Goal is to grow their sales grow.

Additionally, they’ve built a new research and development (R&D) building in Chennai, which cost around Rs. 30 crores, and it’s now a state-of-the-art facility.

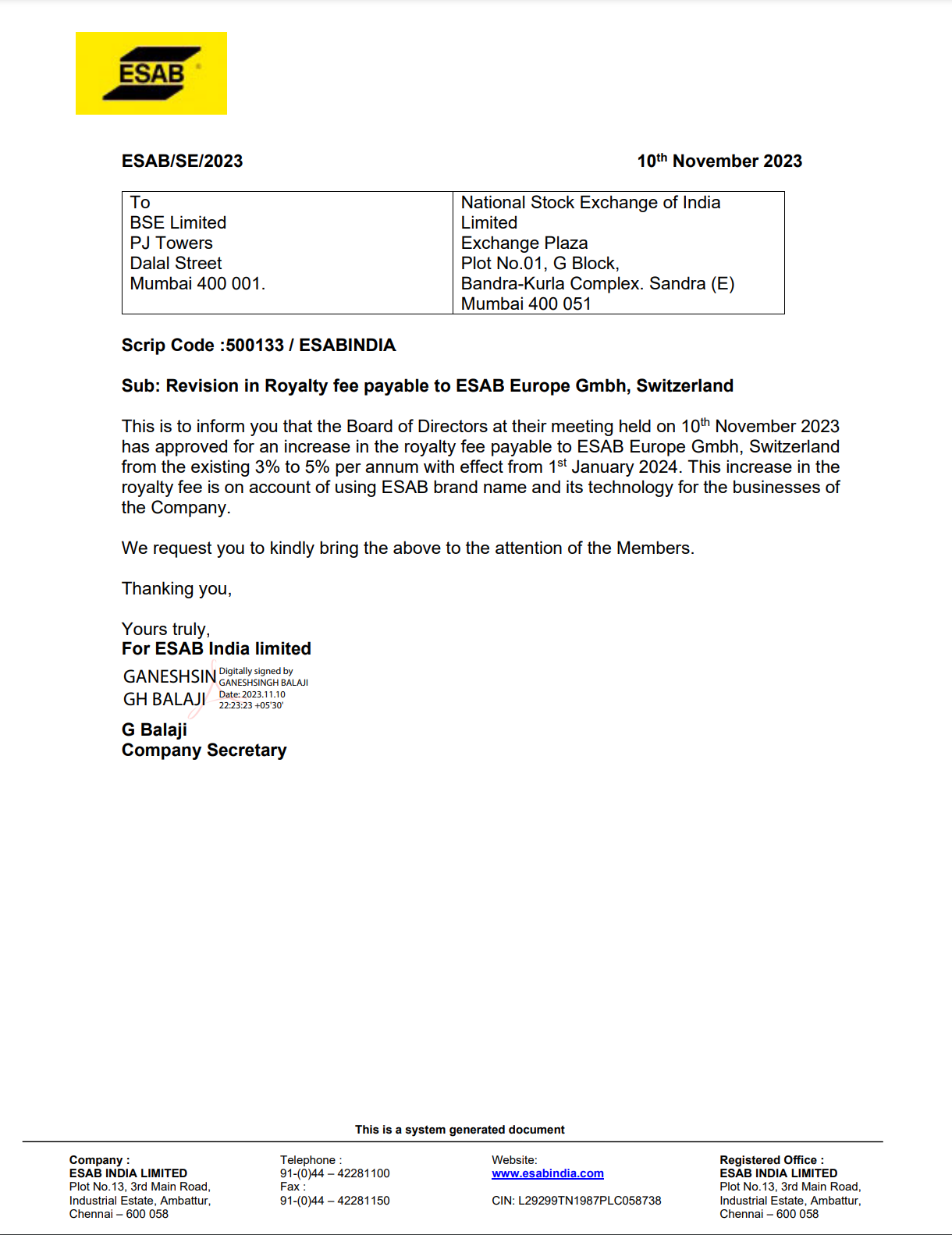

The company’s board of directors met on November 10, 2023, and they have decided to raise the fee they pay to ESAB Europe Gmbh, Switzerland. This fee is for using the ESAB brand name and technology in their business. The current fee is 3%, but starting from January 1, 2024, they will be paying 5% as the new fee. This decision is to ensure they can keep using the ESAB brand and technology.

Very typical MNC behavior…raising royalty as soon company starts doing better… since 73.72% of the listed entity is already owned by ESAB USA (through it subsidiaries), this 2% increase in royalty is basically taking away that much money from minority shareholders…No wonder stock price got punished in the market

disclosure - invested earlier but reducing position and may decide to exit soon

1 Like