Hi Guys

How is the journey, especially after brutal fall in 2025.

Please share your experiences.

Best Regards

Hi Guys

How is the journey, especially after brutal fall in 2025.

Please share your experiences.

Best Regards

We hardly had a fall till now

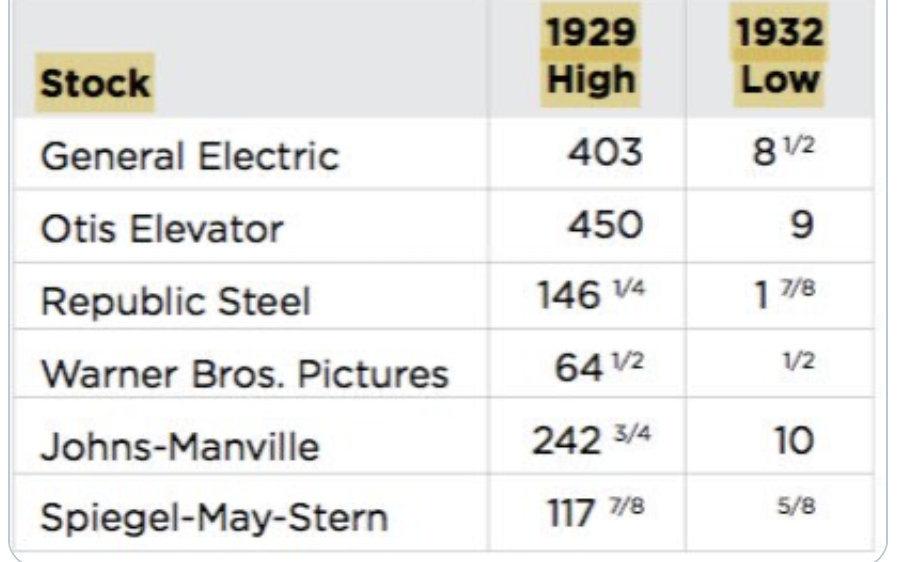

Full time investors have to be prepared for major declines in portfolio values even in quality stocks … One never knows when 67X will become just 2X . A small snapshot of history to pinned & revisited again and again

This is like Infosys falling from Rs 1800 to Rs 50 … It is crazy to think what can happen to small cap and mid cap in such crashes …

How does one survive such fall is important … Remember even Ben Graham filed for bankruptcy in this fall … This did not happen in 1929 but in 1930s when he tried to average down ( using leverage) stocks which he thought were bargains .

Full time investors need to stick to strict asset allocation rules at all time → bull and bear markets .

Leverage should be strict NO NO at all times …

Survival is key to long term success in Stock market .

Sustainable Dividends income is very important … The interesting part is even in 1929 depression … Good sustianable dividend stocks kept giving good dividend yields upto 20% when prices crashed .

I have strict rules on equity and individual firm and sector level exposures . I don’t touch emergency funds even during most attractive investment time like 2013 , 2016 , 2020 …

Hope this is useful

The is no option to superlike a message, hence writing.

This line speaks of maturity level and I echo this. If we stop here, its hardly a fall yet.

Some excellent examples you have cited from 1929 - 1932 with some marquee names in there and must have even been large caps before their fall.

How does one ensure during initial stock selection that their universe of stocks & hence businesses are such that in extreme market crashes they fall a worst case 50% (just an example) and not like 95% and never go towards bankruptcy.

As per you, what is an ideal exposure to equity as a percentage of networth (after removing the house a person stays in from the networth).

Thanks a lot for your comments. Always look forward to your messages.

These must have been cash rich companies from the universe of healthy stocks and investors who would have averaged these down would have survived and came out stronger. Were these FMCG/consumer facing cash rich or any such names? Am I wrong in my interpretation? Did this universe also fell 95% or stopped at say 50%, relatively much less than the ones that were battered badly (numbers just examples)

I have discussed my portfolio construct in this thread …

To rephrase : My Investment philosophy is

which means

For simplicity → Equity asset allocation at broad level you can use following table … . All depends on your own risk profile .

I have similar pre-determined price targets at firm and sector level depending upon their business performance for next 3 years … That helps me to manage volatility better

Hope the above info is useful

Hi All , I know there are a lot of full-time Investors in this forum. And every full-time person knows it’s extremely boring profession during the months when there are no earnings release or earnings concalls.

Full-time is a tricky profession when it comes time management, you may seem like you’re bored but at the same time you cannot get very busy outside the markets , one needs to strike a balance

I have a small study office like 2 mins away from my home on scooter.I am struggling when it comes to having urge to come back to office after lunch on non-earnings months , so I would love to hear from others how do you plan your day to keep yourself " occupied "

I lack curiosity, so I find it difficult to read anything or watch anything that doesn’t give me an actionable outcome with respect to markets in the office, this is my biggest struggle at the moment.

Thanks & Regards,

Varun

Hi,

Frankly I find hard pressed for time even on non result seasons. I try and read 2 financial papers ( 1 International and 1 Indian ) . I also try to read up on 1 company in my watch list most of the day (concall, presentation, AR etc ). I have some side projects like studying technical analysis , some skill sets etc. What I have found helpful is to have a daily to do list and having a time table . I track the hours spend reading / studying daily so as to keep track. I do endeavour to read a book for 1 hr min daily.

I do have the problem of not going back to study post lunch as you mentioned . I take a nap ![]() post lunch for 1-1.30 hrs

post lunch for 1-1.30 hrs ![]()

I guess that is one of the luxuries of being a full time investor.

Thanks Midhun , I think the time table and one hour dedicated to book reading is an excellent idea. I shall try to implement that.

Happy to know about the post lunch nap atleast that makes me less guilty ![]()

If you are already in active Job than don’t leave your Job untill you have Networth of atleast 6-7 cr. Keep your loans to nil. 50% real estate, 50% liquid. For me its 9 months now in full time investing, don’t have time to get bored:joy:![]() . Morning Badminton, 6-7 hrs in active and passive market engagements, 2 hrs Netflix/prime. Already completed 27 years in corporate Job, no more patience left to continue as Job demand expectations increased hughly, opted VRS last year, nil liabilities, son persuing graduation, have created good real estate portfolio and Equity PF hence could take a call to go for VRS, think wisely before taking any plunge from active Job, though no one likes however, everyone has to do it for the sake of our dear ones and nothing wrong in it. Buying your freedom is most toughest part in life.

. Morning Badminton, 6-7 hrs in active and passive market engagements, 2 hrs Netflix/prime. Already completed 27 years in corporate Job, no more patience left to continue as Job demand expectations increased hughly, opted VRS last year, nil liabilities, son persuing graduation, have created good real estate portfolio and Equity PF hence could take a call to go for VRS, think wisely before taking any plunge from active Job, though no one likes however, everyone has to do it for the sake of our dear ones and nothing wrong in it. Buying your freedom is most toughest part in life.

Hi Cshar , thanks for your msg. Can you explain briefly about your daily 6-7 hours market activity , it would help me get a perspective of your daily routine

These are daily on non earning month or earning month.

whereas on Earning months which are very busy going through con calls, reading notes utilising notebook LM google feature to summarise in podcast. Also reading ratings notification as they are much detailed.

These are very much enough to keep. myself super occupied.

Apart from this watching cricket , gym, walking and family time.

And sometime not often a short trip.

Hi,

I have quit my job & have been trying to learn the ropes of investing. Very vaild points made by fellow investors, I like to see it as Pre & Post.

The Pre would be getting your financials in place so that you can sustain your lifestyle, this required a 6-12 months of tracking my expenses & income alongwith calculating my net worth. Putting in place debt instruments in FDs etc to receive monthly income. Once everything was aligned I took the plunge.

In the Post scenario, I would recommend joining any investor community (I have enrolled in SOIC), since I had to learn the basics & also once you finish the learning by being a part of a community you get a lot of information thrown at you, YT videos, book recommendation, online & offline sessions talking about industries etc. This way the struggle is very less on what I need to do everyday as an individual. sort of give some guidelines.

Apart from this regular taking time for yourself & a little bit of travel. Basically find more meaning to your life rather than being a part of the rat race.

P.S: I am not recommending or promoting any particular community for stocks

You need to define your time how and on what you want to dedicate, I am long term, short term both, even if convincing intraday as well. Short and Intraday for cash generation, long for wealth generation.

Charlie Munger said “Those who keep learning will keep rising in life.” So, you gotta be a life long leaner to stay top of your investing game. Lot of investors have said that they get ideas and get better at investing from reading philosophy, history, game theory and even fiction. So read books/ topics that invoke your curiosity. Play games/ activities that challenge your brain and improve your mental cognition like chess and bridge.

Apart from these talk to people from all aspects of your life. Talk to your mechanic and ask why he uses one brand of battery or engine oil over others, talk to your IT friend and ask how it was to work in top 3 IT companies. Talk to people.

Very good post. I would like to add my two cents too. Its been only 6 months since i became a full time investor but routine has been similar to what most people posted here.

I try to start my day at 7.30 am after exercising and yoga. and work until 12.30 pm with short breaks in between.

Post lunch, i have a 2 hour kind of break where i see podcasts or management interviews ..kind of chilling out. then couple of hours of work. Most of the time is spent on screening (which company to read).

I have been spending a lot of time on screener, sovrenn, regulation30 links, just to find which companies to study.

Evenings- generally not much work…more of walks (thinking), gym and television and sleep by 10 pm to wake up around 6 am.

On weekends, the intensity of work drops (just a habit that has been ingrained as i was working for 17 years).

I agree very good post. I am still earning a good amount and unfortunately laid off recently. I am already into the groove of investing for many years now. I have sufficient saving/invested at ~5 cr. Just not able to decide if full time is going to be the right decision at this point of time or Shall I accumulate little more by finding job. But question that I ask is what is enough? I think, I have enough but somewhere job and constant flow of monthly income from salary prohibiting the full time decision. Any advice or suggestion from fellow investors here? How did you break the chain especially after working for more than 15 years 20 years etc?

My response to anyone contemplating this would be - introspect very very deeply. For all said and done, a life without any meaningful engagement is not worth it ( for most atleast ).

One needs to remember that Investing in itself is not a professional endeavor unless you are investing on behalf of others while being compensated for the time that you spend towards it. If its about deploying your own money, there is no compensation for time. And in all honesty, you dont even need that much time ( if your portfolio goes beyond 10-15 stocks, you would be mimicking the market or some active fund ).

While a fund of 5Cr may be technically enough to sustain your lifestyle ( am assuming a moderate lifestyle here ), there would most likely be a feeling of emptiness since an inner voice will keep asking you if you are adding any value to anything or anyone in life.

Dont want to make this too philosophical but just my 2 cents.

I worked for 13 years almost and quitted at 33.

https://forum.valuepickr.com/t/daily-routine-for-full-time-investors/192142/7?u=imurlovish

On top of what i shared above, below are few points:

If your porfolio and your strategies are working very well and you are consistently making money every year, some year 40-60% and in some 10-15% due to market cycles. You are good to go. You know how this market works. So having a right corpus (depending on your family expenses) you can choose to plan 1 year - 2 year of free cash in liquid funds. As sometime market bearish can vary recent one was of ukraine war time of 18 months, however 12 months free cash planning is enough. And rest of the money can be used to make more.

In the end the focus should be if you are going to do very expensive buying , for example a 2cr house, your portfolio should be enough to sustain this. So having 5 cr portfolio, lets enjoy one more bull rally and when 2 cr looks like peanuts , spend it.

Having buckets of portfolio is also one kind of way to live life -

for example:

20 Lakh portfolio - profit from it for enjoying trips, ghumna firna etc.

1 cr - for kids education, marriage.

and so on.

At last on the headline topic:

I also wish people to find right mentor at the right time.

Invest on yourself.

And lastly i have joined PGPFM from NISM , to get my third degree. Was thinking when quitting i can do much more. ![]()

I have a different sort of question for full time investors here. I think it’s most probable that your yearly expenses are/were far lower compared to portfolio. I assume this since anyone leaving salaried job for full time investing will be very cautious and traditional safe withdrawal rates like 4% and 3% apply only for index and mutual funds. Stocks are too volatile and have too much drawdowns to use large withdrawal rates.

Most of us are into full time investing to get much higher returns than index. If we can’t beat index over long timeframe, there would be no point of investing ourselves. So there are many full time folks here who have generated and will generate 18-20-25-30 or even higher CAGR over years.

Just for an example, if one starts with yearly expenses of 12L and Portfolio of 8-10 Cr. After a decade of compounding, if your expenses only keep up with inflation, the expenses vs portfolio difference will be huge.

Now my question for you is have you increased or planned to increase your expenses and lifestyle as your portfolio goes higher? And if not, what’s the point of increasing portfolio value? After a while, it’ll be just a number in demat. And after a certain age, no number will matter if your health is not good. I get that all of us enjoy the journey of investing. But would it harm to enjoy some fruits of our achievements too? Otherwise, there will be only two uses of our wealth. It will pass on to next generation (will anyways happen whether or not we spend) or it should be utilized for charity.

Would like to hear experience and thoughts of full time investors here.

Note - I always had this question in mind all these years. I read in Warren Buffett biography that he always knew he was going to be rich, from the very young age. I am sure most of us who have seen a decade in markets and have generated decent CAGR, know in our heart, that if we continue for few decades, most probably, we are going to end up HNI’s and UHNI’s. The thing I am in process of figuring out is what am I going to do with the money.