ELEVATOR PITCH

Equitas Small Finance Bank is at an inflection point with strong core book growth, reducing cost to income, credit cost moderation, relative undervaluation and a well seasoned team driving the above levers of change at the bank.

BACKGROUND

Equitas Small Finance Bank Ltd before acquiring small bank license, operated as a wholly-owned subsidiary of Equitas Holding Ltd. The holding entity started its operations in 2007 in the microfinance segment & diversified into vehicle & housing finance in 2011. Also entered into SME & LAP in 2013. It merged with the other two subsidiaries named Equitas Microfinance Ltd & Equitas Housing Finance Ltd & formed a bank. After receiving a license in Sept 2016 the company commenced operations under Equitas Small Finance Bank.

CURRENT MARKET/INDUSTRY TRENDS

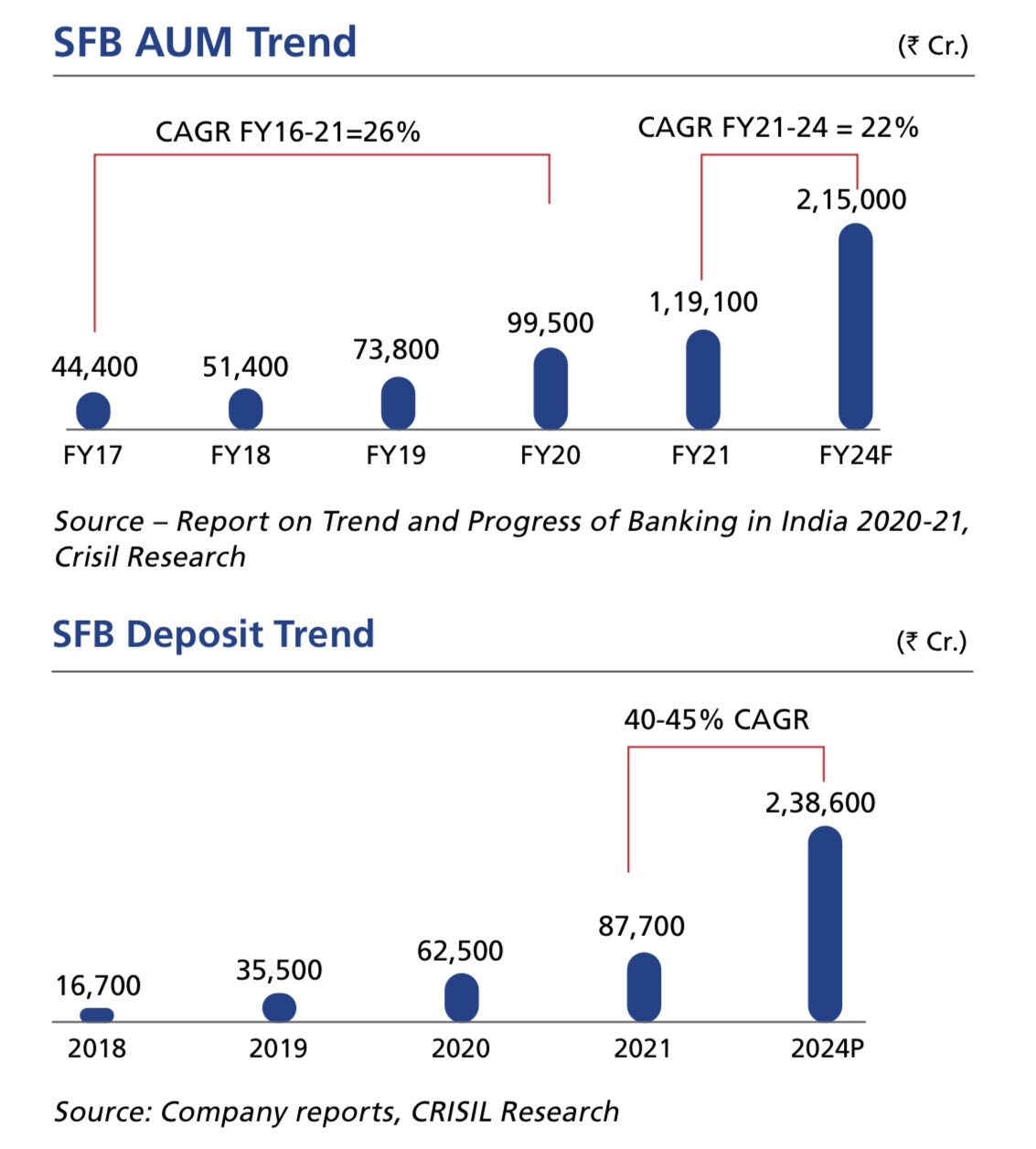

There are 12 operational SFBs in the country. With experience in serving the underserved segments, SFBs have a strong operational experience in MSME Finance, vehicle finance, MFI, affordable housing loans. They are well positioned to address the credit gap in small ticket loans across customer segments. For context on the degree of runway and underpentration, the entire universe of SFBs form only 1% of the total assets of the scheduled commercial banks.

SFB total advances grew at a CAGR of 26% during FY16-21. The top three (Equitas, AU, Ujjivan) accounted for 60% of the aggregate AUM. The sector’s loan portfolio is likely to see healthy growth going forward as most of the SFBs have completed the transition phase to banks and will experience operating leverage going forward.

When the licenses were issued by RBI in 2015, 8 out of 10 entities were microfinance entities, it’s interesting to see the trajectory some of the major ones have taken in terms of building the assets and liability franchises.

COMPARISON WITH OTHER SFBs ON KEY METRICS

| Metric as of Q1FY23 | Equitas | AU SFB | Ujjivan |

|---|---|---|---|

| Market Cap | 6,018 Cr | 40,033 Cr | 4,691 Cr |

| Price to Book | 1.4 | 5.1 | 1.6 |

| Loan Book | 21.6k Cr | 50.1k Cr | 19.4k Cr |

| NIM | 9.05% | 5.9% | 9.6% |

| Avg Yield on Advances | 17.15% | 13.3% | 18% |

| CASA% | 52% | 39% | 28% |

| Cost of Funds | 6.2% | 5.7% | 5.9% |

| GNPA | 3.95% | 1.96% | 5.9% |

| NNPA | 2.07% | 0.56% | 0.1% |

| Assets Mix | SBL - 38%, VF - 24%, MFI - 18%, HF - 8%, Others - 8% | VF - 37%, SBL - 34%, CB - 17%, HF - 6%, Others - 6% | MFI - 69%, MSE - 9%, HF - 15%, Others - 7% |

| Secured Book | 82% | 94% | 29% |

| Restructured Book | 5.5% | 2.1% | 3.4% |

| Cost to Income | 60.6% | 65% | 61% |

| RoA | 1.4% | 1.5% | 3.4% |

| RoE | 9.03% | 14% | 28% |

| PCR | 48.46% | 72% | 98% |

LIABILITY PRODUCTS

For any good bank, a well functioning and solid liability franchise helps build the foundation for the lending operations. Efforts have gone into building a CASA franchise by offering higher savings rate and focusing on partnerships with fintechs and NRI accounts to source savings accounts. With term deposits, the bank has focussed on granular retail deposits which contribute 72% of total term deposits. A glimpse of the trajectory here over the past few years is interesting.

| FY 18 | Current | |

|---|---|---|

| Deposits | 5.6k Cr | 20.4k Cr |

| CASA | 1.6k Cr | 10.6k Cr |

| CASA Ratio | 28% | 52% |

| Cost of Funds | 8.4% | 6.2% |

Borrowings Profile

The bank has a granular liability profile - The share of deposits, including certificates of deposits, in the non-equity liabilities rose to 88% in FY22 (FY21:79.7%), led by 76% yoy growth in current accounts saving accounts deposits (FY22: 52% of total deposits; FY21: 34.4%; FY20: 21.4%), primarily driven by high growth in savings account balance (78% yoy in FY22). The term deposits declined by 16% yoy in FY22; out of the outstanding deposits, around 22% are bulk deposits.

A lot of the trajectory in CASA is attributable to the high CASA interest rates offered compared to other institutions (7% p.a for balances above 5 lakhs with no MAB requirements). Remains to be seen how sticky this CASA base is, if the bank chooses to reduce rates here.

While this is not a major concern, considering their lending segment and spreads are quite healthy to absorb continued higher interest rates. And with the exception of Chola, they will continue to have the edge in CoF over competition in the regions they operate in.

The bank is further working on building the stickiness in savings accounts by adding other products like 3 in 1 brokerage, insurance, fastag and credit cards.

Some of the fintech partnerships that the bank is driving within the ecosystem. Digitally sourced accounts now form 9% of overall SA balance.

ASSET PRODUCTS:

The bank has presence mainly in 6 asset segments: Small Business Loans (38%), Vehicle Finance (24%), Micro Finance (18%), Housing Finance (8%), MSE Finance (5%), NBFC (3%). Brief description of each asset product and customer profiles looked at here:

Small Business Loans

Small Business Loans are secured products through LAP offered to mostly self employed individuals in urban and semi-urban locations. Small business loans are advanced to individuals belonging to low income groups engaged in business activities that do not maintain formal records for credit evaluation. Customers that typically comprise this product segment include mechanics with garages, push-cart owners, and individuals carrying out agriculture, dairy business, etc. The ATS for these loans is in the range of 6.23 Lakhs.

SBL was started as a cross sell product to MFI customers who had been through 2 or more cycles with good payment record. Currently, >70% of SBL loans are to customers outside MFI segment. The high yields in a secured product are largely due to assessment risks, high opex and low ticket size. Further, the bank does not use DSAs and the sourcing is predominantly done by the bank’s employees.

Housing Finance

HF is targeted towards self-employed individuals who have limited access to loans from banks and larger housing finance companies. Loans are provided for purchase of plots or house, construction of house, improvement/ restoration/ extension of home. Some of the affordable housing finance products are cross-sell products offered to existing customers with a satisfactory track record. Customers in this segment typically run small enterprises and/or are employed in the informal segment, or are involved in informal trade or commercial activity where income is not completely documented and requires field based credit assessment.

Microfinance

Microfinance loans are targeted towards micro-entrepreneurial women with limited access to formal financing sources. These loans are provided essentially for use in their small businesses or other income generating activities. These loans have a tenure of up to two years and are offered at interest rates of 20-21% per annum. The group loan products are built on the peer-guarantee loan model, which enables individuals to take loans without having to provide collateral or security on an individual basis, while promoting credit discipline through mutual support within the group, prudent financial conduct among the group, and prompt repayment of their loans. Typically repayments are made at group meetings, which are held at intervals of 28 days. At these meetings, if any member defaults in making payments to the group leader or is absent, the other group members are responsible for the amount. The member is subsequently required to repay the amount to the group.

Particularly interesting is that they have walked the talk on reducing the risk in this segment. Can see that in how the book is performing and in how the ticket sizes are among the lowest among MFI peers.

Vehicle Finance

Commercial vehicle finance segment is typically first-time formal financial channel borrowers purchasing used and new commercial vehicles, with experience in hyperlocal logistics. It also includes small fleet operators. It is conducted based on experience of working with customers without sufficient credit history, and ability to effectively assess risks associated with financing such customers with no access to formal credit. While such customers typically have limited access to bank loans for commercial vehicle financing and mostly have limited or no credit history, they should otherwise own assets such as a house or property or vehicle.

In the used passenger vehicle segment, it is the private cars segment and are working with dealers operating across all the vehicle finance branches. Private car customers are majorly income based or surrogate based. This segment of clients are all credit tested.

MSE Finance

MSE finance is provided to enterprises engaged in business activities that maintain formal records for credit evaluation, primarily in urban and semi-urban areas. They typically undertake manufacturing and trading activities. Products are working capital loans in the form of (a) fund based facilities including cash credit limits, overdraft limits; and (b) non-fund based facilities like bank guarantees and letters of credit, term loans for specific business purposes.

These facilities are predominantly secured by primary and collateral security in the form of stock, book debts, machinery, commercial or industrial premises and residential properties of promoters/ proprietors.

Evolution of the AUM mix over time

| Loan Type (cr) | FY19 | FY20 | Q1FY21 | Q1FY22 | Q1 FY23 | Contri %ge | Yield |

|---|---|---|---|---|---|---|---|

| MFI | 3069 | 3616 | 3618 | 3128 | 4007 | 18% | 20.8% |

| SBL | 4577 | 6279 | 5855 | 6998 | 8234 | 38% | 17% |

| VF | 2951 | 3760 | 3776 | 4377 | 5279 | 24% | 17% |

| HF | incl in SBL | incl in SBL | 629 | 1017 | 1821 | 8% | 12% |

| MSE | 180 | 669 | 712 | 1208 | 1122 | 5% | 9.9% |

| NBFC | 455 | 818 | 772 | 914 | 692 | 3% | 9.7% |

| Others | 469 | 223 | 211 | 195 | 533 | 2% | |

| Total | 11704 | 15367 | 15573 | 17837 | 21688 |

The company has grown the MFI book disproportionately less and focussed on growing its secured book with SBL, VF and HF. MFI book is expected to be around 10-15% of AUM going forward.

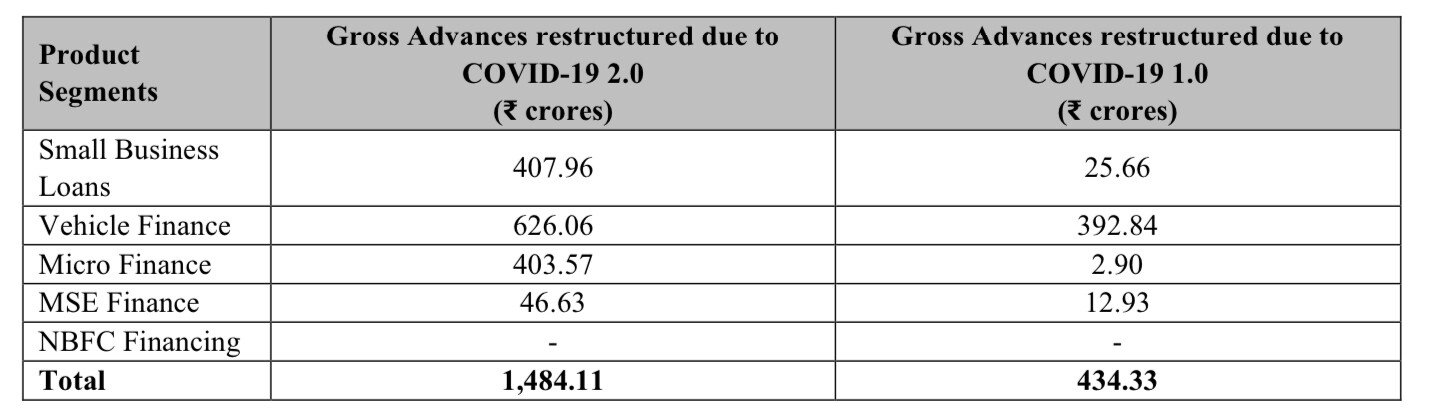

Restructured Book

With COVID first wave and second wave, the bank had restructured its book.

In the COVID second wave, where the bank had to restructure 9% of its loan book. As of Q1FY23, the restructured book is down to 5% of total loan book and the non-standard part of the restructured book is down to 3.6%.

Slippages, GNPA and Provisions

| Quarter | Q2FY20 | Q3FY20 | Q4FY20 | Q1FY21 | Q2FY21 | Q3FY21 | Q4FY21 | Q1FY22 | Q2FY22 | Q3FY22 | Q4FY22 | Q1FY23 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Loans | 13268 | 14615 | 15367 | 15573 | 16731 | 17373 | 17925 | 17837 | 18978 | 19687 | 20597 | 21688 |

| Gross Slippages | 108 | 127 | 94 | 15 | 23 | 36 | 514 | 375 | 339 | 267 | 408 | 296 |

| GS % (non annualized) | 0.8% | 0.9% | 0.6% | 0.1% | 0.1% | 0.2% | 2.9% | 2.1% | 1.8% | 1.4% | 2.0% | 1.4% |

| Net Slippages | 61 | 63 | 21 | 7 | -4 | 6 | 459 | 186 | 87 | 118 | 164 | 148 |

| NS % (non annualized) | 0.5% | 0.4% | 0.1% | 0.0% | 0.0% | 0.0% | 2.6% | 1.0% | 0.5% | 0.6% | 0.8% | 0.7% |

We can begin to see convergence between the net slippages of pre covid quarters and recent quarters as collections and recoveries improve. With regards to gross slippages, Q1FY23, the bank saw 296 cr of slippages, of which 53% was from the restructured book, indicating that the slippages on the 95% of the book that is non-restructured has gone back to pre-covid levels. Credit cost should normalise going forward as the restructured book gets reduced and provided for and the stress in the book gets reduced with each quarter.

| Segment | GNPA %ge | PCR %ge |

|---|---|---|

| MFI | 4.7% | 47.8% |

| SBL | 4.2% | 39.6% |

| HF | 1.3% | 34.9% |

| VF | 4.2% | 67.9% |

| MSE | 5.6% | 30.9% |

| NBFC | 0.7% | 100% |

| Total | 3.9% | 48.5% |

The management has guided to bringing the GNPA levels down to pre covid levels of 2.5% in the next few quarters, for credit cost of 1.5% for FY23 and to taking the PCR levels to 70% over the medium term.

INTERESTING VIEWPOINTS:

Organisation Structure

The org structure at Equitas is such that the branch manager is responsible for both lending and collection. There are separate collections teams but they report to the branch manager. Ensures that even at onboarding, it is the right set of customers that are being onboarded and not for the purposes of chasing growth and hitting targets.

Underwriting Culture

In the period of existence as NBFC and bank, it has exhibited a conservative underwriting culture (evidenced by among the lowest ticket sizes for MFI loans and diversification away from MFI earlier than other SFBs) for the type of customer segment, if credit costs are taken as proxy. The bank focuses on constant monitoring due to the erratic nature of customer cashflows.

| Year | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

|---|---|---|---|---|---|---|---|---|

| Credit Cost | 1.8% | 1.4% | 1.4% | 2.6% | 1.0% | 1.7% | 2.3% | 2.6% |

| Spike | Gaja | Covid | Covid |

Universal Banking License

Post the completion of amalgamation of Equitas Holdings, the bank is due to apply for the universal banking license with the RBI. This, along with the lowering cost of funds, will enable the bank to increase the lending to the non PSL and formal segment which is currently at only ~10%. On a risk adjusted basis, this would enable the bank to enter into product segments and geographies that are at similar levels of attractiveness in terms of returns.

BULLISH VIEWPOINTS

Vintage of the Asset Products

The company has reasonable vintage in all of the major segments of SBL, VF, MFI, HF and has been operating in these segments even before it became a bank. MFI is the oldest segment launched in 2007, Vehicle Finance and Housing Finance was launched in 2011 and Small Business Loans was launched in 2013. MSE Financing was launched in 2018. The book is of reasonable vintage and seasoned, having been through multiple shocks including the microfinance crisis, demonetisation, Covid, etc. And the different segment’s lending operations are experienced, having built in specialisation and expertise in underwriting to this segment as well having done the migration and diversification away from a concentrated MFI book years ago that other SFBs are going through now.

Excerpt from QIP doc:

The data we have collected over the years and continue to collect relating to cash flows, credit and demographic behaviors of our customer segments can be applied to derive a granular understanding of the banking trends of such customer segments. As a large portion of our customers are first-time borrowers, relying solely on credit bureaus for credit decisions is inadequate, and we are mandated by our internal policies to additionally apply our extensive knowledge of the segment.

This vintage helps build an organisation colossus on understanding how different segments and geographies behave under stress. It feeds back into the loop to correct the underwriting filters.

Opex Evolution

In the set up stage of the bank, it incurred heavy opex towards setting up of new branches, tech infra, addition of employees which increased opex and decreased ROA.

| Year | 2018 | 2019 | 2020 | Q1FY22 | Q1FY23 |

|---|---|---|---|---|---|

| Cost to Income | 79.9% | 70.3% | 66.4% | 68% | 60.6% |

Last quarter had some one-offs, adjusted for which C/I ratio would have been 65%, management is targeting to bring this down to 55% over the next couple of years, which would lift the RoA considerably to >2%.

If the bank brings down the cost to income to ~55% in FY25 from the ~65% base of FY22, assuming a 20% CAGR of NII+Other income, the delta from operating leverage here could add up to ~450 cr to the bank’s operating profits.

Secured Book

The bank has moved to a nearly 82% secured book with only the MFI portion of the book remaining unsecured. SBL loans are backed by property as collateral. MSE loans are backed by stock, fixed assets as collateral. Vehicle finance loans are backed by underlying vehicles as collateral. LGD values in all the segments are low, even in vehicle finance where the bank has taken 100% provisions in the restructured book that went to NPA, the LGD values are 40-45%.

Further, with low LGDs in VF portfolio and LAP based SBLs, HF portfolio, the bank can apply better leverage to reach better RoEs vs high RoA MFI focussed players where the book can’t be leveraged significantly.

Cost of Funds/Liabilities

With the strong growth in retail liabilities and declining cost of funds ~6%, now mostly at par with private banks like RBL, etc. the bank has indicated in recent interactions about going down the risk curve, lending to more formal segment customers and prime product segments with better risk adjusted returns.

BEARISH VIEWPOINTS

Customer Profile Served

The customer profiles served are the highest affected during times of macro events and disturbances. Over the last decade, this segment has witnessed multiple events that have caused NPAs to spike including floods, demonetisation, COVID, etc.

At an industry level, all institutions lending to these segments have periods of high NPAs and depressed returns during these event led spikes in bad loans.

Overhang in Leadership Transition

After a stint of nearly 15 years, Vasudevan is moving out of the role to focus on his charity work. While there are no specified timelines to close the succession, it will remain an overhang on the stock until the person is identified and leadership transition is completed. In the interim, they’ve elevated the current head of assets and head of liabilities divisions to ED roles with more added responsibilities.

PCR low

The PCR is on the lower side at close to 48% compared to other banks. Management has stated the intent to take it to 65-70% incrementally over the upcoming quarters depending on slippages and recoveries.

Geographic Concentration

The company has a large part of its loan book concentrated in Tamil Nadu (~54%). And the top 3 states account for 78% of the total loan book. Maharashtra at 13% and Karnataka at 11%. The bank has now been trying to diversify its loan book and now has operations across 18 states and UTs. However, in the medium term the loan book is likely to be concentrated in a few states.

Pan India Bank

One question that remains and yet to be known unless interacting with people in the company, is the culture they are building. With a large portion of book in TN and top management from TN - it is yet to be fully understood if they can become a truly pan India bank. As is the case with Equitas, the liability side network expansion doesn’t completely correlate to asset book expansion as they service different customer segments. The liability branches are well spread out. Remains to be monitored whether they have the ambition and depth to take it to scale in the asset side across the country in a calibrated manner.

MANAGEMENT

The top management has a history of experience and expertise in banking and NBFC companies and have led critical functions there.

PN Vasudevan - MD & CEO - 15 years at Equitas. Previously, 2 decades at Cholamandalam Group. Was Vice President and Head - Vehicle Finance at Chola.

Rohit Phadke - Senior President, Assets - 2 years at Equitas. Previously, 2 decades at Cholamandalam Group. Was President and Business Head - Home Loans.

Murali Vaidyanathan - Senior President, Liabilities - 3 years at Equitas. Previously, 13 years at Kotak Mahindra Bank. Was EVP at Kotak.

Pallab Mukherji - Chief People Officer - previously with HDFC Bank.

Narayanan Easwaran - CTO - previously with IDFC First.

Vaibhav Joshi - Chief Digital Officer - previously Group EVP and Digital Head at Yes Bank.

With the management there has been a history of walking the talk and conservativeness in their lending. The team has a mix of folks with expertise in scaling and building the bank.

VALUATION MODEL/ESTIMATES

| FY22 | FY23 | FY24 | FY25 | |

|---|---|---|---|---|

| NII | 2039 | 2447 | 2936 | 3523 |

| Other Income | 538 | 646 | 775 | 930 |

| Total Income | 2577 | 3092 | 3711 | 4453 |

| Cost/Income | 66% | 61% | 59% | 57% |

| Opex | 1704 | 1900 | 2175 | 2525 |

| PPOP | 873 | 1192 | 1536 | 1928 |

| Credit Cost | 494 | 425 | 525 | 620 |

| Credit Cost % | 2.6% | 1.9% | 1.9% | 1.9% |

| PAT | 281 | 576 | 758 | 981 |

| RoA | 1.1% | 2.5% | 2.8% | 3.0% |

| RoE | 7.75% | 17.8% | 19.5% | 21.0% |

The bank trades at 1.4 times price to book with scope for re-rating on the basis of growth in advances, operating leverage playing out and credit costs coming into control post moderation in asset quality.

Some rough estimates with the base case of 20% growth CAGR and opex and credit cost taken conservatively gives a picture of what the ROA tree for the bank can look like going forward and gives an idea of the upside.

CORPORATE GOVERNANCE/RED FLAGS/FORENSIC SCAN

-

The bank hasn’t been conservative enough to increase their provision buffers and beef it up at more comfortable PCRs.

-

The key man exit does leave the bank open to the possibility of uncertainty over successor, potential exit of key folks, etc.

-

The bank has historically been active in CSR initiatives and spent considerably higher than mandated norms. The CSR culture shows up repeatedly over multiple ARs historically.

DISCLOSURE(s) OF STOCK STORY CONTRIBUTORS

Ashwin: Invested (transactions in last 30 days)