Any reason of such underperformance? Even company is walking the talk and giving expected results, still market is not rewarding the share holders? any specific reason which is making this pattern to continue?

1 Like

They are raising money through qip … As per my knowledge…once they become market leader.. rewarding does…

About the Company

Entero Healthcare Solutions Ltd is a tech-enabled, pan-India healthcare distribution platform founded in 2018. It connects over 2,700 manufacturers to ~95,000 retail pharmacies and ~3,600 hospitals across 500 districts, distributing a wide range of pharmaceuticals, diagnostics, medical devices, and OTC products. With ~101 warehouses across 20 states, Entero uses its proprietary digital tools (like Entero Direct and MedCords) for real-time inventory, ordering, and supply chain management. The company grows through strategic acquisitions and technology integration, aiming to streamline India’s fragmented healthcare distribution system.

Positives

Top-3 distributor with 113 warehouses, presence across 490 districts / 20 states; strong distribution moat.

Hospital franchise expanding: 2,800+ hospital clients supports higher-quality, stickier demand.

Sustained growth track record: ~30% revenue CAGR (5Y consol) indicates consistent execution and consolidation-led growth.

Strong Q2 operating leverage: Revenue +21% YoY, EBITDA +46% YoY, margin improved to ~4.0%.

H1 momentum strong: Revenue +24% YoY, EBITDA up sharply; profitability scaling faster than topline.

Outgrowing the market: H1 IPM +8.2% vs Entero +24.1%; organic growth still healthy (~13–14%).

Margin trajectory improving: Guided ~4% EBITDA in FY26, with scope to move towards ~5% next FY post integration.

Med-tech pivot is margin accretive: Bioaide + Anand Chemiceutics add higher-margin mix; Anand in low double-digit EBITDA supports blended uplift.

Visible acquisition pipeline impact: FY26 acquisitions can add ~₹1,000 Cr topline once integrated.

Tech investments now monetising: 2–3 years of platform capex can drive efficiency, working capital discipline, customer stickiness.

Management expects H2 growth > H1 aided by recent acquisitions + improving IPM growth (Oct ~11%).

Key Concerns

- Integration Risk: Managing 50+ acquisitions strains systems, culture, and leadership bandwidth.

- High Working Capital Needs: Large inventory and receivables require constant funding support.

- Low Margins: Thin EBIT margins with modest gross margins in a competitive sector.

- Intense Competition: Faces pressure from regional distributors and direct supply by manufacturers.

- Operational Complexity: Consolidating diverse small players adds risk of performance dips and IT overload.

- Capital Inefficiency Drag: Despite a stronger asset turnover (1.88×), Entero’s low Capital Efficiency Ratio suggests excess capital tied up in the business, pulling down ROCE to 9.7% signal of suboptimal capital deployment.

- CFO is negative by 57 Cr as per H1FY26

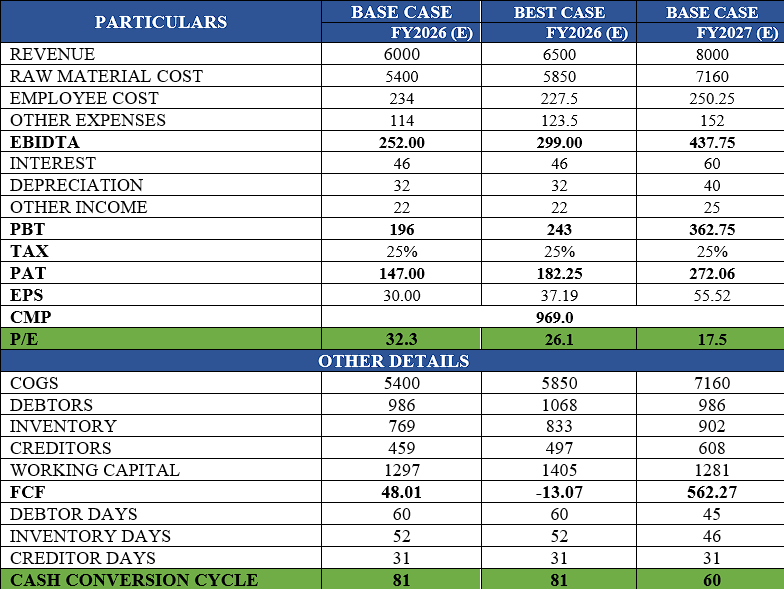

*FUTURE OUTLOOK

CONCLUSION

Entero Healthcare Solutions is a high-growth, tech-enabled consolidator with a steadily improving margin and earnings trajectory. While the business exhibits strong long-term potential, it is currently navigating near-term challenges including operational complexity, integration risk, and negative operating cash flow. For investors with a tolerance for execution risk, Entero offers an attractive mid-cap opportunity, particularly as valuations moderate to ~17.5× FY27E P/E. The current valuation embeds expectations of sustained high growth and operational improvement; if the company successfully executes value-accretive acquisitions, expands margins, and converts scale into strong free cash flow and ROCE

PS. Not invested in the stock