In most conversations around India’s healthcare sector, attention often centers on hospitals, diagnostics, insurance, or the pharmaceutical manufacturing segment. However, the distribution layer — the infrastructure connecting manufacturers to the retail and institutional markets — remains relatively under-discussed.

India’s pharmaceutical distribution network comprises a vast base of small, regional, and often family-run entities. More than 60,000 wholesalers operate across the country, supplying medicines and healthcare products to over 800,000 retail pharmacies and 70,000 hospitals and clinics. This highly fragmented and largely manual system presents both challenges and opportunities for modernization.

Entero Healthcare Solutions Ltd is aiming to address these structural gaps by building a pan-India, technology-enabled pharmaceutical and healthcare distribution platform. It operates in a space currently served by legacy regional distributors and a few scaled players like Keimed (Apollo Group) and Ascent (backed by Reliance). Entero, as the first independent listed platform in this space, aims to drive industry consolidation and operational efficiency.

The Problem: India’s Pharmaceutical Distribution Landscape

India’s pharmaceutical distribution market is structurally different from those in developed markets. While countries like the US or Germany have 2–3 players handling the bulk of national distribution, the Indian market remains highly fragmented. As of FY23, the top three players controlled only around 8–10% of market share.

Here’s a typical breakdown of the current distribution value chain in India:

-

Pharmaceutical Manufacturers: This group includes large firms like Sun Pharma, Cipla, and Alkem, as well as smaller and mid-tier manufacturers. They generally do not distribute directly and rely on intermediaries.

-

Clearing & Forwarding Agents (CFAs) / Super Stockists: These logistics providers manage regional warehousing but do not take inventory risk. They coordinate between manufacturers and distributors.

-

Distributors / Wholesalers: Numbering over 60,000, these are typically region-specific and independently operated. They take inventory ownership, offer 30–90 days credit to customers, and function with limited digitization.

-

Retail Pharmacies & Hospitals: These end-customers often order from multiple distributors to maintain inventory breadth. Most operate without real-time stock visibility or digital ordering systems.

-

Returns & Expiry Management: Handling expired or unsold stock involves significant manual reconciliation and often long claim cycles.

This structure results in several challenges:

- Limited operational efficiency

- Fragmented logistics and fulfillment

- Credit-intensive working capital cycles

- Lack of centralized visibility for manufacturers

As regulatory changes (e.g., GST) and evolving customer expectations encourage compliance and scale, there is increasing demand for more standardized, tech-driven distribution platforms.

Company Background: Founding, Model, and Strategy

Entero was founded in 2018 by Prabhat Agrawal (ex-CEO, Alkem Labs) and Prem Sethi (with experience at IQVIA and Accenture), with support from private equity firm OrbiMed. The founders brought experience from both the pharmaceutical and consulting sectors, while OrbiMed contributed domain-focused capital and strategic backing.

Entero’s approach involved:

- Acquiring regional distributors with strong local relationships

- Integrating them under a common ERP and tech stack

- Offering centralized services to manufacturers and pharmacies

- Building analytics tools for data-driven decision-making

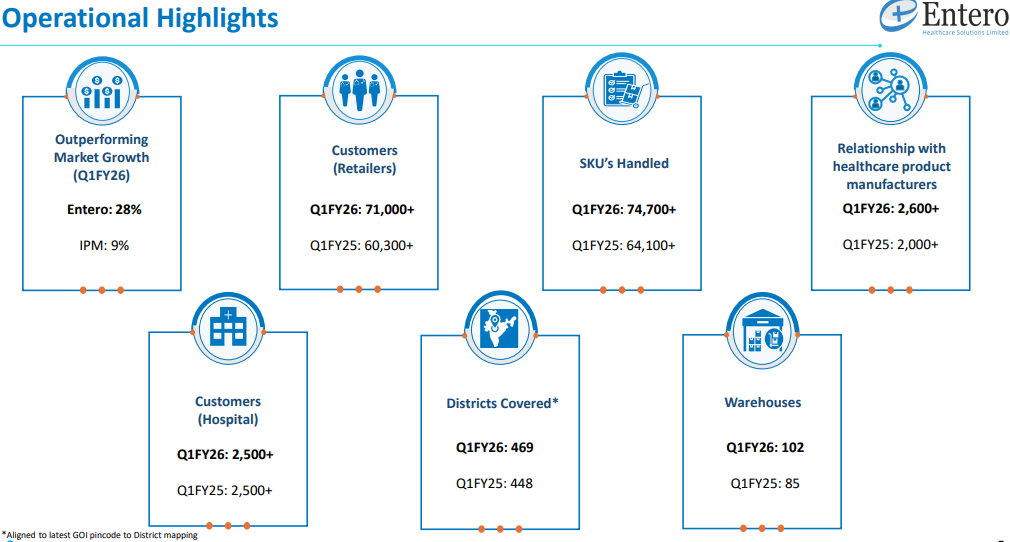

Since inception, the company has:

- Completed 45+ acquisitions

- Integrated 104+ warehouses

- Reached 86,000+ pharmacies and 3,500+ hospitals

- Achieved revenue of ~₹4,000 crore (FY24)

Business Model and Value Proposition

Entero operates as a B2B distributor that procures from over 25,500 manufacturers and supplies to healthcare institutions and retail pharmacies. It earns gross margins of approximately 9–10%, primarily through trade discounts. While it does carry some inventory and credit risk, it positions itself as a supply chain platform rather than a traditional stockist.

In addition to physical distribution, Entero has invested in:

- Entero Direct: A mobile app for pharmacy customers to place orders and manage returns

- Teqtic: A business intelligence platform for manufacturers to track demand and inventory in near real-time

These tools aim to differentiate Entero by providing service reliability, transparency, and operational insight to both ends of the value chain.

Market Opportunity

India’s healthcare product distribution market was valued at approximately ₹2.7–3.3 lakh crore in FY23 and is projected to grow at a CAGR of ~10%, reaching ₹4.5–5 lakh crore by FY28. The sector remains largely unorganized, offering opportunities for consolidation and technology adoption.

Entero’s current market share is under 1.5%, suggesting significant headroom for growth even with modest market share gains.

Execution Highlights

- Rapid Scaling: Revenue growth from zero to ₹4,000+ crore in 6 years through organic growth and acquisitions

- M&A Strategy: Acquisitions focused on geographic expansion and synergy capture, often at 5–7x EBITDA

- Tech-First Infrastructure: Built digital tools for both ordering and analytics

- Improving Margins: Gross margin improved from 8.1% (FY23) to 9.8% (Q3 FY25); EBITDA margin increased from 1.9% to 3.7%, with guidance toward 5%

- Customer Reach: Serving nearly 10% of pharmacies in India, with further potential for network effects

Future Growth Drivers

- Continued acquisitions in under-penetrated regions

- Margin expansion through private label healthcare devices (20–25% gross margin potential)

- Improved customer stickiness via digital platforms and integrations

- Reduction in working capital days (current ~69; target ~60)

- Operating leverage as scale increases

Potential Risks and Considerations

- Cash Flow Management: Sustained negative operating cash flow could affect capital requirements

- Integration Risk: M&A-led growth may face execution or cultural challenges

- Competitive Intensity: Larger players (Keimed, Ascent) may respond with aggressive pricing or strategic alliances

- Thin Margin Profile: Despite scale, mature margins may remain modest relative to capital employed

- Valuation Sensitivity: At 25–30x FY26 earnings, any underperformance on growth or margin could impact valuations

Entero Healthcare is attempting to modernize a complex, legacy-driven sector through scale, technology, and disciplined execution. While the business carries execution and cash flow risks typical of a consolidator, it also offers long-term potential due to the size and fragmentation of the addressable market.

Given its early traction and network effects, Entero is positioned to benefit from formalization trends in the healthcare supply chain.

Investors may wish to track progress on cash generation, acquisition integration, and margin expansion as key metrics of success.

PS: Biased and Invested. Please do your own due diligence.