Any idea what would be competitive moat for endurance and how sustainable it is?

In my opinion it’s relation with Bajaj Auto can be considered as a MOAT which few other companies can boast of.

It has also started supplying other competitors while maintaining the relationship with Bajaj.

While it majorly focuses on 2W vehicles they have increased the share of 4W supplies over the years.

We may also over time get to know if the Maxwell acquisition (engaged in EV battery management systems) is value accretive.

Disc - Holding

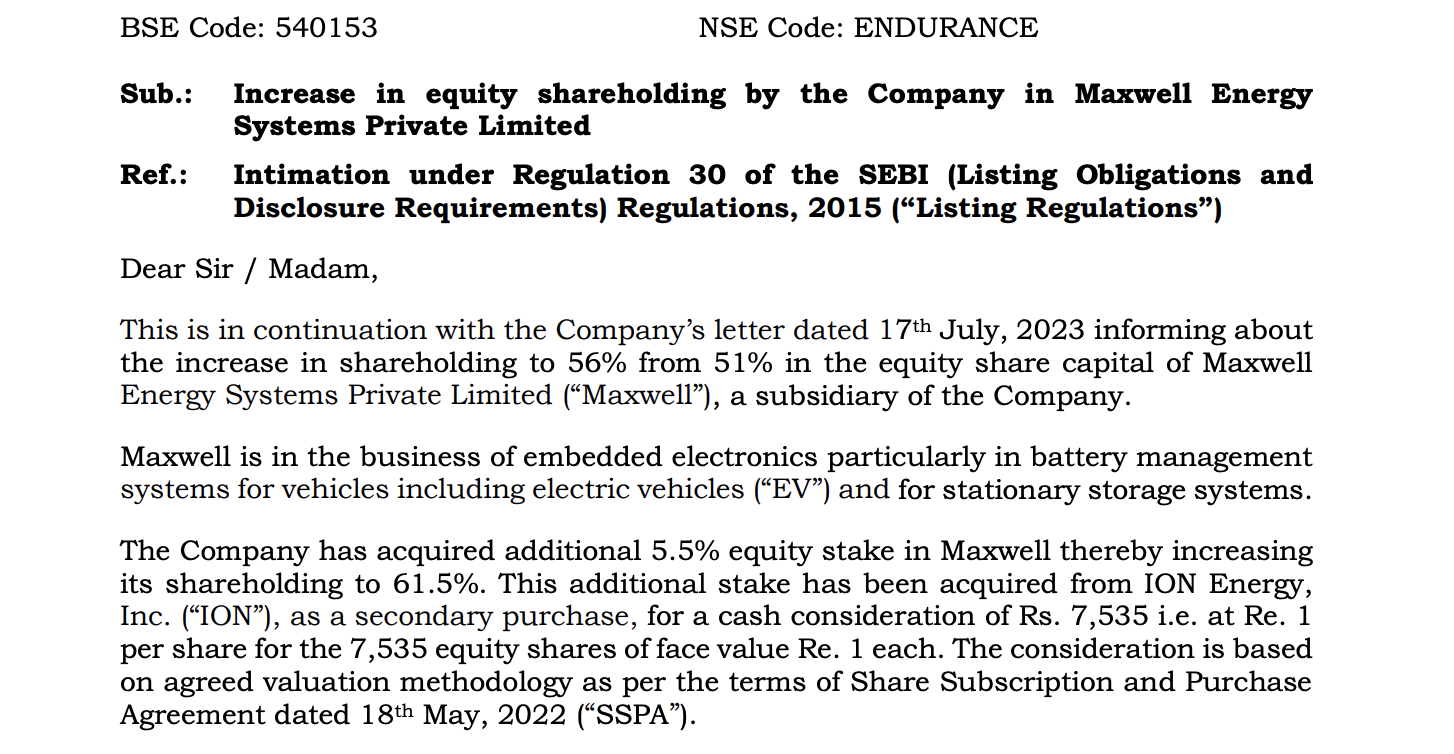

Endurance Maxwell increased stake 61.5% now

Remaining 38.5% equity stake in Maxwell shall be purchased from ION in a phased manner in annual tranches, spread over the next three financial years.

Plan of merger of wholly-owned step down subsidiaries of the Company in Italy.

Company should benefit greatly from new rule mandating ABS for ALL two wheelers

From January 1, 2026, the Indian government will make ABS (Anti-lock Braking System) mandatory for all new two - wheelers, including those below 125ccc , to improve road safety ..!!! - No BUY or SELL Recommendation!!!

Endurance Technologies -

Q2 FY 26 results and concall highlights -

Q2 outcomes -

Revenues - 3604 vs 2939 cr, up 22 pc

EBITDA - 498 vs 409 cr, up 22 pc

PAT - 227 vs 203 cr, up 12 pc

Segmental results -

India business - 2692 vs 2317 cr, up 16 pc. EBITDA @ 336 vs 316 cr, up 6 pc. PAT @ 188 vs 185 cr, up 2 pc

Europe - 908 vs 617 cr, up 47 pc, EBITDA @ 161 vs 100 pc, up 61 pc. PAT @ 41 vs 27 cr, up 42 pc

Maxwell - 44 vs 19 cr, up 130 pc, EBITDA @ 1.9 vs (-) 1.7 pc. PAT @ (-) 1 vs (-) 4 cr

In H1, Indian Scooters, Motorcycles, 3Ws, 4Ws Industry grew by 6 pc, 4 pc, 16 pc and 2 pc respectively. As the new GST rates cuts take effect - These growth rates should see a meaningful uptick in Q3 ( already seeing strong growth in Oct - Nov 25 )

New car registrations in EU grew by 2.5 pc in H1 ( still down 13 pc vs the base of FY 19 )

H1 outcomes -

Revenues - 6958 vs 5799 cr, up 20 pc

EBITDA - 977 vs 616 cr, up 20 pc

PAT - 454 vs 407 cr, up 12 pc

Region wise breakup of H1 sales -

India - 77 pc

EU - 22 pc

Maxwell - 1 pc

Product wise breakup of H1 sales -

Suspension systems - 25 pc

Die Casting products - 45 pc

Disc Brakes - 12 pc

Alloy Wheels - 6 pc

Transmission systems - 3 pc

After mkt sales - 4 pc

Category wise breakup of H1 sales -

Motorcycles - 52 pc

Scooters - 9 pc

3Ws - 8 pc

4Ws - 30 pc

Others - 1 pc

H1 Capex @ 460 cr for India business + 223 cr for EU business

India capex includes - New Die Casting, brake assembly, alloy wheels, Aluminium castings and machining, Battery packs, Dual channel ABS

EU capex includes - capacities to cater to new orders from Stellantis, Daimler, Porsche and Audi

Company’s dual channel ABS facility is under customer validation. Setting up additional facilities in view of new draft regulations making ABS mandatory for 2 Ws over a period of time

Planning to expand ABS capacity to 5 X of current capacities

Plan to increase the 4W mix to 45 pc of consolidated revenues ( over medium term ) - contribution should come from both EU + India - making mkt share gains in braking systems, drive shafts, suspension systems

In H2 LY, company acquired 60 pc stake in Stroferle Ltd Germany with a plan to acquire the rest of 40 pc over next 5 yrs. It specialises in machined Aluminum die-casting for auto parts. Stroferle’s LY revenues were aprox 750 cr

Ex of contribution from Stroferle in Q2 ( as it wasn’t a part of the company in Q2 LY ), company’s topline growth would have been 7 pc vs the reported 22 pc growth

Capacity to make 1.2 million units of ABS are to be installed by Q1 FY 27. Another round of capacity expansion by 1.2 million units / yr shall happen when actual guidelines come out. ABS were already mandatory for 2W with engine capacity > 125 cc

Company has started civil work for setting up a new Chennai plant for disc brake systems, which includes the master cylinder, caliper, brake disc and brake hoses. Here they produce 3 million disc brake assembly systems + 4 million disc brakes / yr. Plan to take this capacity up to 7.6 million disc brake assemblies + 8.6 million disc brakes

Company’s new alloy wheel plant shall have a capacity of 3.6 million wheels / yr - should generate a revenue of 600 cr / yr. The new facility is already fully booked. Their existing alloy wheels plant produces 5.5 million alloy wheels

Company continues to position their new AURIC Shendra facility as a key point for critical machined castings for 4W and non-auto applications. They are therefore equipping this plant with highly sophisticated machining and finishing equipments. In the past, they mentioned about orders from marquee U.S. and UK-based OEMs and also orders from Valeo for electric platforms of Mahindra. And now they have added Yazaki as a customer taking the total sales close to Rs388 crores per annum at peak. SOP for both the U.S. and UK OEMs will start in Quarter 1 of FY 27 and they will reach peak sales in FY 28. The SOP for the AURIC Shendra plant is going to be in January 2026

Company’s subsidiary - Maxwell Ltd achieved a turnover of 74 cr in H1. They supply battery management systems for 2Ws, 3Ws, tractors and construction equipment

Company’s new battery pack manufacturing facility has already won business worth 300 cr / yr from a 2W OEM

The new alloy wheel facility of 3.6 million wheels / yr should reach full ramp up by Q2 next FY

Company is a leading manufacturer of inverted front forks for 2W OEMs. Company supplies these to 4 Indian OEMs and one International OEM ( KTM ). One Chinese OEM will start sourcing these from the company wef next FY. Should be able to sell 6.5 lakh inverted front forks in FY 26

Company has also started selling Solar Dampers. Have won business worth 200 cr from a Spanish OEM for their Solar Dampers. This business ca potentially grow multi fold going forward

Margin compression in Q2 in India business is on account of higher RM prices ( mainly Aluminium ) + higher investments made in their after mkt business

Share of power sourcing from renewable sources stands @ 28 pc

Current capacity that the company has to make ABS stands @ 0.65 million pieces / yr

Four wheeler suspensions is a very tough business to get into. Undergoing trials with one of the OEM. Company has a tech tie up with a South Korean technology partner. The system being developed by them is suited for small cars. Company is expecting a major breakthrough in near future. Company is already a leader in suspension systems of 2Ws

Company’s mkt share in front forks ( 2Ws ) is @ 43 pc. In the inverted front forks, their mkt share is even higher. In shock absorbers ( 2Ws ) , their mkt share is @ 45 pc

Company solar dampers business has a huge mkt potential and can also grow @ rapid rates. In talks with 2 more OEMs ( beyond the Spanish OEM mentioned above ). This can be a huge growth opportunity going forward

Similarly, battery packs is another high growth area which also has a long growth runway

Capex for H2 planned @ 400 cr for India + 200 cr for EU business

Disc: initiated a tracking position, not a buy/sell recommendation, biased, posted only for educational purposes