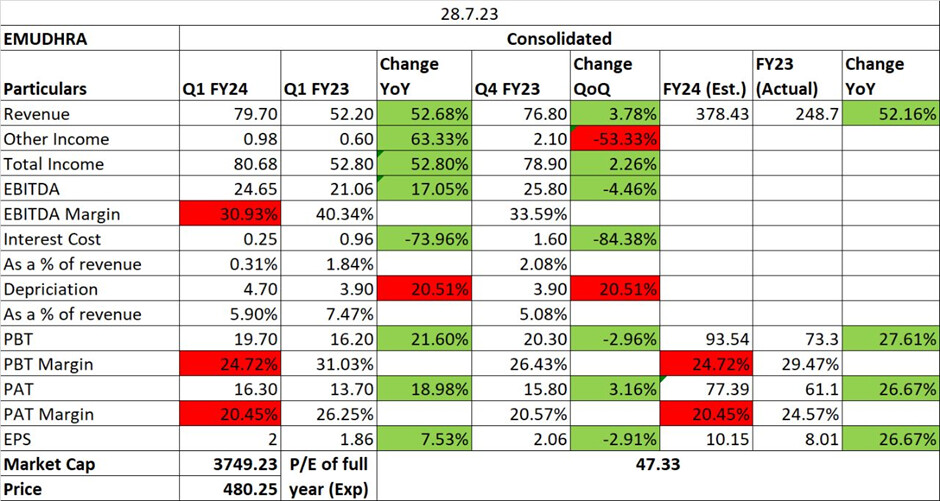

Starting they guided 30% growth with 35% + margin. Now guidance reduced to 25% and margins 20-30%.

1 Like

- Revenue growth driven by Enterprise Solutions in overseas markets.

- Despite investing in overseas markets for future growth, we have achieved strong EBITDA and Net profit growth.

- Sustained Net profit margin.

- The growth in the international business was supported by significant deals in North America, the Middle East and Africa regions for Enterprise Solutions.

- Cash flow operations, as a percentage of PBT, stood at 65%, slightly lower than the 66% reported in the last financial year.

- Channel pricing for Trust Services remained stable throughout the quarter.

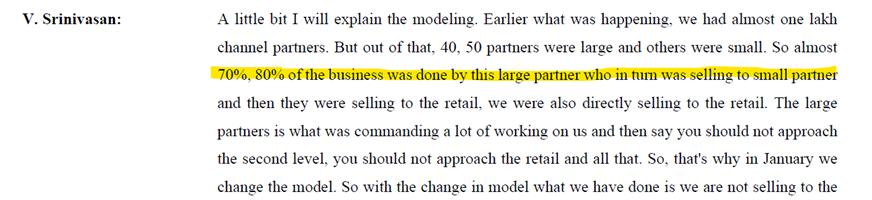

- The company’s strategic shift towards retail business and eSign has proven to be successful.

- Completed acquisition of Ikon Tech LLC, a company headquartered in Houston, TX providing solutions focussed on cyber security and digital transformation.

- In India, the trust services and enterprise solutions segments have shown an upward trend on a year-on-year basis.

- The order book for enterprise solutions in India remains robust, and they anticipate an uptick in the enterprise business as new government and BFSI projects are executed.

- They are optimistic about sustaining their growth trajectory and reinvesting margins into driving further growth.

- Revenue growth guidance of 25% will be achieved. Margins will be maintained at the same level. May increase by 50-100 bps.

- Moat of the business: Company has almost 1/3rd of its employees in R&D currently, so there is a high chance that they will keep developing a niche.

- Attempting to expand the certification products in the private sector market of the US.

- The company is also working with AWS to expand their network and help gain momentum in the upcoming quarters.

It is not that easy to switch to a new tech provider for KYC and digital signing solutions. When new tech stack is used, it has to undergo a complete audit. This is true for insurance, Banking and finance as well as government establishments. If the per unit cost of this tech that you use is insignificant compared to your overall product, then the company is not going to switch as the benefit a few bps in margins is not worth the risk.

Second, the company is not offering a single product but has multiple solutions under a single roof and this is easy for the client companies as they don’t want to hassle over this. There are multiple companies whose individual offerings are easily replicable but since they offer multiple solutions under a single head, they continue to be in business.

BTW, tech is never a moat as a lot if it is open source. Reliability and availability matter more here.

P.S. : I work in semiconductor tech and this behaviour is seen here as well whether it is us as the clients of tech or providers of tech.

3 Likes

Sharing some observations and your opinion on this may differ. I am not stating my opinion on the same.

Source: Concall FY 23

Source: Concall FY 23

Source AR 23

Source DRHP

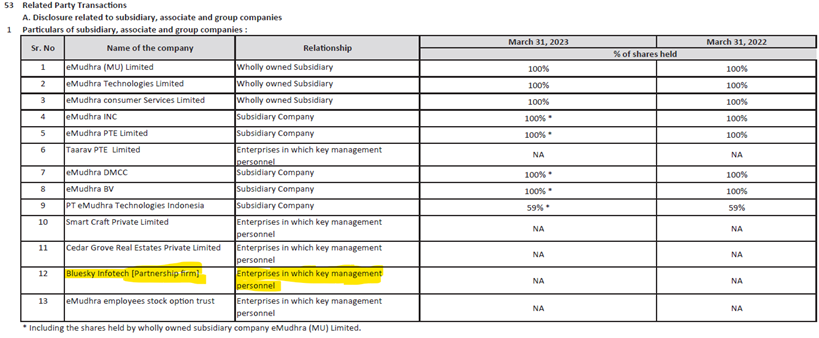

Who owns bluesky infotech?

you can check annual report on their website. Here is the link: https://shorturl.at/grDP8

Are you able to connect the dots?

Disclosure: Not invested

3 Likes

No not able to connect the dots, can you please elaborate?

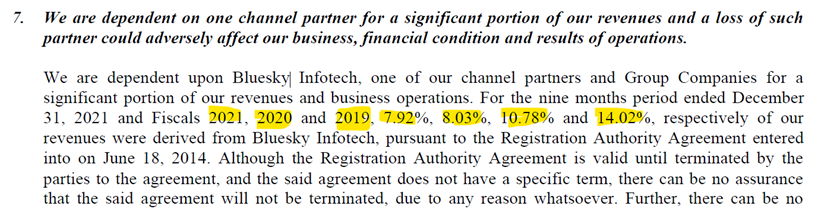

This is an opinion and not a fact: The company has approx 10% of sales coming from bluesky infotech, the realization this sales is just 10% of the actual realization ( done through direct channel). Bluesky infotech is owned by a related party. This is a corp governance issue in my opinion.

Disclosure: Not invested

3 Likes

Okay. Unfortunately the link isn’t working Akshay and my independent research on MCA couldn’t locate this firm either. But I guess that doesn’t matter as your inference is clear.

I have met the promoters personally and they seem very decent guys. While theoretically still possible I would say its unlikely.

Also note, it is a 280 Cr business of which about 80 crores come from DSC. This too they are on a trajectory of reducing the channel partner contribution. So I wouldn’t worry about this too much.

1 Like

You need not go on MCA. My link is not working. You can see the financials with signatures by promoters here https://www.blueskydsc.com/

You can also do some ground research on the realization of digital signatures. Numbers just don’t add up.

It is not about the amount, it is simply about the promoters intention. Why will I sell a product to a related party for 10rs if I can directly sell the same for 100rs? Why will I deprive minority shareholder of that much margin?

Disclosure: This is an opinion. Not invested.

2 Likes

I am an investor in eMudhra and thus biased but I am going to make a case for this company. Also I think an initiating coverage post was never made here. So here we go…

What the does the company do?

The company is in the business of providing trust in the digital world. This has manifested in various different forms but can broadly be classified between Public and Private. Public trust refers to scenarios where entities need to be authenticated over the internet, while private trust is needed where authentication is required within a private network of devices / servers.

Public Trust Solutions

- DSC: The Digital Signature Certificate is the oldest solution provided eMudhra where they behave as the Public Certificate Authority providing proof that the person signing the document is indeed the person who they claim to be.

- SSL: This is very similar for DSC, except while DSCs are made for humans, SSLs are made for websites, servers or machines.

Private Trust Solutions

- emSigner: This is eMudhra’s paperless transformation solutions where they digitize workflows of an organization along with providing secure digital tools for various approvals. The simplest example would be getting your expense approved by your boss before submitting it to finance for processing.

- emAS: This is their access management solution. It provides features like multi factor authentication and also allows restrictions to be placed on users basis their role and clearance levels. Think employees not having edit access to attendance records, while HR having it. Or Supply Chain team not having access to Marketing DBs.

- emCA: If a corporation has a large network of devices and usecases, getting them all certified by a Public CA can be expensive. Instead to ensure sercurity on their private network they may choose to set up a private CA for themselves that will manage the Certification for all devices, services, people within that network. The customer can also use this solution to become a public CA as well!

How does it earn?

The company has various business models running:

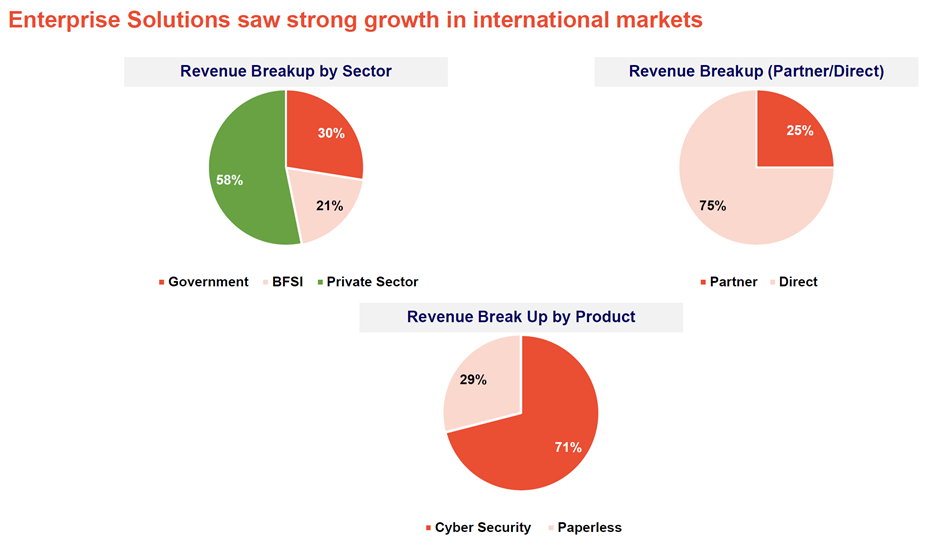

- Public Trust: Made up of SSL and DSC. Sold for a 2 year period (generally) at which point they need be renewed. These are sold via channel partners and also D2C. This is about 33% of the business.

- Paperless Transformation: Made up of emSigner. This is sold to companies on a license basis (basis number of users) and for a particular set of time (~5 years). There is an additional AMC fees associated with it which is recurring. Also license counts increase as usecases increase within the same organization. This forms 17% of the business.

- Zero Trust: Made up of emAS, emCA and some other products (e.g. emDiscovery). This is the same as emSigner in terms of business model and forms 50% of the business.

Hence, while 30% of the revenue is still coming from the DSC business, eMudhra has moved considerably away from being only dependent on that and is now in more in the space of Zero Trust security which is a much larger global theme being played out. This is a security approach where devices are not trusted even if they are part of the network and everything is authenticated. This become a preffered approach to mitigate the damage that a malicous actor can do even if they manage to compromise the security and enter the network (e.g. steal a laptop).

Total Addressable Market

- Public Trust: I am ignoring this because I don’t consider this a major growth area.

- Paperless Transformation: Generally considered a 8-10 B dollar industry growing rapidely (30%)

- Zero Trust: is a huge market, but the company has pegged the size for their products at about 15 B dollars.

Geographical Spread

eMudhra began its operations in India but quickly spread its market. We know that 45 to 50% of their business comes from abroad but country wise split has never been shared. It is reasonable to guess that currently major portion of this is coming from the Middle East, with Africa rising fast and their hope is to make US the largest market in the medium to long term.

Basis management commentary, it seems like MEA is a strong region for them and they have been present there for a while. They believe there is a lot more opportunity here to grow. However, nothing beats the scale of America.

They have been trying to make forays into the US for the last few quarters and this has been a learning curve for them. This is not to say that they have not managed anything: Management said that even this year about 60 Cr revenue should come from the US.

If and when they crack the American market, this can accelerate their top line quite significantly.

Right to Win

Their right to win is incredibly simple and powerful:

- They are cheaper compared to all their western competitors

- Are willing to work with th customers and fine tune their product for them

- Have stayed in these geographies for years and established credibility

Financial Track Record

The company has grown at 35%+ for the last few years and infact the last 3 quarters has grown at 69%, 53% and 65%. Its profit growth has not kept pace with the top line because I suspect the company has taken a conscious cost to increase BD expenses to scale faster. Their new benchmark is 30% EBITDA margins. In a couple of quarters the baseline will have adjusted and then profit growth will be in line with revenue growth.

The company is cash flow positive, no debt, and has an ROE of 22%.

Valuation

This stock is at 55 PE. If it continues to grow at 50-60% within 2 quarters it will be 30.

7 Likes

At 60% YoY growth rate for profit, it would take 4 quarter for PE to reach to 30

3 Likes

You’re right. I was looking at the wrong row.

But Management has given the guidance for 25%

1 Like

Yes they have in the long term. But they have also said they will hit 360 Cr this FY24. Which is a 40% growth. So it is likely that the growth in the next two quarters will be a little lower.

I personally feel the management is being conservative. And I also feel there is a great optional value here - because the day the US PMF is established; it can catapult the companies topline growth significantly.

1 Like

Any idea why eMudhra share price suddenly jumped during last couple of sessions with heavy volume? Is there any any news flow around it? The stock’s PE and PB seems very expensive. Any insights on why this sudden upmove?

Hike in stock prices

Emudhra- the recent price hike has been influeneced by many factors such as

In January 2024, eMudhra raised Rs 200 crore through a qualified institutional placement (QIP). The company issued 4.74 million equity shares at a price of Rs 422 per share

- total income increased by 59.5% on a YoY basis, accompanied by growth at 26.9% and 20.1% in EBITDA and PAT margins

- Dollar got stronger in last 3 days 45% revenue from overseas mkt

- 20% to 30 % cheaper producst in Us mrkt compared to peers.

- 30- 40% increase in order book last qtr

- 40% depreciation in tax last qtr

- Recievable closing time as financial year end

- In Q3 FY24, significant expansion in the international markets, supported by wins across various regions, driven by increased demand for our cybersecurity solutions

- rollout of e-signature platform for a large urban development company in Kingdom of Saudi Arabia, rollout of e-signature platform for paperless transformation of customs authority in the Middle East, upgradation of e-signature platform for a certifying authority and single window operator in West Africa, rollout of e-sign for bank officials of a large public sector bank for digitally signed approvals to enhance transparency

- The growth was primarily driven by the sales in the overseas market. There was a rise in the enterprise solution segment, which generated a revenue of Rs. 745 million,

- Almost it is 35% to 40% growth we have achieved in the order book compared to March

- 20% to 30% cheaper compared to competition because we are at a penetration stage.

- e US market development, we had spent some Rs. 2 crores, Rs. 3 crores of marketing.

- got quite a few wins in the SSL, TLS, and emDiscovery . large banks, stock exchange in India and some private sector clients. North America also recently, one IT company is using for private PKI.

- 40% depreciation from the tax perspective

4 Likes

Thanks for sharing this. Indeed helpful. But I was trying to understand the sudden spike on last Thursday and Friday. These reasons are based on Q3 results that was disclosed a few weeks ago. Hence wondering if there’s something new on this counter.

Anyways, today it is down wiping some of the gains.

2 Likes

Maybe expecting better Q4 results. so giving a rally before

Hi, A few queries:

- EBITDA margins have been going down, a year, year and half back, it was projected as a 35%-40% margin business, however, it has continuously declined and is currently at 25% (Dec 2023).

- Management has been giving the same reason of increase in employee cost due to incremental hiring in the international market, however, it is not reflected in the sales

- There were some RPT issues

- Nippon MF, CIF III Scheme I and some FPIs have subscribed to the QIP. What is the purpose of the new fund raise, is ant acquisition planned.

Thanks.

1 Like

eMudhra Q1 FY2025 Analysis: Key takeaways!!

eMudhra started FY2025 on an optimistic note, with total income increasing 17.7% year-over-year (YoY). The company saw strong deal momentum in India’s BFSI sector for integrated eSign and eStamping solutions, particularly for customer onboarding and lending workflows. The enterprise solutions segment generated revenue of INR 678 million, while trust services revenue was INR 246 million. Management expressed confidence in achieving 25-30% growth as projected earlier.

Strategic Initiatives:

- Global expansion: eMudhra is strengthening its presence in the United States, Europe, and emerging markets like the Philippines, Malaysia, and Kenya.

- Acquisition strategy: The company is acquiring TWO95 International to enhance its services capabilities and gain access to new customers.

- Product portfolio expansion: eMudhra is integrating email security capabilities through the acquisition of TWO95’s S/MIME certificate technology.

- Partnership development: The company signed a global partnership agreement with Tech Mahindra to sell cybersecurity and e-signature offerings.

Trends and Themes:

- Digital transformation in banking and government sectors

- Increasing focus on email security and identity protection

- Growing demand for integrated e-signature and e-stamping solutions

- Expansion of trust services and enterprise solutions in emerging markets

Industry Tailwinds:

- Increasing adoption of digital signatures and trust services globally

- Government initiatives promoting digital transformation

- Rising awareness of cybersecurity threats, particularly in email communication

- Growing demand for secure identity and access management solutions

Industry Headwinds:

- Regulatory changes affecting business models in the trust services sector

- Potential reduction in digital signature certificate demand due to changes in tax audit report requirements

- Delays in government projects due to elections

Analyst Concerns and Management Response:

Concern: Impact of regulatory changes on trust services revenue

Response: Management acknowledged a INR 6 crore dip in Q1 due to the new business model but expects improved revenue in coming quarters due to direct invoicing to end customers and potentially better realization.

Concern: Competition from new entrants like Protean eGov Technologies

Response: Management expressed confidence in their mature product offerings and deep focus on solving complex enterprise workflows, particularly in the banking and financial services sector.

Competitive Landscape:

eMudhra faces competition from both established players and new entrants in the digital trust services market. The company emphasizes its mature product offerings, deep industry expertise, and ability to handle complex enterprise workflows as key differentiators.

Guidance and Outlook:

Specific numerical guidance wasn’t provided, but the management expressed confidence in achieving 25-30% growth as previously projected. They expect improved revenue in coming quarters from trust services due to the new business model and continued growth in enterprise solutions across global markets.

Capital Allocation Strategy:

eMudhra is investing in enhancing its services capabilities and expanding globally through organic and inorganic means. The acquisition of TWO95 International and investments in data centers in Bangalore, Chennai, and Amsterdam demonstrate the company’s focus on strategic capital allocation for growth.

Opportunities & Risks:

Opportunities:

- Expansion into new geographies, particularly in emerging markets

- Upselling potential to existing customers

- Growing demand for integrated trust services and enterprise solutions

Risks:

- Regulatory changes affecting business models and pricing

- Potential reduction in demand for certain digital signature certificates

- Intense competition in the digital trust services market

Regulatory Environment:

The trust services sector is experiencing significant regulatory changes, with new business models being implemented. These changes require certifying authorities to invoice end customers directly and pay partners a referral commission, impacting pricing strategies and revenue recognition.

Customer Sentiment:

Management indicated strong deal momentum and customer interest across various sectors, particularly in BFSI, education, and government. The company’s ability to upsell to existing customers and win new deals in multiple geographies suggests positive customer sentiment.

Top 3 Takeaways:

- eMudhra is successfully expanding globally, with strong growth in enterprise solutions across Middle East, Africa, and the US.

- Regulatory changes in the trust services sector are creating short-term challenges but may lead to improved realization in the long term.

- The company is strategically expanding its product portfolio and service capabilities through acquisitions and partnerships to address evolving market needs, particularly in email security and identity protection.

3 Likes

I don’t think 20-25% growth, they are achieved? This space for 10-12% I seen yet.so their valuation now I don’t understand.also they are not alone in this space or not market leader or don’t have any pricing power, so how they are still at 90 time PE. or europe or America they are not base customer it was totally fake narrative. Pardon me if I am wrong here.

3 Likes