I prepared a small notes on Emmbi Industries:

Emmbi industries (previously known as Emmbi Polyarns) is one of

India’s largest speciality polymer processing comapny pioneer in

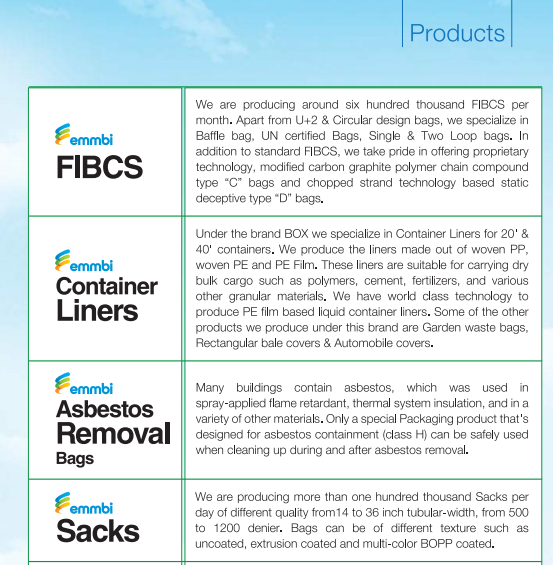

manufacturing and sale of FIBC (Jumbo Bags) and Woven Sacks and

various woven polymer based products like Container Liners,

Protective irrigation system, Canal Liners, Flexi Tanks, Car covers

etc. In addition to FIBC company manufactures various woven

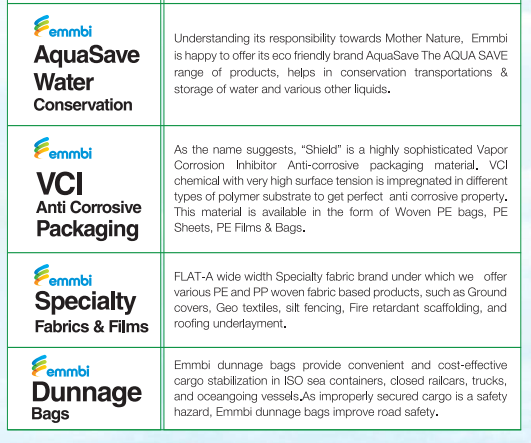

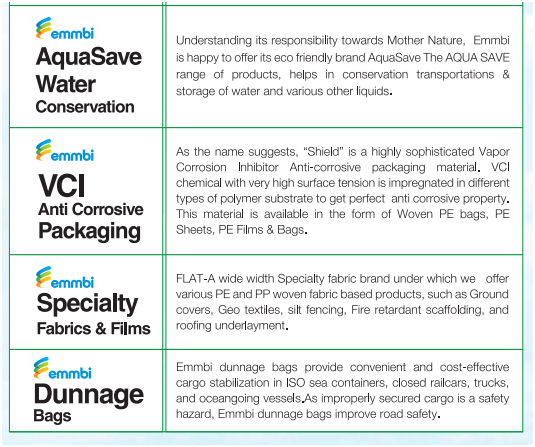

polypropylene products including Small bags, Box woven bags, Roofing

underlayment fabric, Courier bags, Ground covers, Silt fence and

Geotextiles & offer woven bags and fabrics in both PP and HDPE.

Their products are UV stabilized and pre-conditioned against

shrinkage.

The Company is involved in producing various types of Specialty

Bulk Packaging material for the Indian Market. In Domestic market,

remains one of the most active players for the packaging needs of the

E-Commerce Companies, FMCG Products such as Detergent Powder, Branded

Salt and Branded Wheat flour etc Major customers are from cement,

fertilizer, tea, sugar, seeds, food grains–Raw material etc.

It has a customer base of around 180 spread across various

countries. It has the one of the worlds largest fully intergrated

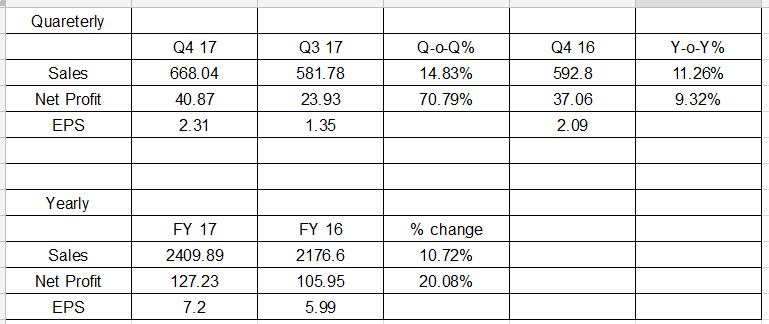

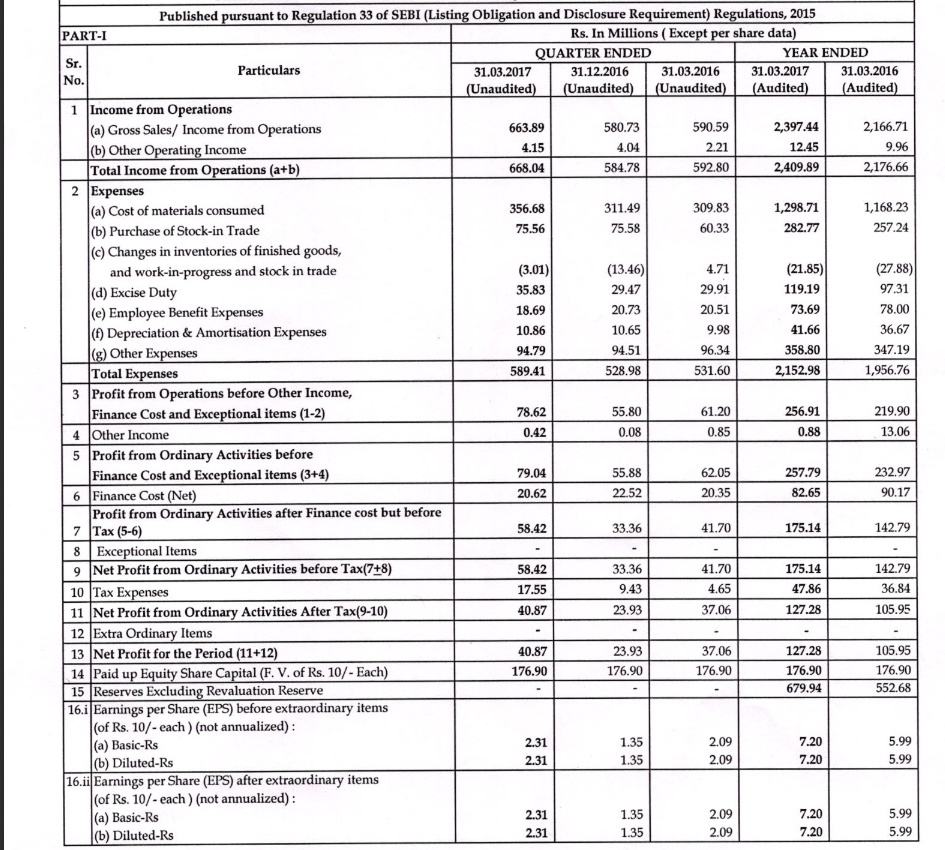

Woven Polymers plant manufacturing wide range of products. Revenue

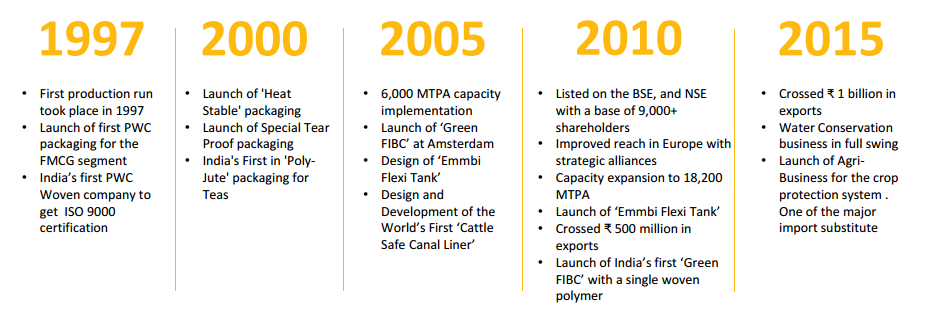

increased from 1 Cr in 1997 to 190 Cr in 2015. Last 3 years revenue

growth is at 18% CAGR. Profit had grown by 37% CAGR during the

period.

Have wide range of Product portfolio like:

- Flexible intermediate bulk containers

- Protective irrigation textiles

- Flexible and bulk water tanks

- Car Covers

- Geo Textiles, which are used in Chemical, Cement & Agriculture industries

- Water conservation products

- Packaging

50% of the revenue comes from Exports to more than 50 countries in US, Europe, South America, Few African countries, Australia, Middle East etc across 5 continents.

Exports from US, UK, Europe has increased by 55% YoY and Middle East increased by 400% (on a lower base).

Company is confident of showing promising growth in future from Export markets.

Owns Aqua Save brand which mainly have 2 products: Flexi Water tanks & Cannal and Pond Liners. They are exported to more than 12 countries.

Manufactures 6 Lacs Jumbo bags every month and over 1 Lac Woven Sack bags every day.

It produces 350 KM Fabric every day. Operates at 4 manufacturing plants in Maharastra.

India’s first Woven polymers processing company, who is ISO 9001 cerfified from past 15 years for designing and manufacturing.

Management to concentrate on Water conservative & Water transportation products where they find the potential.

There was an SEBI case on underwritter “Keynote Commodities” during IPO times involving the malpractises to increase the subscription of IPO for Emmbi.

Here is the link: Business News Today: Read Latest Business news, India Business News Live, Share Market & Economy News | The Economic Times 02/news/41008323_1_emmbi-polyarns-entities-sebi

With the raise of IPO money, promoters promised to estalish a annual capacity of 17800 MT, and actually had established 18200 MT.

Current revenue is 193 Crs, and doesn’t need any more capex till it the revenue reaches around 300 Crs.

Company has constantly paying the dividends since IPO. This year they have increased the dividend from Rs 2.5/- to Rs 3/-

Management is constantly buying the shares from Open market. It has bought almost 5.5% equity in the past 2 years.

Geographical Share of Revenue (i.e 50% of total revenue). They have achived a mile stone of crossing 100 Cr in Exports this year.

- USA: 37%

- Europe: 36%

- UK: 14%

- Oceania: 7%

- Asia 1%

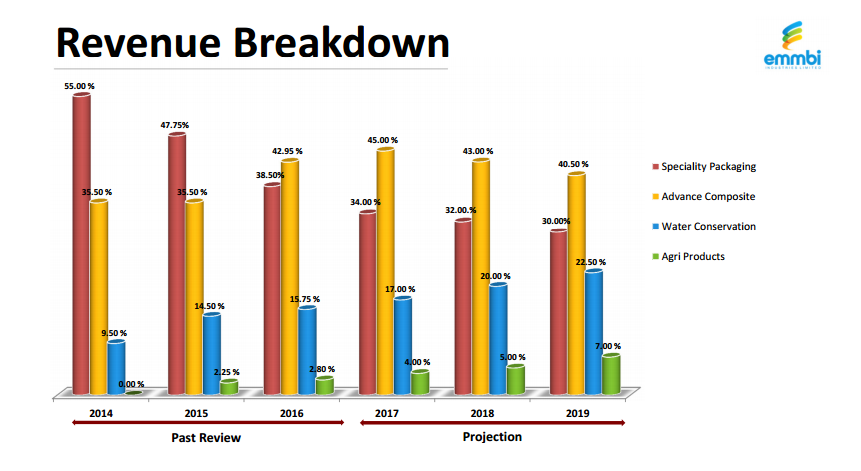

Products share of Revenue:

- Speciality packaging: 47.75%

- Advance Composites: 35.50%

- Water Conservation: 14.5%

- Agri products: 2.25%

EBITDA Margins moved from 9.8% in 2011 to 13% in H1F16

Last year alone, EBITDA margins increased by 31%.

ROE expanded from 5.6% in 2011 to around 13% this year

ROCE expanding from Single digit to 13% in H1FY16

D/E of 1.27

ROIC of 15%

H1FY15 vs H1FY16 has seen a Sales growth of around 21% and PAT growth of around 193%.

This is backed by the huge reduction in Raw material cost. In the same period sales inreased by 21%, where as Cost of Raw materials increased by 6%.

Also to mention here, for the same period during FY2014 to FY2015, the Raw material cost was UP by 12.5%.

Hence the decrease in Raw materials (mainly Crude) will have an positive impact on Margins going forward.

Current capacity utilization is 68% (as per the latest AR). This says that there is no major Capex requirement in the coming future. (As per the management, the current capacity will have full utilization by 2018).

Risks include:

- A very unorganized and a competitive sector.

- A commodity product and so called its brand “Aqua Save” is in initial stages and may take a lot of time to capitalize on its brand value.

- Dependent on global Crude prices.

- Thin margins. Margin expansion majorly dependent on the capabilities of the efficient management (which we can see are improving)

- No information from management on the Debt reduction. Even though it is not currently at scary level.

- We are not sure of how management going to deal with future Capex requirements (not immediately, but over a period of 18-24 months)

-END-

Disclaimer: Invested.

Regards,

Krishna Kishore A

)

)