• Sales: 30 – 35 Cr range for last 5 years

EBITDA: 12-16 Cr range

PAT: 8 – 10 Cr range (Margin 30%)

Cash equivalents = 65% of Market Cap

RoE ~20%

RoCE ~ 36%

• Debt free (both Long term and Short term), has investments in quoted securities and MFs worth 41 Cr as of 31/03/2015

• Single Product Company with total tapping solutions - only threads tools. Full varieties of taps - inter alia, include HIPerformance Thread Forming Taps, HI-Performance Spiral Fluted Taps, HI-Performance Spiral Pointed Taps, HIPerformance Taps for Cast Iron Tapping, HI-Performance Special Taps, PM Taps, Carbide Taps, Special Designed Roll Taps, Through Coolant Taps (T.C.H), Special Geometry ―Spiral Fluted‖ Taps, Special Geometry ―Spiral Pointed‖ Taps, Taps With Special Coatings among others are widely used in several critical auto components, ensuring the right product for each customer specific production requirement and timely deliveries has given us a competitive advantage in this high-precision industry

• Newly listed on NSE SME platform (August 2015). Listed at market cap of 60 Cr with an offer for sale of 25% from the promoters – objects of the issue being ‘gaining listing benefits!’

Given the margin levels (almost 50% EBITDA for FY15), there is some core competence in the business for sure.

Valuations cant be called expensive by any stretch of imagination. Annual report is now available.

RHP never makes forward looking statements, so future plans is a black box right now. However, machine tools is a mother industry to manufacturing in general. So the growth prospects are bright if there is faith in make in India slogan.

Untested, but worth a good look - as the section is called

Hi This may sound a bit silly. But how does one invest in companies listed in the NSE SME platform? I checked Kotak Trading account (i am an NRI) but this share isnt visible when I select NSE. There isnt a separate selection for NSE SME exchange - only BSE and NSE are the options. I faced same issue when I logged into a resident trading account on ICICI Direct.

Discl regarding the company and stock - not invested, but interested.

This company does not pay dividend but invests in stock market and equity mutual funds! whao! why not return money to shareholders? All of us can ourselves invest in stock market and mutual funds.

Hi Vinay: you can try SM segment on NSE instead of the normal BE segment.

Hi Ishank: Its been listed since Aug 2015 only. Unlisted cos of this size

never pay dividend to promoters by paying out dividend distribution tax. So

may be some time can change this?

I went through this and it looks like one of those too good to be true stories. The bulging receivables and inventories along with a dose of depreciation from renewables to avoid taxes an all too familiar story. Take a look at Shri Ganesh Jewellery House around 3/4 years back which ended by a defaulting client. My only advise is to be cautious and do your due diligence. By the way is there any reason for a promoter to dilute stake in a business with such great returns (debt would be far more cheaper than any OFS) ? Also make sure you understand the holding structure and non promoter holdings. Also take a look at the independent directors, are they really independent?

Co has paid Tax of 6 Crs. So the profits are genuine. Pray do tell me in how many Cos are independent directors really independent, not more than 200 out of 6000 listed.

Hi Anant: Please look at the “objects of the issue”, it says ‘to gain

benefits of listing’ Company didnt raise money, it was all secondary sale.

SEBI mandates them to sell 25% minimum. This objective is meant for people

who want to sell their stake paying STT thus saving capital gains. Surely

we are looking at an eventual sale out in the company. Of course, promoter

has a lock in and all that, but its clear why the listing happened. Given

the margin profile, sale may happen at seriously high valuation.

My view on IPO valuation is that since the offer for sale is promoters own

(last issue @ 192, see RHP) and its done at depressed valuation, likely to

save capital gains for the seller.

On the burgeoning receivables what you say is only half the stories. The

methods you indicating are accompanied by growth in sales which leads to

believe the company is aggressively growing. This is a company which

supplies to capital good and auto industry, and we all know how the topline

growth scenario has been off late.

My only word is caution I see several red flags in the story which makes it a strict no-no for me. Incase your conviction in the story and trust in promoters is high I am happy to be proven wrong.

The company has a tremendous operating profit margin/EBIDT margin in the region of 40%. Looks like too good to be true. The company is also debt-free, gives a small amount of dividend.

However, the company employs most of its capital in mutual funds and quoted shares!!! Out of the total shareholder’s fund of 120 crores, 80 crores are invested in mutual funds and shares.

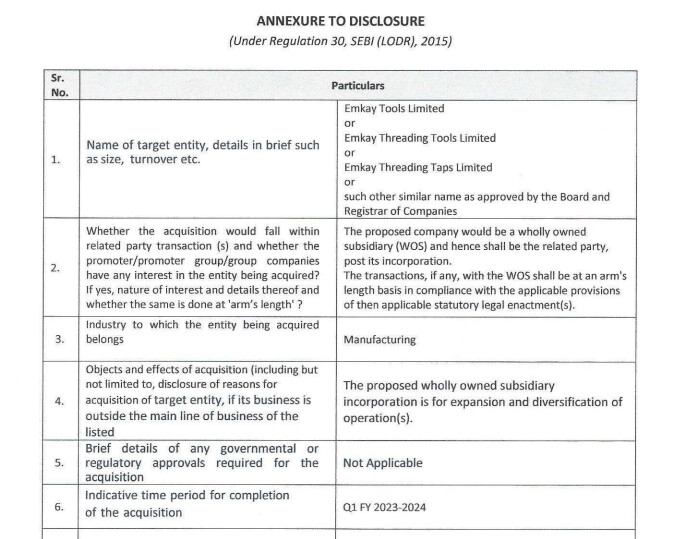

Recently, a WOS is formed for expansion.

Good growth, great OPM !!, Cash flow ok - seems money is coming into co and business is real.

160 cr in MF, PMS and equities. Almost nil debt.

EVEBITDA on TTM basis less than 3 !!!

RISKS :

No definite succession plan

No dividend and No special treatment to minority holders

No management interviews and information available is limited.

Everything made is put in equities

A buyback was failed in past.

Quite an interesting case to study and connect to management/factory visit/AGM.

This one seems to be running like a private company in the guise of a public company.

The company website https://emkaytools.com/ does not have any section for investors. Isn’t this a violation of the SEBI norms?

Promoter sold 3lakh shares towards the end of Feb 2020 (when the pandemic started). Extremely well-timed sale since the price crashed from around Rs 160 when he sold to around Rs 61 within 6-7 months.

75% promoter holding. No dividends. The valuation is very cheap but minority shareholders are unlikely to see their share of the profits.