I happen to speak to one of my friend in Lucknow, who is a real estate agent.

He told me there is an uptick in the no of units sold. He is doing around 10-12 units a month. Pre covid was around 18-20 units a month.

When asked specifically about Eldeco, he had no idea, as he is not dealing with Eldeco.

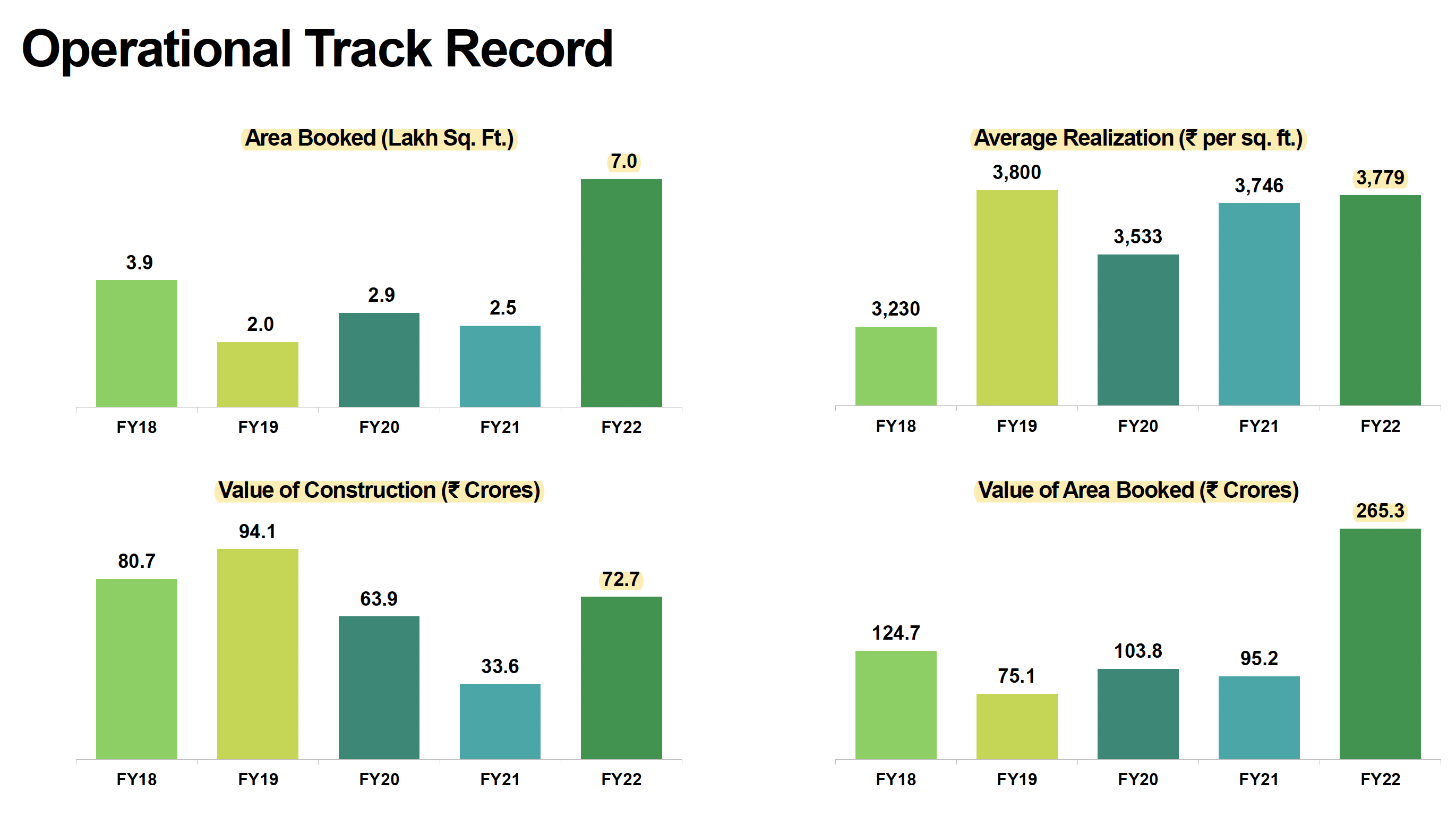

Eldeco did very well in terms of pre-sales, jumping from 2.5 lakh sq.ft in FY21 to 7 lakh sq.ft in FY22. They are now working on their project pipeline which can support this kind of pre-sales numbers. Here are my notes from today’s concall.

Will take a couple of quarters for new approvals to happen (thereby new supply to come in). Demand is very strong. Next couple of quarters, pre-sales numbers will likely be muted

Average realizations have increased from 3500/sq.ft to 4500/sq.ft this year. It appears lower in numbers as Q4 also had some sale of plotted land which comes at lower realizations

Construction costs: 40-50%, land costs: 20-30%. Overall trying to maintain gross margins (taking into account land + construction costs) of 40%+ which is much higher than peers

In affordable housing cos, construction costs are 70-80% of selling price. So increase in commodity costs affect affordable housing cos more than Eldeco. Eldeco is positioned towards the middle income segment with some premiumization element

Like the experimental project in Bareilly, company is looking at a luxury home project in Rishikesh, which will be positioned towards a second vacation home for HNIs. This will be announced soon

Imperia Phase I was sold out very quickly, have got 17 acre of land next to that. Approval process is expected to take a couple of quarters. Have not yet applied for Phase II approval as company is looking to add more land (increase from 17 to 25 acre) and go for the approval at one go

Eldeco City at Bareilly (40% Beneficial Interest) will not get recognized as revenues, only profit will be recognized. It’s because Bareilly project is <50% holding

Eldeco Luxa project was a premium project with 15-20% higher pricing than rates prevailing in that area. It took time for the market to accept the project, the company was able to sell well in FY22 and it’s no longer a slow moving inventory

Look for project specific IRR of 20%

Company was earlier maintaining 3-4 years land bank which has reduced to 1.5-2 years due to uptick in sales. Will look to bring land bank back to 3-4 years

How long does it take from purchase of land to getting all the approvals for project launch? Used to take 1-1.5 years earlier. Nowadays its lower at 6-9 months (3-6 months for local approvals + 3 months for environmental clearance)

How much of the saleable area of 13.23 lakh sq.ft can get launched in FY23? Half of it (Imperia Phase II and one of the two group housing projects)

With the current management bandwidth, how much can Eldeco grow? Can easily double or triple pre-sales numbers with the current setup. Only constraint is on launchable project

Project construction is completely outsourced to local contracts

Fixed costs are likely to go up from 3-4% of sales to 6-7% as sales scale up

Less than 1 year supply in overall Lucknow market, the market is undersupplied

Out of the 5 forthcoming projects, confident of launching 3 in FY23 and further adding 3 more projects to the pipeline

Current pipeline is about 750 cr. (3-3.5 years of project pipeline) and will add to this pipeline

Have seen price increase of 10-15% in apartments and 40-50% in row housing & plotted development projects in last 18-months

Not averse to taking debt for construction finance + land acquisition. Have built a sizeable cash position and will be happy to use judicious amount of debt for building pipeline. Don’t intend to go beyond 1x on debt to equity

Hope to double pre-sales from 250 cr. in FY22 to 500 cr.+ by FY25

Disclosure: Not invested (no transactions in last-30 days)

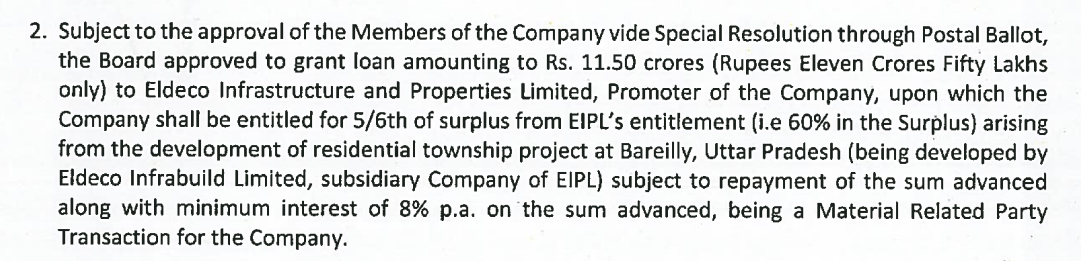

Can anyone explain the above resolution in simple language?

Is the company loaning to the promoter? If yes why? What kind of business is this ? Also, how is 5/6th of surplus related to 60% in the surplus?

Revenue Rs. 109Cr in FY18 vs Rs. 127Cr in FY22.

PAT Rs. 24Cr in FY18 vs Rs.50.8Cr in FY22.

Is it sustainable to grow profit without growing revenue in this industry?

Last 5 Quarters PAT and PAT margin has been falling.

35 Subsidiaries and only 6 are profitable. Omni Farms Pvt. Ltd is the only big subsidiary.

Can’t really understand the competence of the company?

In my view, the company is just selling high-priced real estate. The company is just creating many subsidiaries with negative reserves and unproductive assets.

Really doubt the company’s ability in cost-cutting measures and expertise in the technicality of building real estate. I am unable to see how these subsidiaries are maintained and why they are so unproductive.

Standalone vs Consolidated difference in inventories is 42%.

Standalone vs Consolidated difference in PAT TTM is 20%.

Disclosure. Invested unsatisfied with my investment. Really doubt the real estate industry. Can’t understand the business model? The company seems shady.

Demand in Lucknow is strong, market is undersupplied

3 land parcels have reached term sheet stage in Lucknow, 2 are in primary land aggregation and 1 is prime group housing

Total inventory: 4.68 lakh sq.ft (in on-going projects) + 14.12 lakh sq.ft (in upcoming projects; 700 cr. potential sales) + 3 term sheets (500-600 cr. potential sales)

Drop in EBITDA margins was due to reversal in GST credit (5-6 cr. impact)

Group housing projects are lower margins vs plotted large township projects which are based on land aggregation model

Will launch 2 projects in FY23: Imperia Phase-2 (4.55 lakh sq.ft), 1 group housing project in Eldeco city. These two should contribute 450 cr. in topline in next 3 years

Will increase beneficial share in Bareilly project to 50% from current 40% due secondary purchase of shares

Currently focus in on getting more projects in Lucknow rather than venturing out to other cities

Average realizations have improved to 4500/sq.ft

Bareilly: 40 acres of land, have approvals for 35 acres and for the remaining 5 acres, will apply for approvals. For the 35 acres, presales have done very well (sold 5.83 lakh sq.ft of 8.74 lakh sq.ft available). Currently prices are around 4000/sq.ft (vs 2500 at time of transaction)

Disclosure: Not invested (no transactions in last-30 days)

In 9M FY23, have purchased additional land of 16.52 acres (for Imperia Phase III) + raised beneficial share in Bareilly project from 40 to 50%

FY23 Launches: Only one small project was launched so far in FY23 (Twin tower; 1.57 lakh sq.ft out of which 0.95 lakh sq.ft was sold worth 38.8 cr.). Plan to launch two additional projects in Q4 FY23. All other pre-sales were from sustenance inventory

Near term launch pipeline: Eldeco Imperia Phase II + Eldeco Latitude 27 (9 lakh sq.ft with 400 cr. revenue potential). Will take 4-6 months to launch (rera + environmental clearance required)

Within next 12 months, will launch projects worth 800 cr. Booking value at launch is around 50%

Only 25-30% of homes are sold on loans

Should be able to do presales of 300 cr.+ in FY24 (~1mn sq.ft)

40% EBITDA margins are only possible in plotted development and not in group housing. Currently EBITDA margins are higher due to higher contribution of plotted development. Going forward with increasing contribution from group housing (50% contribution), blended EBITDA margins will reduce

Disclosure: Not invested (no transactions in last-30 days)

Demand in Lucknow is buoyant, supply is a problem due to lack of new launches

Due to lack of new launches, pre-sales was low at 93 cr. Launches suffered because land assembly issues took longer. Company has advanced 25 cr. in these projects

Have witnessed interest from real estate funds who want to enter Lucknow and might use them to fund newer projects

Positive side of this delay is that prices have increased and launches will happen at price points higher than original underwriting

Added land bank of 20.91 acres in FY23

Received RERA registration for Latitude 27, which will be formally launch in Q1FY24. Imperia Phase 2 will be launched during H2FY24

Have signed two new projects where land assembly and approvals are under process, will announce them next quarter

Plan to raise debt (upto 100 cr.) for new projects

Total inventory: 9.22 lakh sq.ft (in on-going projects) + 10.95 lakh sq.ft (in upcoming projects) + 2 term sheets

Current saleable volume is ~2mn sq.ft. At avg realization of 4500-5000, it will give potential revenue of 900-1000 cr.

Realizations have increased to 4600 (20% vs last year). Expect 10% increase in FY24

FY24 delivery: Imperia Phase I (by Q3FY24)

Will maintain 50-50 split between horizontal plotted development and group housing

Dividend payout has increased to 18%, aim to take it to 25%

Don’t believe affordable housing is a sustainable business model as margins are very low

EBITDA margin in newer projects will initially be 30% and increase to 35%

Disclosure: Not invested (no transactions in last-30 days)

Have acquired 3 acre of land for Eldeco Trinity, this was a recent deal and they hope to launch in FY24 (can also get shifted to FY25 depending on approval process)

75-80% of inventory that was opened was sold in Bareilly project

Will require 200 cr. for project investments in FY24, will raise 100 cr. debt from Piramal with early repayment option

In horizontal development projects, ~25% of inventory is blocked by authority, which gets released once they deliver the projects (after receiving OC)

Horizontal development costs: 2-3 cr./acre land; 2 cr./acre for development; 1 cr./acre for getting registrations & 1 cr./acre in overhead costs

Approval process in Uttar Pradesh and Haryana is getting elongated which is actually benefitting company right now as their actual launch prices are higher than earlier planned

Given the city land prices are high, focusing on high rises within the city

Disclosure: Not invested (no transactions in last-30 days)

Eldeco came with a muted set of nos, they are very confident of crossing 200+ cr. of presales in FY24 on back of 3 new projects (1 already launched, 2 in pipeline for FY24). Concall notes below

FY24Q2

Eldeco Latitude 27 was launched this quarter (5.17 lakh sq.ft total area), it has 5 towers of ~1 lakh sq.ft each. Have opened 2 towers (~2 lakh sq.ft) and will open 3rd tower in current festive season. Sold 41 units (36 cr., 73,766 sq.ft) and allotted 44,200 sq.ft to partner

Eldeco Trinity (high rise; luxury group housing in Shaheed path): Seeking RERA registration, will add 5 lakh sq.ft (received layout/map approval). 6500-7500 sq.ft realization

Eldeco Imperia Phase II: Received layout/map approval, expect RERA approval in next few weeks (6.3 lakh sq.ft). Imperia Phase I last sales was done at 4200/sq.ft, expect 4000-4500 sq.ft realization for Phase II

In group housing projects, EBITDA margins will be 25-30%

Acquired 18.1 acres of land in Q2

Raised debt of 160 cr. from two lenders (Piramal, ICICI), 80 cr. has already been allocated and deployed

Disclosure: Not invested (no transactions in last-30 days)

Total booking area: 3,22,831 sq ft (135.24cr)= realisation (2387/sq. feet)

Delivered= 56.6k sq feet (q); 1.53lsf (9m)

Applying for CC : Eldeco Imperia, E. Twin Towers

Imperia 1: total saleable area:3lsf

New Launches

E. Trinity (high end)

E. Imperia Phase II (received 101 bookings in pre-launch for 1,28,450sf ; avg realisation was 3500sf

New land parcels

3 new pieces; hope to conclude land assembly and aggregation in 6m

Total land acquisition in 9m= 63acres

Other highlights

Lucknow developing swiftly; however Slow approvals; unable to meet demand; hence hardly any inventory in market

If they open 100 bookings demand is for 200 bookings

At present increased land prices are not leading to margin pressure as able to pass on to end users, however cognisant that this might start hurting margins later when unable to pass the increase in land prices

D/E is 0.3

If money is needed they can manage if required apart from debt can also raise funds in a SPV format from PE funds or AIF’s who are keen to invest

avg time to get CC can be 1-3months after filing.

hope to launch 2 other projects by end of next year from the new aggregated land however unable to commit.

no new cities or areas being considered as find good demand in Lucknow for next few years.

I am sharing few facts that i came across while reading about some of the projects of Eldeco.

This is a project in Noida

First i was happy that Eldeco is doing a project which is selling it around 10-11000 per sqft.(checked offline)

After taking a closer look came across this

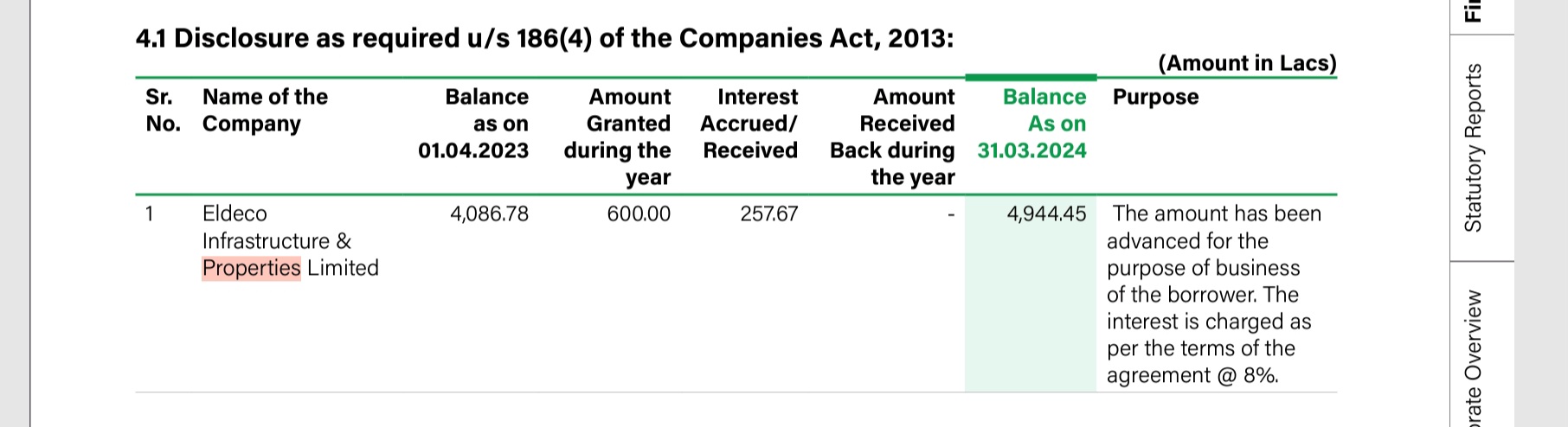

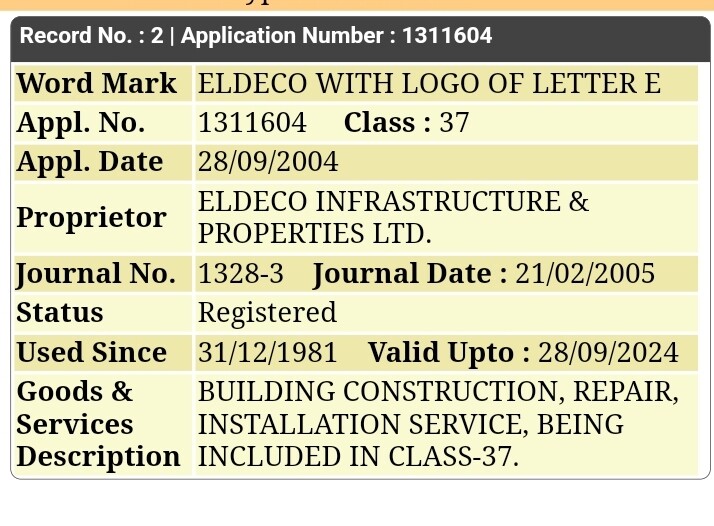

This project is using ELDECO brand name but is not a subsidiary of the listed entity. It is a separate company called Eldeco infrastructure and properties limited having the same KMPs.

Reading through the annual report, i found that this company owes ~50 crores to the listed company and accrues interest at 8% pa.

8 percent!!!

Speaks a lot about intention. The related party could have sold its 0.51% stake to repay that cheap loan.

One more mystery that i encountered was eldeco la vida bella project.

This project is on their website. This project is currently quoting 10,500-11,500 per sq ft in market.(checked offline) But the promoter of this project is entirely a new firm called Eldeco Real Estate ltd, which is neither subsidiary nor related party as per annual report of the listed firm.

Then why this project is listed on Eldeco group website? Why are they using same logo? According to govt data eldeco trademark is owned by the listed firm

No royalty is being paid to listed firm either from related party (Eldeco infra & properties ltd) or the unrelated party (Eldeco real estate limited).

These are only 2 projects that i have discussed. Please do your own research before trusting your money with such promoter.

Before forming opinions on the promoter and highlighting potential issues, it might be helpful to first review the initial post on this thread, which outlines the situation (see below). The listed Eldeco operates primarily in Lucknow, while the unlisted company, which is significantly larger in scale, has operations in multiple cities. This is common knowledge, and nearly every conference call includes questions about this. Pankaj has consistently stated that this structure is unlikely to change in the near future.

Disclosure: Not invested (no transactions in last-30 days)

FY26 is expected to be a big launch year, with presales guidance of 400 cr. Land aggregation seems to be finishing now.

FY25Q3

Q3 EBITDA margins were lower due to revenue recognition from Imperia Phase 1 which generated 17% margins as they front loaded club and infra costs in Phase 1. Phase 2 EBITDA margins will be 45-50%. Believe their sustainable EBITDA margins are 32-35%

Launched a new wing within Eldeco Latitude 27 in Q3

Acquired 7.3 acres of land in Q3

Available sale inventory in launched projects: 9.3 lakh sq.ft

Pipeline: Will launch 2 new projects (Hanging Gardens, Skywalk) with 6 lakh sq.ft and realizations of ~6,000. Aggregating land at 3 more locations and plan to a big launch (~600 cr. @5000/sq.ft) in one of those locations during later part of FY26

The new normal for realizations will be 5000-6000 / sq.ft

Targeting annualized presales of 400 cr. in FY26

Sales velocity is good across projects, they see greater traction during launch where 50-60% of inventory gets booked vs earlier where sales were staggered throughout the project cycle

Macro: Lucknow absorbs 2000-3000 units/year and they believe it can easily double if supply comes. Pune: 60-70k units/year, Chandigarh: 4000 units/year

Disclosure: Invested (bought shares in last-30 days)