Eicher was in steroids last few days. With new 52 week highs everyday, 21k got taken out today. Another pattern I had observed is that stock takes off around 1st of each month, when the SIAM numbers are released. 48% y on y growth was dancing in front of buyers, on monthly sales.

Veterans. We are within a shouting distance of the 3 fig mark in PE. Where are we heading ? Also, I haven’t looked at vol comparison. Are these highs with increasing volume ?

1 Like

I would suggest to put up a estimate for CY15 numbers here, in terms of revenue, margins, EBITDA, PAT and EPS.

The sales number are coming pretty strong and without much volatility, so i think this may not be a very high risk exercise.

This should give us a good indication of forward PE, historical PE is well history.

Regards

Raja

@rajpanda…let me take the easier route of starting with a few brokerage reports and take things from there

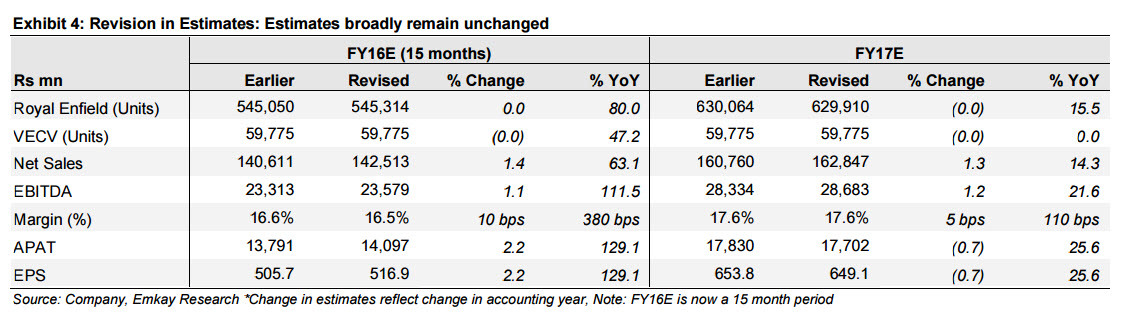

This one is from emkay…and it will look at a forward PE of 32.6, if we consider the FY17 projected EPS of 650

Buy Eicher Motors; target of Rs 18100: Emkay

1 Like

Kalyan,

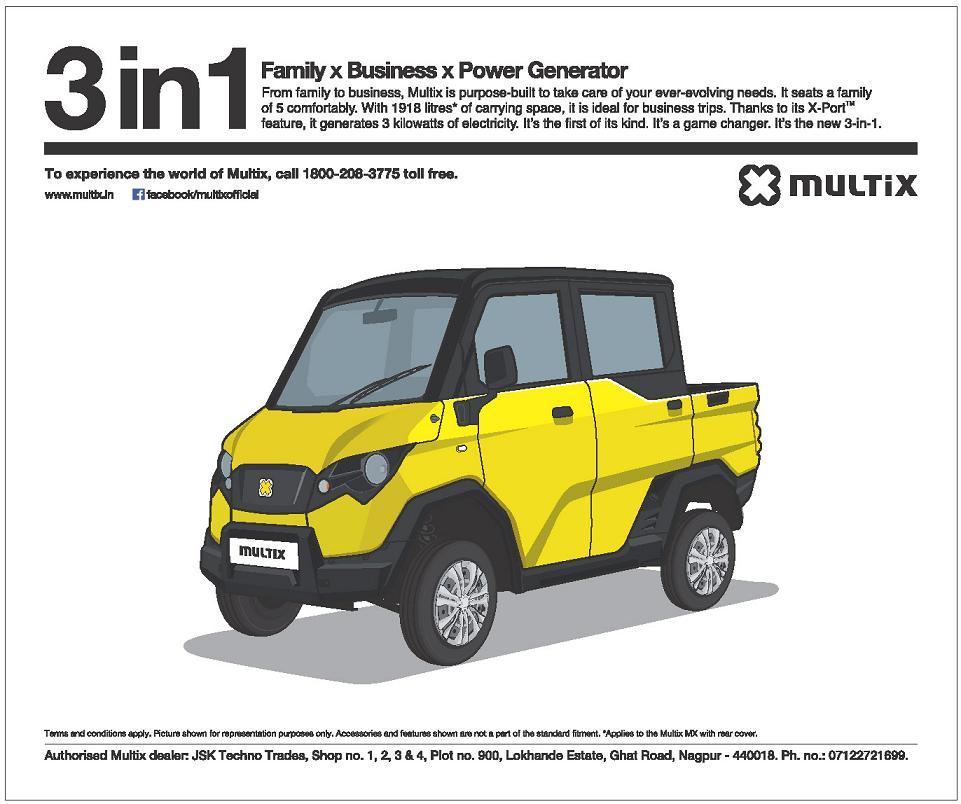

After going through Multix power generating feature, it just reminded one of Bollywood blockbuster, 3 Idiot were Rancho was planning to develop an inventor which can generate power from batteries.

Eicher-Polaris has implemented same with Multix. With Royal Enfield (Two Wheeler), Mutlix (Personal Utility) and VECV (Commercial Vehicle), the company also appears to ride on 3 Idiots growth. Like the movie which was one of the excellent entertainment produced in 21st century driving into block buster collection, I wish., even Eicher would have a great business (with 3 Idiots) and generating great wealth for all stakeholder !!!

Any thought?

@dd1474 like your analogy. The themes are simple and execution and track record of the firm is well known. Hope Lal proves to be the AK of our dreams

Royal Enfield, India’s oldest bike manufacturer, will sell 200 limited edition units of its most popular motorcycle Classic 500 through the online medium only, a first by the 115-year old company.

1 Like

This presentation from Prof. Bakshi talks about many businesses that we follow on VP and is a absolute brilliant read for investors. Posting it on this thread as he has made some glowing praises for Siddhartha Lal.

6 Likes

Good good write-up Raj. Thanks for sharing

Thanks for sharing worth watching and great learning experience.

Eicher to increase RE production capacity to 52k per month by December this year. That’s 624,000 capacity for next calender year vs 4.5 lac production target for CY15. Takes care of ~38% unit growth demand for next year.

1 Like

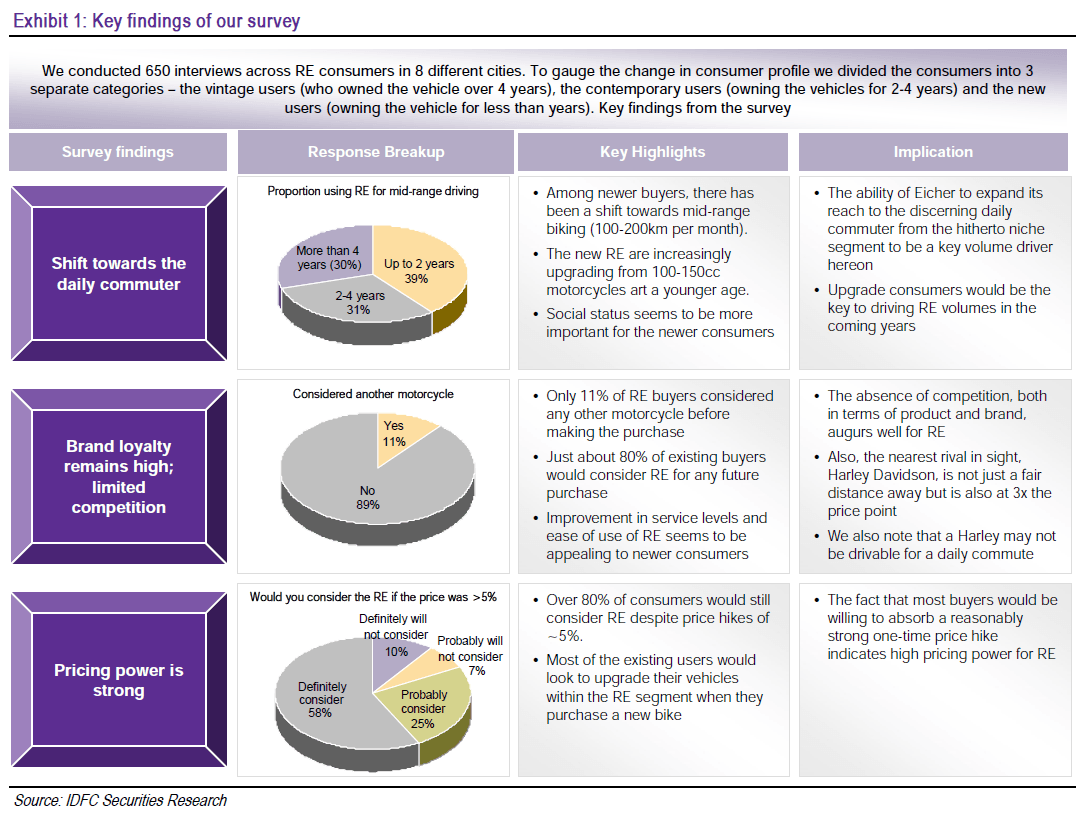

IDFC has came out with buy report on Eicher with target price of Rs 24,802/-. They have conducted survey of around 650 RE buyer. A friend of mine has shared with me key summary of survey which is as follows:

3 Likes

Ties up with Chola for financing Multix. Step in right direction I would think.

The news flow on Eicher has been so brisk, it’s getting difficult to post each and every news item. Media, it seems, have been giving them a free ride. Every day there is a news item!!

1 Like

The survey about buyer profile changing from enthusiast to daily commuter is big news indeed.

If that is to be true, I think we should expect a minimum of 10% market share.

Transitioning from being the choice of the enthusiast to that of the commuter has ramifications beyond merely gaining market share. The most important one is that it will no longer being the premium bike with aspirational value. This might dilute the pricing power that the brand Royal-Enfield commands today. There is always a premium attached to a product where supply cannot keep pace with demand. Should this transition happen, I figure that at some point the rich valuation of the stock will revert to a point where it is more in line with normal valuations. The stock might still go higher, but the earnings will be working much harder than today to deserve that price.

sold 200 bikes… now bikes are selling online!!!

@rajpanda, @punitm306 @sammy11 @nikrod12,

After almost a year, Eicher continue to show more than 45% growth in RE sales. However, CV sales did not seen major revival at least for Eicher. Another positive development is a new launch of Multix and a globally renowned design company acquisition.

We see market Cap of around 56,000 Cr with Consolidated TTM PE of nearly 80 times. Assuming FY16 EPS of around 425, Giving forward PE of around 50 times.

In my view, the growth engine in RE continue to ride with Eicher reporting highest EBIDTA margin in global Automobile business in standalone RE business, the PE is justify. Just wanted to get your perspective as well since you were familiar with previous discussion. I also respect your opinions and hence want your view point as well.

Dicl: Largest holding in my portfolio and continue to hold same.

1 Like

Hi dhiraj,

This is one story which has turned out way better than I initially thought. One key thing in my mind, even 1.5 years back, was the order book for a consumer product, which I thought was highly unusual in current times. That gave visibility of revenue & company seemed very capable of running operation efficiently and generating excellent returns. Cut to now, seems nothing of that has changed except valuation. On the other hand understanding and conviction on the story has only got better with time.

- An increasing number of mainstream/daily commuters are accepting RE as a vehicle of choice.

- The core customer base of enthusiast young riders and affluent car owners joining leisure biking continues to do well.

- This is one company which charges people for marketing it’s product (think of Hiamalyan Odyssey, ) and it shortlist’s participants who can have that privilege. Think of the customer loyalty and brand ambassadors it’s generating for the product via such initiatives and in the process staying close to it’s customer base and listening to their needs and aspirations.

- Management has started to make some excellent moves for international market. Just think of the global potential. Take a look look at Bajaj’s exports with essentially a “me too” product, which mostly sells in developing world. RE is starting from top end markets and gives a feel there is a long way to go. Commuting though is an essential human need, “moving the soul” is no lesser a need !!

- I think the company can reach a 10% market share in domestic market and that’s the cake. In my mind that’s a reachable target, don’t the ask the logic

and icing will be the international market.

and icing will be the international market. - On the CV side, looking at the pick up in volumes from AL i too feel strange that VECV hasn’t picked up as strong. But if you see mgmt. commentary, they believe themselves to be little ahead of time in terms of modernization in CV fleet and expect that when market catches up with the modernization, they will be the leaders. Am kind of trusting mgmt. instinct here. That’s the broad international trend as it’s beneficial for customer too over long run with the only pain point being more investment upfront.

- Multix seems to be an excellent addition and am waiting, as others, to see market reaction when it’s available for sale form Aug.

and icing will be the international market.

and icing will be the international market.Only problem with the story is valuation has got way ahead of fundamentals as we like to call it. For fresh allocation it’s a problem. Am holding all quantity and this is my highest allocation as well and not planning to sell it soon at anywhere closer to these levels. May add around 35 times forward if the story continues.

That’s from my side, hope to hear from you and other guys as well

2 Likes

My 2 cents in addition to the above.

Eicher is one stock that has performed exactly contrary to my reading. I had bought it as a basket along with Ashok Ley and Tata motors to play the CV theme. Gradually I realised the strength of the RE brand and now my thesis has turned over its head. It is now through and through an RE story with the CV being only the icing which will add to the sweetness. Valuations sure look high, but if the CV story starts playing out it can quickly add to the EPS and moderate the valuation.

Kotak securities in this report (http://www.moneycontrol.com/news/stocks-views/sell-eicher-motors-advises-hitesh-goel_1993521.html) vouch overwhelmingly about the management executing the story very effectively, and surprisingly have based their sell decision purely on valuations. I have a feeling they may go wrong on this. Eicher (along with Page, another of my holding) will be live test cases for all the Guru speak of holding on as long as the company is doing well which can make the stock overvalued. In the process we may have to live with poor relative underperformance compared to some of the other stocks. Portfolio returns may get affected, but I, for one, am willing to bear with it as it may be only temporary.

I feel the following are key monitorables in the story:

- RE waiting period – reducing waiting period to say 1-2 months would be an indicator of sales catching up with demand.

- CV sales

- Performance of the Polaris vehicle

Am no expert to suggest when to buy. It may not come down to any lower PE estimates we may have. It may time correct, it may fall, who knows. But it is one of the few stocks with a fair amount of visibility for the future (3-5 years). I know sceptics would compare with Infosys of the dot com boom, but my view would be that Infosys at that time was probably growing at an unsustainable rate, whereas Eicher isn’t.

But… only time will tell.

FYI: Have been investing for the last 3 years.

This has done an amazing job for the last 10 years, growing strength to strength. But looking at the PE I am having nightmares about it’s pe. As mentioned above, I have no ability to justify new purchases and it’s killing me since they have done so well. A constant concern now of mine is the high sensex pe, and my feeling that the market is fully saturated. How do we move forward with this story. Sitting on the sidelines is no fun.

Sanjay