Superb results. Last 12 months profits at Rs 214crs. At current market cap 3556crs stock trades at a cheap 16.6x P/E

2 Likes

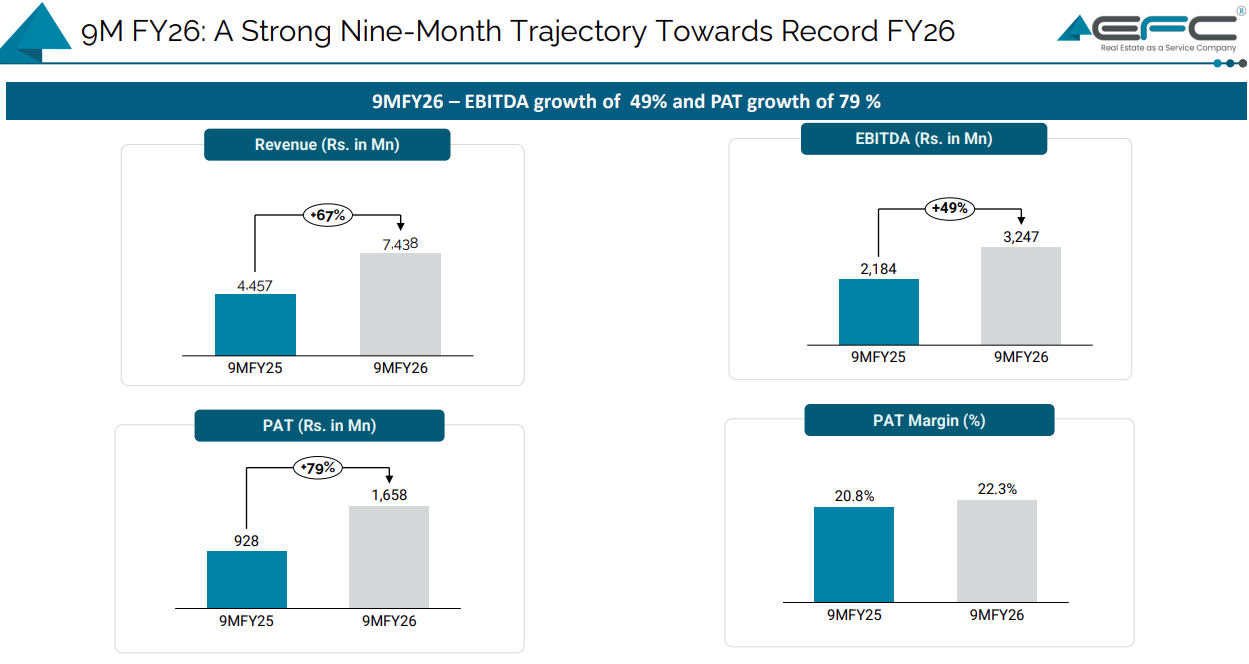

Few concerns from the investor presentation:

- Rental segment - The billed seats / Total seats ratio has decline YoY which is not a good sign, looks like company doesn’t have good visibility on occupancy and is being conservative.

- They had committed a target of 92k seats by FY26 and then walked it back to ~78-80k and not if they want to reach that target, they need to develop their highest seat quarterly seat addition in q4

- Instead of a steady, predictable and low working capital cycle rental business, the growth is majorly coming from design and build and small extent from furniture business both of which will dilute the margin and are working capital heavy businesses

- Furniture segment - Current capacity utilization is still low compared to earlier claims of 200 Cr yearly sales and 250-300 cr peak utilization and with rental segment’s slow growth, the backward integration is slow

- Company has started to acquire properties on its own book which is a good idea if they can get properties at a low rate but it exposes them to downturn risk somewhere down the line which must be adjusted in the valuation multiple

Other concerns:

- Company uses it own depreciation policy instead of standard ind-as one which is dissimilar ahd higher than Awfis and DevX. This inflates profit to some extent

- Management integrity - The subsidiary deals are a red flag and no explanation seems justifiable. They incorporated a subsidiary with a lot of management stake separately in a listed company and funded it with capital / loans from listed company without any risk to promoter. When the company started working, they merged it and got a boatload of money

- Brokerage fees to related parties - They are paying a lot of brokerage fees to a subsidiary of TCC Concepts which is a material %age of TCC’s revenue.

- Pepperfry deal - They acquired Pepperfry in Oct at 659 Cr but now raising money 4 months later at 1600 Cr from Sageone, etc. How is that possible? Probably a lot of losses being absorbed in TCC, preference shares to clean up the business and TCC shareholders getting hosed (this is a hunch). Exclusive: Pepperfry to raise $18 Mn funding in down round

The only good thing is the valuations which seem to price in a lot of these risks it seems.

4 Likes

Disc - Not yet invested and not yet biased

3 Likes

People are exaggerating fear of AI instead of taking as force for development.

Following articles gives better idea, especially, how India will get benefited from recent FTA/AI deals. Companies in the managed office space Q3FY26 result is proof of the momentum in office demand. In con call of all managed office space companies are bullish on demand and there is no sign of slowdown.

2 Likes

what are the members thoughts on the AI effect on the reduction in white collar jobs and also on co-working companies ?

Acc to management this will motivate the tech companies to rent more seats instead of doing own capex .

1 Like

I have very similar opinion. GCC’s would continue to boom as AI advances would be used to replace high cost labour in the developed countries to get the maximum benefit of AI. Whatever minimum manpower requirements would be there, those would be fulfilled through the GCC’s of these global organisations.

1 Like

What’s going on with the stock price? So much selling with so low volume. If ace investors liked it at 290 then it’s cheap at 184

They are planning for a QIP. During such difficult times, they have no consideration for shareholder value, whereas there was no indication of a QIP earlier.

3 Likes

Diluting at this low price is big blow for retail shareholders. They claim that they have good cash flow from flex office business and it can fund other vertical growth, but now will raise fund by diluting at this price. This is another blow to shareholders after the last merger by allocating huge equity to promoters.

3 Likes

No idea what they are thinking here honestly. Can rationalise a lot of things but diluting at 52 week lows is nonsensical. I understand that price has not been decided yet, but I don’t want a company that always raises cash!

2 Likes

for a company wanting to grow 50-60% but with 20-25% roce how do u propose for them to grow if not raise funds?

1 Like

Do a rights issue and let retail investors as well as the promoters participate. I am sure Sageone is participating in this QIP as I saw a recent interview by Sameer talking about undervaluation in this space. Sageone is also invested in TCC Concepts and in Pepperfry aside from TCC.

These dealings are somehow giving me an uneasy feeling about Sageone and its relationship with the promoters.

Which recent interview you are talking about? Please share the link. Apart from EFC and TCC, Sageone also invested in Synthiko Foils Ltd share price | About Synthiko Foils | Key Insights - Screener where Umesh Sahay is a promoter.