Hi guys,

Here is my attempt to explain the corporate structure of EFC (I)

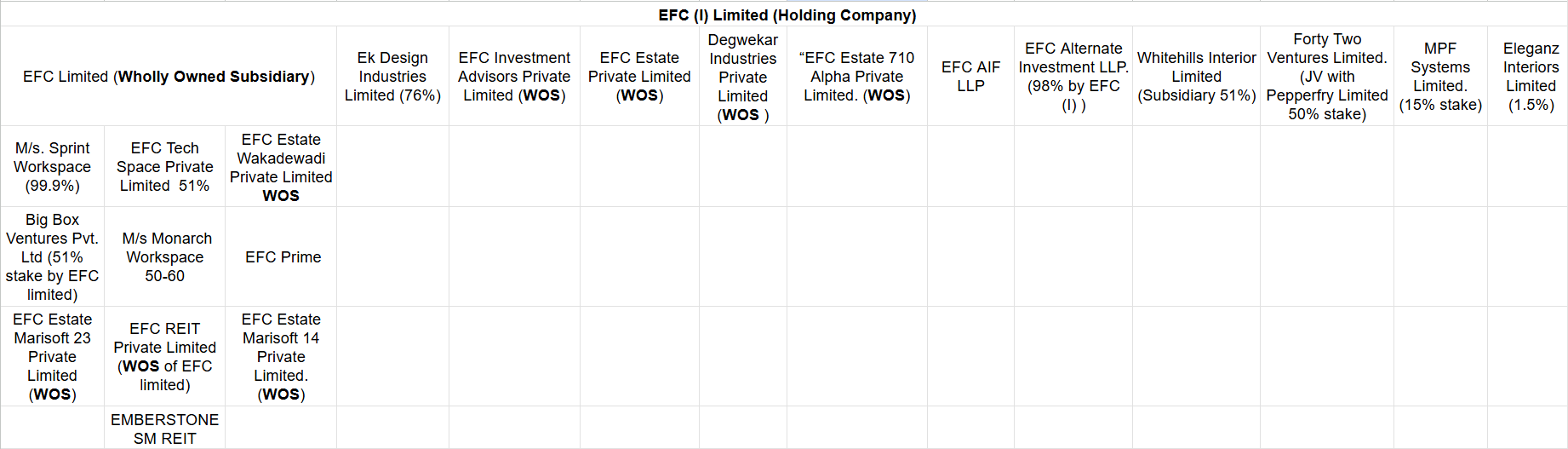

- Amani trading and exports was a listed entity, so the promoter took a majority stake here and changed the name to EFC (I) Ltd. Since majority business was under EFC Limited they were made a WOS of EFC (I) ltd. Hence we understand these two entities.

Understanding structure of a large REIT

- Trustee of a REIT is an independent party who oversees the REIT. Sponsor of the REIT is responsible for setting up the REIT and initially holding at least 15% of the total REIT units (locked in for 3 years). Manager of the REIT manages the operations (it is generally a WOS of the company). So EFC REIT Private Limited is the manager. Then you need a REIT whose units would be sold EMBERSTONE SM REIT (Please note these 2 entity are for SM REIT and not large REIT I was just drawing parallels for the need of these 2 companies)

- In case of large REIT the total size in terms of asset value should be exceeding 500cr, so I need to have property worth more than 500 cr

- The SPV hold and develop properties, now in case of large REIT 80% of the SPV should be income generating meaning only 20% can be used for development, the rest should already be an existing income generating property. (you can have a holdco in between REIT and SPV optionality)

- It makes lot of sense to keep each property in a different SPV because

a) If one building under an SPV faces litigation, debt default, or environmental issues, other buildings under separate SPVs remain unaffected

b) You books of account for each SPV becomes separate, it becomes more transparent, easy to raise debt or funding against that particular asset

c) Allows for better TAX structuring

d) In future if you want to sell that asset it becomes easier to just sell shareholding of the company which holds that asset

-

Hence for EFC it makes complete sense to purchase the income generating asset the manage from their landlord, create multiple WOS (SPV) and transfer these asset from parent company books to these WOS and start creating a portfolio of these assets to prepare for Large REIT where you need assets more than 1000 cr

-

Hence most of their subsidaries are named after the name of the assets. Let’s summarise and discuss all the subsidiaries covered till now

-

EFC (I) - holdco

-

EFC limited - Was the primary business which was made a WOS of EFC (I) ( Amani trading and exports) to get the business listed

-

EFC REIT Private Limited - Manager of the REIT (this is from SM REIT)

-

EMBERSTONE SM REIT - The SM REIT

-

EFC Estate Marisoft 14 Private Limited - (SPV)

-

EFC Estate Wakadewadi Private Limited - (SPV)

-

EFC Estate Marisoft 23 Private Limited - (SPV)

-

EFC Estate 710 Alpha Private Limited - (SPV)

-

EFC Estate Private Limited - (SPV)

-

Since RPT is allowed in large REIT it makes a lot of sense for EFC to acquire these assets in their books and bring them into the REIT. In this process if the company can acquire these assets at a cheaper price and sell it to the REIT at market value at arms length giving them their desired IRR, the company can earn a huge amount of profits. Please note that this is something which even embassy does. Build & develop properties in their real estate arm then sell to embassy reit at arms length pricing.

even a 10-15% discount on a 500cr asset would be 50-75cr of PBT.

- Going forward there might be a possibility of them creating more of such SPV. Creating a REIT structure allows them to eliminate landlords from properties, reduce the terminal value risk, improve the anti fragility of the business and make EFC asset light.

Under SM REIT

- SInce RPT is not allowed here I first get the IPO, raise funds and then acquire properties directly under the REIT. Also the properties need not be income generating here unlike the large REIT.

Conclusion - Instead of buying assets in EFC books, I create a SPV buy asset there so at the time of selling I am selling the company not the asset and the existing asset would be demerged into to SPV for ease of selling

I had also met the management of DevX where they had done something similar in an AIF structure, they created an SPV, had assets under that SPV, sold stake and now their yield would flow to the investors. once they list it would be easier to understand EFC

Other Subsidiaries

- EFC Tech Space Private Limited

Incorporated 9yrs back so not some new subsidiary.

- Signing a new building requires deposit to the landlord and a lot of investments into D&B. Since it is capital intensive in nature, back then when the scale of the company was small such partnerships were done with third parties who could provide capital and EFC would be managing the asset.

- Once the period of contract ends and the third party wishes to take an exit that is where EFC limited can make them their WOS.

Sprint workspace was a partnership firm earlier and in 2023 it became a WOS of EFC limited

So such partnerships or JV or any kind of corporate structuring under EFC limited, deal by deal or asset by asset might have been structured with various entrepreneurs to grow. All these companies were incorporated or registered before they did the fund raise in 2023. Hence these various subsidiaries were created and with time there might be a possibility that most of them become a WOS of EFC limited like Sprint workspace became.

Under this we have

- M/s Monarch Workspace - (partnership firm)

- M/s. Sprint Workspace - (partnership firm)

- EFC Tech Space Private Limited - (Pvt Ltd)

- EFC prime - (Partnership firm)

Under real estate, such formation of various subsidiaries property by property or asset by asset is pretty common and done by various players to have different kinds of financial arrangement for each asset and not mix them which increases your financial and legal complications.

At the time of exiting or selling your asset it becomes very easy in case separate financials are maintained. This is among the most transparent ways a real estate player can operate

Big Box Ventures Pvt. Ltd

During FY 25 EFC limited acquired 51% stake here with a cost of acquisition of 5cr while the company did a revenue of 4cr in FY23 with a potential of 14cr with a 3000 seat portfolio. The P/S of this acquisition comes around 0.35 when various private deals and public market securities are trading between 2- 4 times P/S.

Here are the financials of Big box for you to have a look -

Copy of financial statements_2022-23.pdf (2.7 MB)

Ek Design Industries Limited

EFC (I) holds around 76% stake here with balance with PRAJWAL DEGWEKAR (my guess) he is one of the director at EK designs

Ek designs was setup up for furniture manufacturing where later on it acquired Degwekar Industries Private Limited which was owned by Prajwal Degwekar

Here is the profile of prajwal - https://www.linkedin.com/in/prajwal-degwekar-2297b4110/?originalSubdomain=in

He has been into furniture manufacturing for the last 9yrs

I am sure by now it would be clear having the core business of office space helps him venture into various other businesses in relation with the core business. Where a structure of JV or acquisition is done by bringing capable people who align with the company and provide them the leverage of core business.

Like they scaled the D&B almost 50x now in less than 2yrs

This helps you venture into new vertices providing integration, where alignment of interest is there with the third party where they run the business and you provide the leverage

I am sure EK design would be the second proof of the pudding on the way of working of the promoter on such partnerships

One funny thing which happened was Degwekar was a WOS of ek design but now is a WOS of EFC (I) I am sure Degwekar might have been of no use to ek design since the entire business is happening in Ek design hence EFC (I) might have though to make it a WOS for it Large REIT. Internally recycle your companies instead of creating new subsidiary

EFC Investment Advisors Private Limited

As explained above for REIT similar structure has to be established for an AIF where EFC Investment Advisors Private Limited will manage the Assets and Investment of Alternate Investment Funds and EFC Alternate Investment LLP, EFC AIF LLP would be the Sponsor to the proposed Category II AIF

Whitehills Interior Limited

This is the D&B arm and there is a lot of concern around this on the merger valuation. I hope I was able to explain that in the previous post. Also under merger post the exchange and SEBI approval, shareholders approval has to be taken which is not yet done and the promoter as on date holds less than 50% stake so the merger cannot go through without shareholders approval

Forty Two Ventures Limited

This is a JV with Pepperfry Limited would be interesting to understand about this from the promoter in next call

For any company to sustain the rapid growth that EFC has demonstrated and to maintain scalability even at a substantial level, strategic partnerships, joint ventures, and corporate structuring are essential. These initiatives are not just for immediate expansion but for the future. While a large REIT may still be a long way off, the work for it has to start 2-3 yrs before than

Hence the corporate complexity is for the future. The cost of vertical integration & anti fragile business structure is increased corporate structure complexity to keep the financials transparent. Imagine if all these diverse but related business were in same company then investors would never know margins of any segment & transparency would be lacking.

Valuations and outlook

These projections have been made on the guidance available publically. FY26 target of 90k seats (in FY24 AR). Want to grow at 100% rate in the D&B division (have taken 50%) and furniture division at peak capacity can do 250-300cr (have taken 100 cr for next FY) on top of this how the pepperfy JV would add will have to check in the concall

All in all I am getting an asset light, integrated RAAS (real estate as a service) player growing at 50-60% available at 11-12 times FY26 earning

Dic - Invested