Hey folks,

Does anyone have either a non paywalled version or a summary/note on this article?

Hey folks,

Does anyone have either a non paywalled version or a summary/note on this article?

Please check if this helps - Edelweiss looks to list all firms and enter new business | Company Business News

Two suggestions:

let me know, if it helps. Thanks

Financial services firm Edelweiss to list seven companies in India, pare debt Edelweiss is planning to list seven businesses on Indias stock exchanges, eliminate all debt and start a new business venture, founder and chairman Rashesh Shah told the Mint. The plan will unbundle multiple entities and remove crossholdings, even as financial conglomerate remains under regulatory scrutiny over various violations highlighted in May. Why its important- The Reserve Bank has imposed restrictions on two Edelweiss group entities, including its asset reconstruction company, due to evergreening, circumventing rules and lack of corrective action. The group is now moving away from a holding company structure to an investment company.

decrease in promoter stake beneficial for business longevity, believes edelweiss rashesh shah. the promoter holding in the bse 200 companies came down to 38.8 percent in the march 2024 quarter from 42.1 percent in the december 2022 quarter.

PAT of 110 crore jump of 45% good jump in revenue . Management is strong on value unlock . This should be around 25-30k crore mcap

Value unlocking on cards:

Alternate Asset Subsidiary Files DRHP For OFS Of Rs 1,500 Cr Via IPO

Recently companies are going the IPO way to list subsidiaries. But this is no value unlocking to shareholders. Demergers are value unlocking. The only benefit, a shareholder gets is the advantage to apply for the IPO in shareholder category as well.

Very true … Demerger seems to be one of the best method of value unlocking for all class of shareholders be it promoters or public (in case of edelweiss same was proved was Nuvama was listed as a demerger process).

However, in case of proposed EAAA IPO:

Disc: Invested (approx. 7% of PF)

But once you list a subsidiary, won’t the parent co value reduce significantly due to that much part getting holding co discount? I still feel the stock price will reduce a lot close to IPO record date.

Current MCap of Edelweiss is approx. Rs. 12000 Cr which Mr. Market is giving for all the separate businesses it hold like NBFC, Housing Finance, AMC, EAAA, Life & General Insurance, ARC and holding in Nuvama.

Yes, for sure, once EAAA will be listed - holding company discount will get applied in valuation of Edelweiss.

But in that two primary question: (a) at what value EAAA is going to list, (b) what holdco discount Mr. Market will ask ![]()

If Edelweiss market value will correct, zoom or stay at current level … honestly I don’t have a public opinion on that.

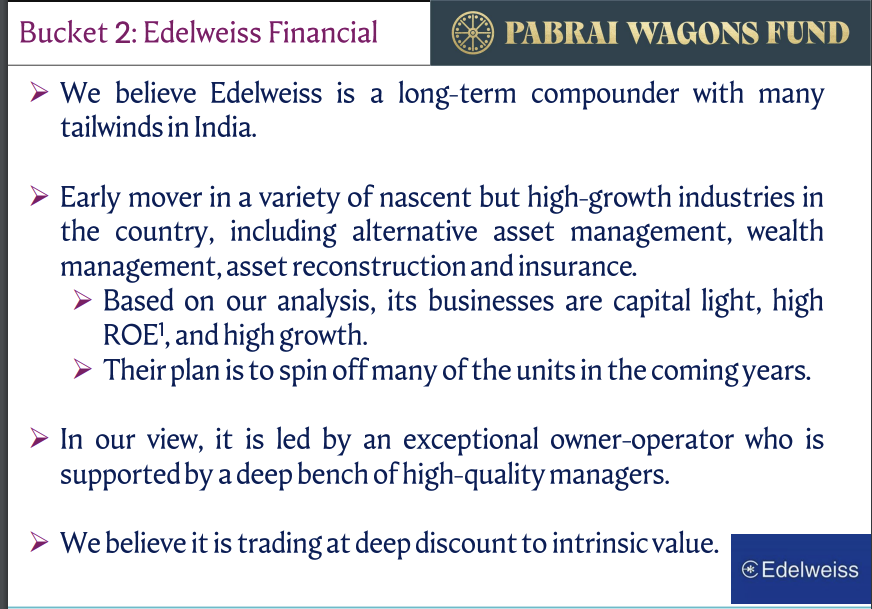

However, I see a value in current Mcap vs underlying business considering the expected listing/stake sale in various business, debt free at listed entity level, growth in individual underlying businesses; hence, holding strong the current portfolio position.

Thanks.

Copy of DRHP is now available at SEBI site for quick reference.

Industry-Research-Report-on-Alernatives-051224.pdf

Report by Care Edge (Subsidiary of Care Ratings).

For listed peer comparison, here they have compared EAAA with that of 360 one WAM.

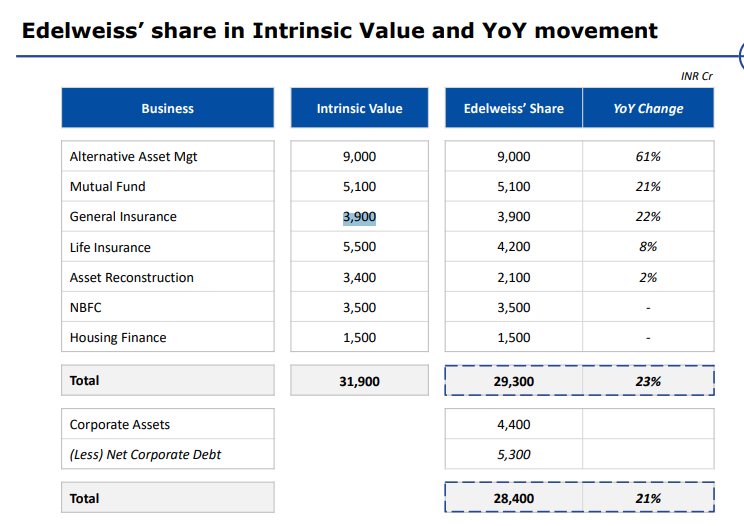

Also, intrinsic valuation being shared by management in last AGM are as following, please ensure self due-diligence, many a times Managements either over-communicate or mis-guide investors.

MF wants to sell 30-35% for around 1500-2000k for strategic partner to grow the business.

Edel want to reduce debt by less than from the current 5,000 cr to 1000 cr in the next 12 months

if AMC’s 30-35% is sold to strategic investor, wondering this will have the same path as that of Nuvama and not that of EAAA.

Good Report from Crisil

The funny part is what Crisil has mentioned is not mentioned anywhere in their quarterly report, no trace. Without this individual investor has not idea that 5300 cr of loan is not on Edelweiss book but they are responsible for it (indirectly as they sold the loans to ARC,AIF)

Furthermore, EAAA India Alternatives Ltd has filed its prospectus with the Securities and Exchange Board of India for an initial public offering (IPO) of up to Rs 1,500 crore, which is expected to be launched by June 2025

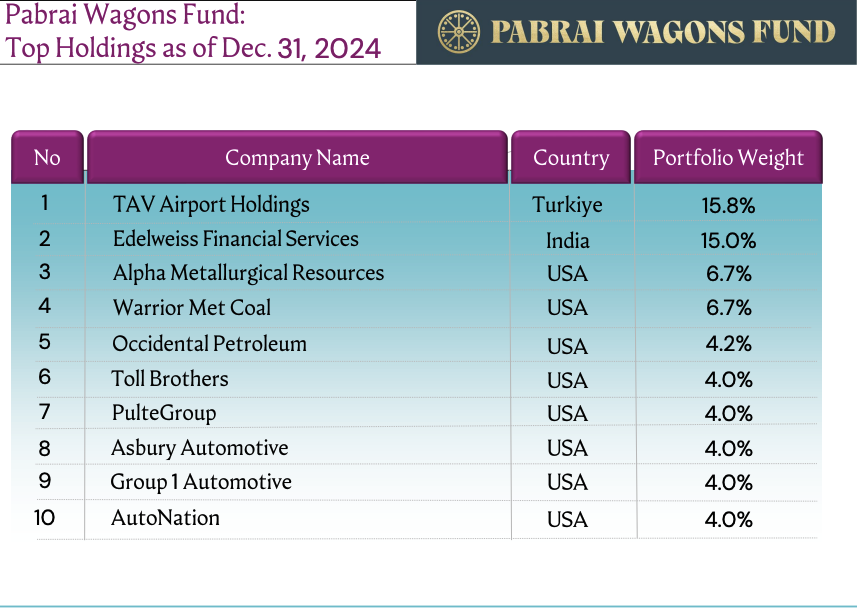

However overall holding of Pabrai has come down significantly in last few quarters as per screener data. Pabrai Wagons fund total assets is $54 mn, so 15% holding in edelweiss translates to 0.6% shareholding. Hope this fund grows in size in coming years!

If anyone could explain the demerger situation with the EAAA business. How it will unlock value for the shareholders? With Nuvama, the EFS shareholders got Nuvama shares. This time it’s OFS, should we keep cash handy to purchase EAAA shares or buy more of Edelweiss shares to benefit?