A detailed article by PA wealth advisors :

3 Likes

What’s happening with this scrip? It is falling 10 % every day now, yet no news anywhere. Does anybody have a clue on this?

1 Like

In wealth Insight mag of this month, there is a mention of “The enforcement Directorate is investigating an investment of Rs 450 cr made by a subsidiary of the company”. Apart from it I can’t see any news.

Disclosure: Sitting at a loss of 70%. I should have exited earlier however loss aversion failed me in this script.

IIC Presentation - June 2019.pdf (757.7 KB)

3 Likes

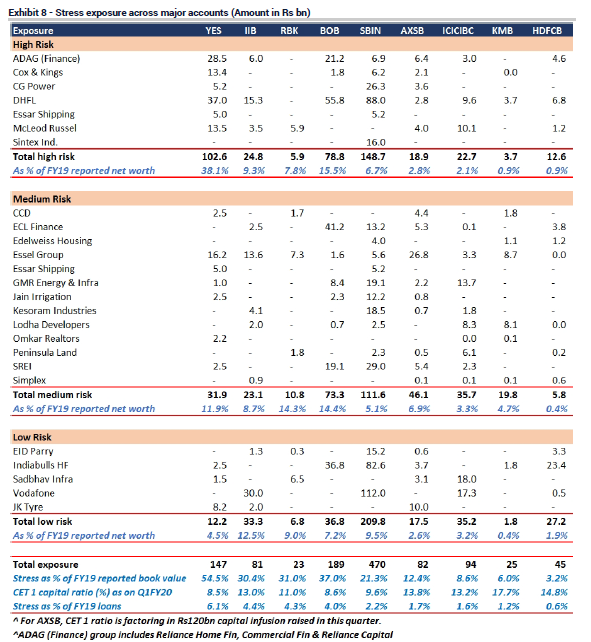

Edelweiss Financial has exposure to Kohinoor, a real estate company which has defaulted on payments.

Management Clarification on this -

“The current probes by IL&FS on Kohinoor transactions are for the period of 2005-12 and related to transactions entered into by IL&FS and certain parties. Edelweiss group had no exposure to Kohinoor during that period,” Edelweiss Financial Services said in a regulatory filing.

I have seen this message circulating in social media.

It includes Edelweiss as stressed asset to Banks.

How true is this.

Don’t know when Edel Housing or ECL finance became stressed? They have 9-12 months of gun powder in the form of cash so where is the default risk? Real estate industry is in trouble but it doesn’t mean that all projects are stuck. In the last concall he clearly mentioned that 33% of all financed projects will be achieving OC this financial year and another one third within 18-24 months. They do have issues in few projects and they do have plan for the rest too. During Q1 they have shared outline that they would reduce wholesale exposure by 3-4k cr of total 15k cr. Now the key question is how. There are three routes - 1) Securitisation with banks and other financial institutions. 2) NPA sell down to their own ARC - this has already happened in the past. This way they keep all the gains inhouse post resolution. 3) Sell down to their own RE/AIF funds in due course. They have raised multi billion funds in ARC/AIF. Now the key question is why would these funds buy assets from NBFC. There are two reasons a) They have recovered full amount in the past so the track record is good b) Edel has skin in the game even if they sell it to fund structure where it is the most suitable.

They were the first one to identify the issue and communicated about applying break on lending engine. Let’s not forget that their capital market subsidiaries will start growing from Q2/Q3 onwards as market revives. It is really shocking to see at 1x P/B but should not be a big surprise given that it was a bull market favourite.

Disc: Remain invested

2 Likes

Their office is also at Kohinoor kurla property …one employee told me 6 months back that they got it as part of recovery

The reason why the stock is falling so much is because the market for not have clarity as to how much money is really at risk. And it being a small cap is likely to be punished severely.

the NPA figure might be too ugly to disclose.

That is plain speculation. If you trust Rashesh Shah, you would find enough hints in his latest interviews that RE industry has not slowed down incrementally over the last few months. Execution has slowed down a bit. It is not great but that is the case for the last 8 yrs or so.

With due respect to Mr Shah, it is difficult to rely solely on what the management says. As an owner of the leverage financial institution, they will never say that their company is in trouble. On the contrary sounding optimistic most of the time.

There are many cases in recent history (in last 12 months) where promoters were not openly acknowledging the true extent of the problem(Yes, ADAG, DHFL to name few). However, the market was smart to give enough hint.

I am not sure that is the case here because Mr Rasesh Shah has a much cleaner reputation than the above-mentioned name.

Leverage financial institution is a tough business to be in. They can do 1000 things right, but one big mistake can wipe them out entirely like PMC bank.

5 Likes

You have to traingulate with what was his communication during good times. He never gave too rosy outlook even when PAT was growing 35-40%. My only contention is that market has overdone it. Their RE lending is 25% of the book and NBFC itself is 50% of the total biz. Even if we give zero valuation to their lending biz it will be slightly undervalued at cmp. Their leverage at ~3.5-4x is among the lowest in the industry. Wiping out entire equity is unlikely given the diversified nature of the organisation.

3 Likes

A couple of insights into Edel management. The pics are from Jana Vembu’s blog; the original document is from Jan. 2017.

4 Likes

4 Likes

Few tidbits from the above interview.

NBFC exposure to real estate - 11,0000 cr/ Balance sheet 55,000 cr (20% of the bank)

No of project - 160.

Overall 30/35 are always under watch.

10-20% always under watch. Those parameter has not gone worse in the last 12 months.

If the project gets completed, the NPA get contained.

Mr Shah sees a huge flow of liquidity from global funds into the credit market in the next six months as they would be earning a return to the tune of 13-15% per annum.

4 Likes

Some thoughts:

The biggest NBFC / HFC in India was a monoline for an inordinate period of time, over multiple cycles: HDFC. Its management still operates it as a monoline and the rest are investments

Gruh Finance, a very commendably run HFC until recently was not only a monoline but in a segment within the monoline.

So are many NBFCs firms down south like STFC / SCUF / Muthoot. Chola / Sundaram Finance are largely monolines. Many struggle across cycles as do all businesses.

![]()

Yes! Sundaram Finance has reduced its book size, if pricing is irrational, in fact it has stated so often. Chola burn’t a bit in the 2008 boom in unsecured lending with erstwhile DBS JV, but scaled it down in an orderly fashion.

![]()

Lending is a risk business that grows not a growth business at any risk! Like someone said, “this is not a business of lending but a business of collection”. Credit company should be OK with a shrinking book if there is no risk-adjusted credit to be underwritten.

13 Likes