Last 8-10 days have been a tough and testing time for Edelweiss investors. Share price has fallen by more than 25% in a short span of time.

IMO, apart from the general market conditions, two specific news have put the stock further in red namely

-

To sell a nearly 17% stake in Advisory business valuing this business at only 10-12 times 2 years forward PAT is indicative of how tough it is for the Company to raise finance and keep liquidity

-

Listing of advisory business - Edelweiss Financial Services Limited will be a holding company reducing the market perception of EFSL to that of a Holding Company

The credit business too is finally showing slippages and management has guided for more credit costs in Q2.

Only silver lining has been management has been upfront and conservative in leverage in credit business and keeping sufficient liquidity. (Except for reversal of growth guidance by management which is also a function of market events not fully in managements control)

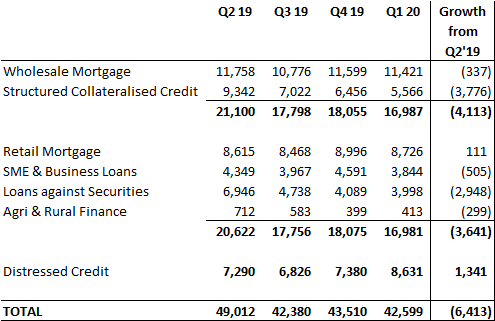

For instance management had guided that wholesale lending will be slowly moving off books to Funds, I have tried to corroborate with data

Clearly, Structured Credit has significantly reduced. Management in Q2 presentation has guided for another 3,000- 4,000 crore reduction in Wholesale book. If this is achieved with GNPA of less than 3% then it will be quite an achievement. It would mean developers are repaying from project cash flows as chances of refinancing look bleak - again this is dependent on markets.

It would also mean that overall wholesale book would be nearly half of Q2’19 levels - again quite an achievement if 50% of Risky book is recovered in ~ 18 months.

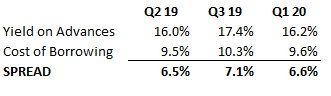

Another point is that as per management cost of borrowing has come down in last 6 months and spreads have been maintained.

Im not sure of how cost of borrowing is calculated since cost of holding liquid treasury assets is booked under separate vertical viz - BMU

Next 6 months would be crucial for the credit business, and if the guidance is achieved, then there is a good chance of change in risk perception of loan book and consequent re-rating.

Also management should clarify on what would be the legal structure of the business post listing of Advisory business. If management cares about its long term perception and interest of minority shareholders of Edelweiss Financial Services - they should be given shares in the advisory business instead of shares being owned by the Holding Company. Such a clarification would again go a long way in dispelling fears and reversal of the de-rating of the stock.

Disc - after last post, sold another 1/3rd of holding in loss at ~ 122.