Transcript of one more update by Mr Rashesh Shah of the Market conditions for NBFCs

2 Likes

There was a good insight by the promoter of MAS Financial on the current state of crisis looming on NBFCs in the market. Thought to share it here too !

"In the events of Crisis , everyone becomes Irrational and start painting everyone with same Brush. Approach towards individual Companies should be discreet. In good times , not every company is good and in bad times , not every company is bad.

MAS has experienced 1995 Crisis , 2002 Earthquakes , 2008 financial crisis and 2013 liquidity crisis. Companies with sound Fundamentals will navigate through these times and will grow and create good assets.

For India to grow at 7% of GDP , NBFCs are the backbone. NBFCs remains the most important last mile delivery of credit . There is no slowdown from the end user demand and these are temporary times which will pass soon.

8 Likes

I just did back-of-the-envelope check to see what market is implying within current price of Edelweiss.

Edelweiss Value = Current Book + Earnings Power

Current Book Value = 7500cr as per latest Sep '18 balance-sheet. I take ~15% haircut to it and I get 6400cr as current book value.

Earnings Power = 900/0.10 = 9000cr (explanation to earnings power calculation - assume that 900cr of FY18 earnings will continue as annuity yield with no growth in future. 10% as after-tax discount rate which means 11.75% before-tax discount rate which comes close to Edelweiss’ today’s corporate bond yield. If I had used pre-tax earnings in numerator, I would have taken 11.75% as discount rate).

So I get Edelweiss Value = 6400cr + 9000cr = 15400cr which is close to current market cap of 15625cr.

IMHO one is not paying for any growth at current market price and eventually getting a well diversified financial services business in an economy which has potential to grow approx 5x in next 20 years (GDP of $2.5T to $12.5T).

IMHO market has literally taken Mr. Rashesh Shah’s statement of future slower growth as “forever no growth”  . And just 2 months back market was implying forever 20% kind of earnings growth. This proves market’s exuberance on both the sides!

. And just 2 months back market was implying forever 20% kind of earnings growth. This proves market’s exuberance on both the sides!

Disc: accumulating at current levels and hence views will be biased.

P.S.: I know a lot of folks will rip apart above back-of-the-envelope calculation. I am not here to argue on current book quality, or hair-cut %, or other appropriate discount rate. Just wanted to share my findings of what market is implying at current levels using conservative assumptions. If you have a better way to do back-of-the-envelope valuation of Edelweiss, would love to see it and learn from it.

12 Likes

Not sure about this, but is there an element of double counting in your calculations?

Doesn’t your Earnings Power include earnings from the current Book Value?

You can’t include both current Book Value and future Earnings Power, which is partly based on the same Book Value, can you?

As a test, assume all the debtors prepay Edelweiss with a 15% haircut (15% figure taken from your post), which the company distributes to the shareholders. Now how much will the company earn from new business in the long term? That, discounted to present value, can be the Earnings Power.

I may be wrong here, happy to be corrected.

5 Likes

Hi - you have double counted the income on nbfc business and hair cut on book value.

The way to look at it is approx.Rs.330 Cr. of Non-NBFC income which using your logic is worth Rs.3,300 Cr. (but this is a high growth business with fantastic return ratios so a 10x kinda working is unfair) further the NBFC business you are taking the hair cut of 15% but you are discounting the gain which would be accrued in ARC from resolution of Essar and Binani Cement

Hi @rupaniamit

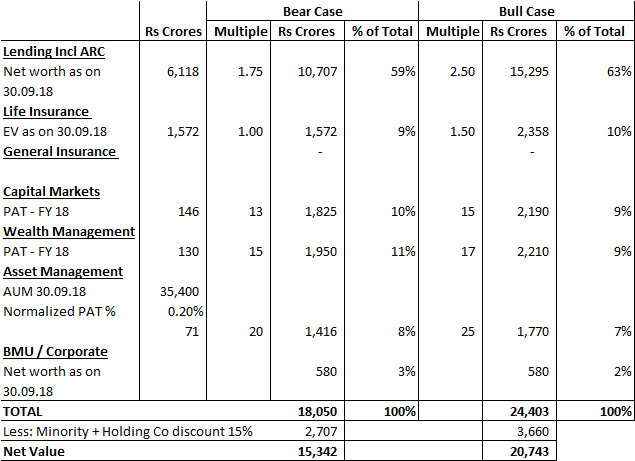

Sharing my rough cut valuation for comparison sake. Multiples considered are purely arbitrary based on my limited experience.

Sharing rationale for multiples

- Lending: I expect near term RoE to be in 15-17% range (it is ~18% for last 2 years) largely due to reduction in high yielding RE and Structured lending, increased cost of borrowing partly offset by improved realisations from ARC business. Long term Growth in BVPS would be in line with RoE. Hence, i feel 2.5 times is a fair P/B multiple. However depending on the risk perception on the lending book, this can be lower.

2.Life Insurance: I dont understand valuation of Life Insurance business very well, but if edelweiss were to sell their entire stake today to another party, i feel they should fetch atleast the amount of EV. Once the business matures, they would get advantages of ecomonies of scale and underwriting and going forward if management doesnt make big mistakes, it can be valued at 2-3 times EV like peers.

-

Capital markets advisory - Taking low multiples since FY18 would be at a higher end of profits in a cyclical business.

-

Wealth management - Many headwinds, multiple in line with peers.

-

Asset management - Have taken normalized PAT on AUM since their AMC is still loss making. HDFC AMC earns 0.3-0.4% of AUM as PAT but that can change now with the SEBI cap. Edelweiss actually has a high share of higher yielding alternatives but unless the size of AUM goes up, cost efficiencies would not be there. That is why I have taken 0.20%.

Barring wealth management, I feel in each of their businesses, the sector can grow at 15% + in the long term. My bet is mainly on the Management to not make any blunders in the future and atleast grow in line with the peer set.

I am hardly an expert on valuation and more of a ‘feel’ guy when it comes to assessing businesses. Hence pls pardon any mistakes in the above.

Disc - Invested and adding. Views may be biased

7 Likes

Not doing much calculations but I have been visiting edelweiss regularly as we are one of their supplier and I manage the customer ( edelweiss ) relationship from my organization.

To all whom I have been meeting and interacting are middle management staff there and all of them are very positive and bullish about their future potential and growth.

There is absolutely no negativity about anything happening to their share prices in market and all of them suggested me to accumulate/buy if I have holding period of midium term ( 3-4 years ).

Just sharing it in case .

Disc - I am invested in it and have bought it at 300, 220 , 170 , 135 levels and it forms 14 percent of my PF at yesterday’s closing price.

So my views can be biased.

2 Likes

Edelweiss’ stock is suffering from sector headwinds only. Series of interview by Rashesh Shah was taken wrongly by the market. In the last one to BloombergQuint he specifically mentioned that his view on the NBFC sector is different from what is happening in his own company. Folks forget that he is also FICCI chairman so he has responsibility to speak from the macro point of view.

Coming to the Edelweiss, it was clearly mentioned in the Q2 concall that they have 3-4k cr worth of bank lines available and daily CP data suggest that Edel is raising short term money at competitive rates. They have repetitively mentioned that they have good relations with more than 40+ banks as they keep buying NPAs from them. As far as I know they have access to the top decision makers in these banks for quite a few reasons. One is NPA and the other is Edel is the largest debt market arranger for many entities including banks. I never believed that they would face any liquidity issue but on their part they have been extra cautious in investor communications.

One more thing we need to keep in mind that they will have the largest ARC recovery so far in the coming 2 quarters. So all slowdown talk in Wealth Mgmt, AMC and Capital market will be compensated by ARC profits. Rashesh Shah mentioned that they will have 2.5-3k cr of cash inflows from Binani and Essar case resolutions but refrained from giving any profit guidance. I think FY19 is sorted for Edel and we need to start thinking about FY20. Hopefully capital market would revive by then or after election during Q1 FY20.

Disc: Among the large holdings

7 Likes

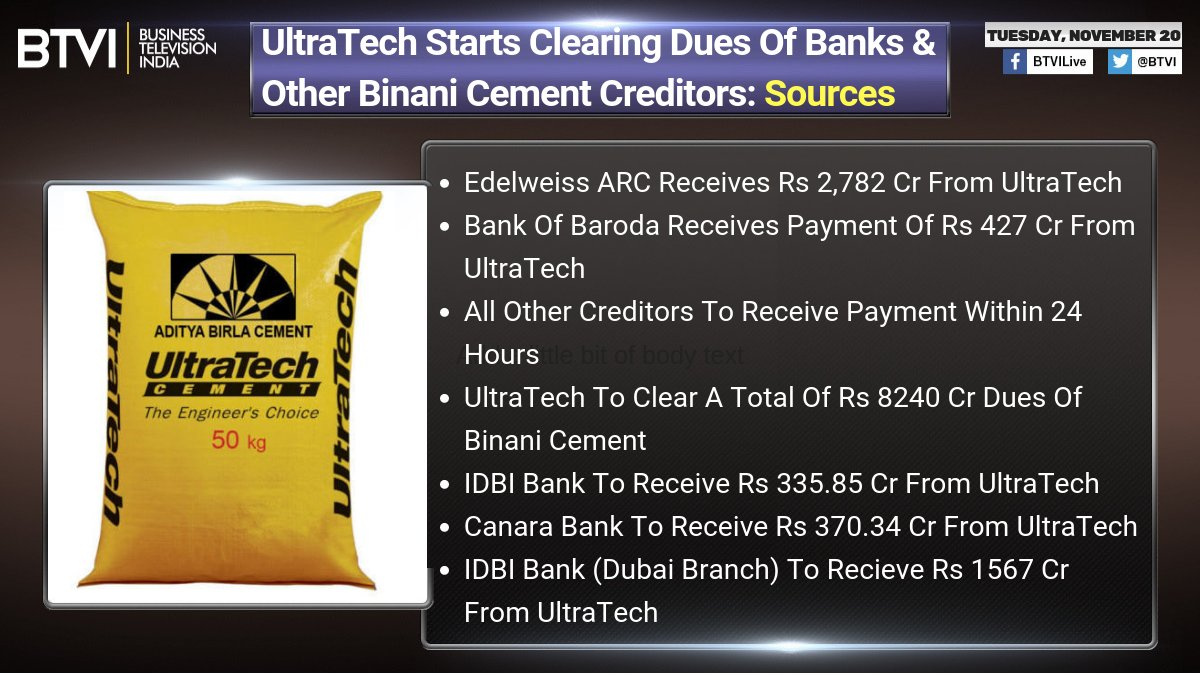

Binani deal is finally closed. Old estimate suggest they would make 500cr profits from this one deal. Good to receive 2800cr cash in these tough times.

11 Likes

Hi - Rs.2,800 Cr. of receipt does not mean Rs.2,800 Cr. of profit. ARCs basically buy debt from banks at a discount/hair cut - usually 25% to 50%. While buying this debt they pay upfront cash of 15% and issue Security Receipts for balance amount. When ARCs recover money they are supposed to redeem the Security Receipts.

ARCs profit if the discount/haircut at which they had bought the Debt is more than the eventual haircut the lenders have to take in the resolution deal.

So out of the Rs.2,800 Cr. of money that is coming back they have to still repay the lenders from which they had bought the Binami Debt and the profit would be the difference in the haircut and eventual discount.

(I would add more detailed workings but I don’t think the profit would be more than Rs.500 Cr. in this case)

1 Like

All said and done, I was expecting some effect on price y’day, after the Binani settlement but I guess, the usual cliche ''it is all in the price, already"applies here …I thought that 500 cr profit is phenomenal but again, it is all relative, I guess

In your second paragraph, I think you want to say that discount rec’d by ARC company is higher than the haircut settled with lender.

Having stated above, I think ARC business like scrap dealers is yet to be understood by retail investors in view of its complexity and not enough details being available in public space

1 Like

I think what matters is that folks are buying in deliveries or not and on that front no worries. I feel that the stock is being accumulated after a big fall and should consolidate given the amount of free float. If it keeps earning growth intact even during the downturn, will deserve a big upgrade and rerating in the market upturn.

2 Likes

Top Bad-Debt Buyer Edelweiss To Focus On Soured Consumer Loans: Report - NDTV https://www.ndtv.com/business/top-bad-debt-buyer-edelweiss-to-focus-on-soured-consumer-loans-report-1956869

1 Like

4 Likes

“As reported by The Economic Times, the potential deal is likely to value the wealth and asset management business around Rs 12,000-15,000 crore. Edelweiss’ current market capitalization is around Rs 17,300 crore.”

If the Reporter is right, it seems as if the collective wisdom of the Market doesn’t assign

any meaningful value to Edelweiss’s other businesses!

5 Likes

Edelweiss Group NBFC arm ECL Finance Ltd. to launch Rs. 10,000 million Public Issue of Secured Redeemable Non-Convertible Debentures (NCDs) on 13 December 2018

Effective Yield of up to 10.64% per annum*

Ratings - “CRISIL AA/Stable” and “[ICRA] AA (Stable)” - indicate high degree of safety regarding

timely servicing of financial obligations

Minimum application size Rs. 10,000 collectively across all Options ranging from 39 months to

120 months

Allotment on first-come, first-served basis

No TDS applicable for NCDs held in dematerialized form

1 Like

An independent director sold his entire holding in Edelweiss. This information hasn’t been provided by company to stock exchange and is instead captured from the demat account of insider.

1 Like

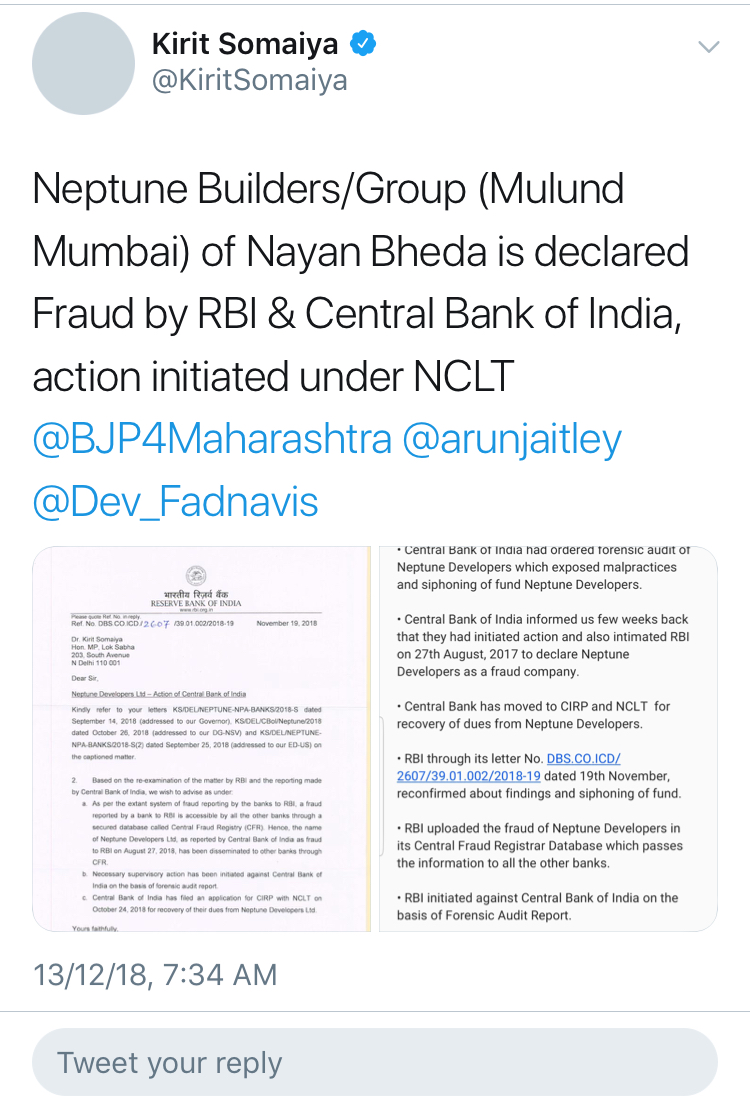

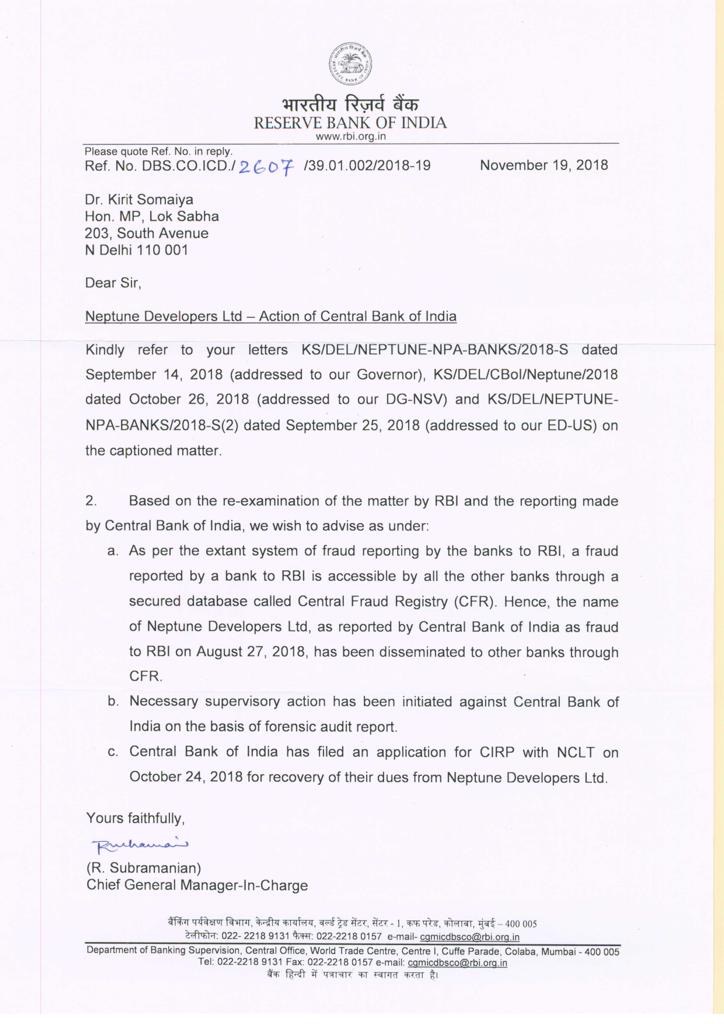

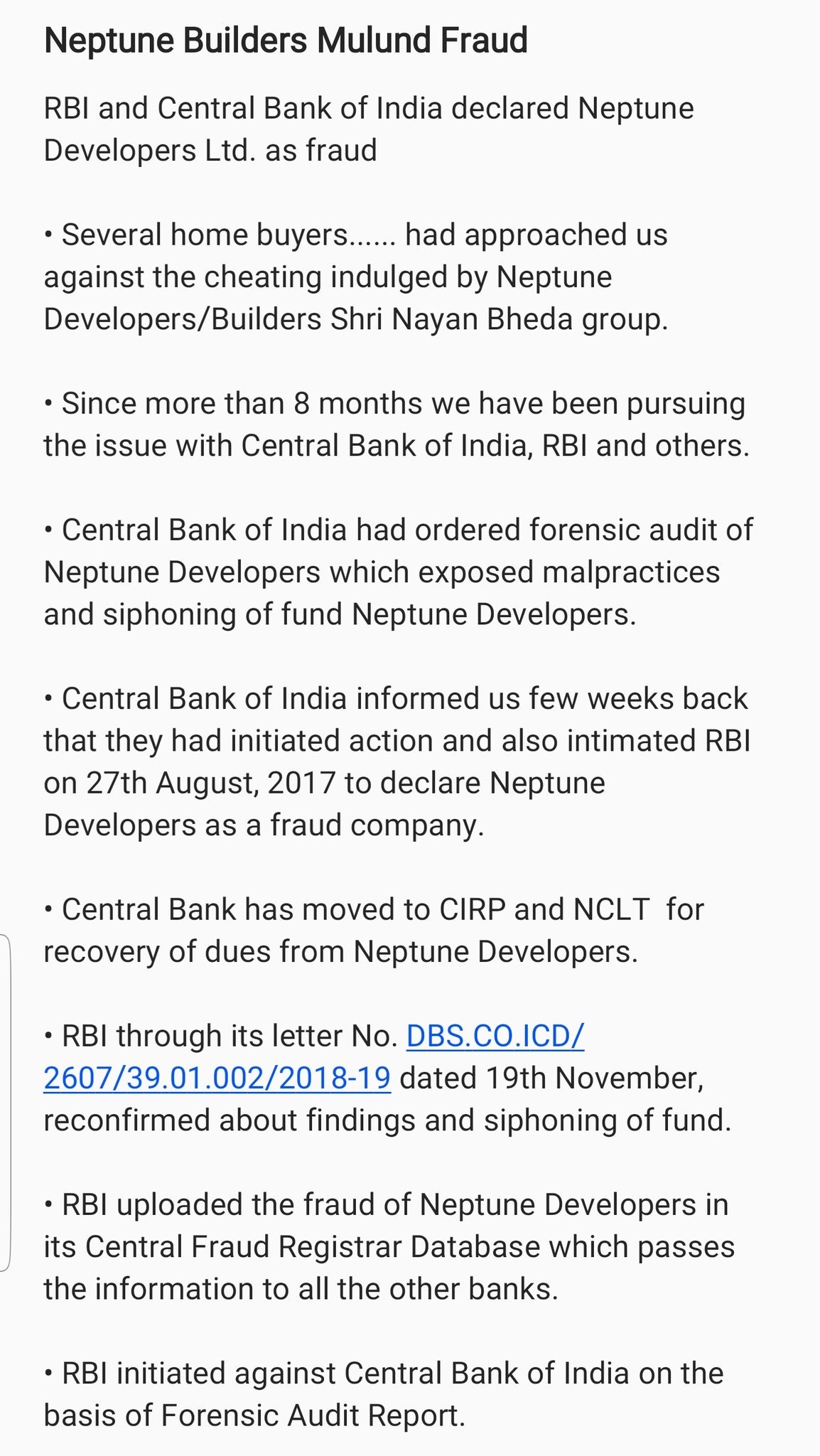

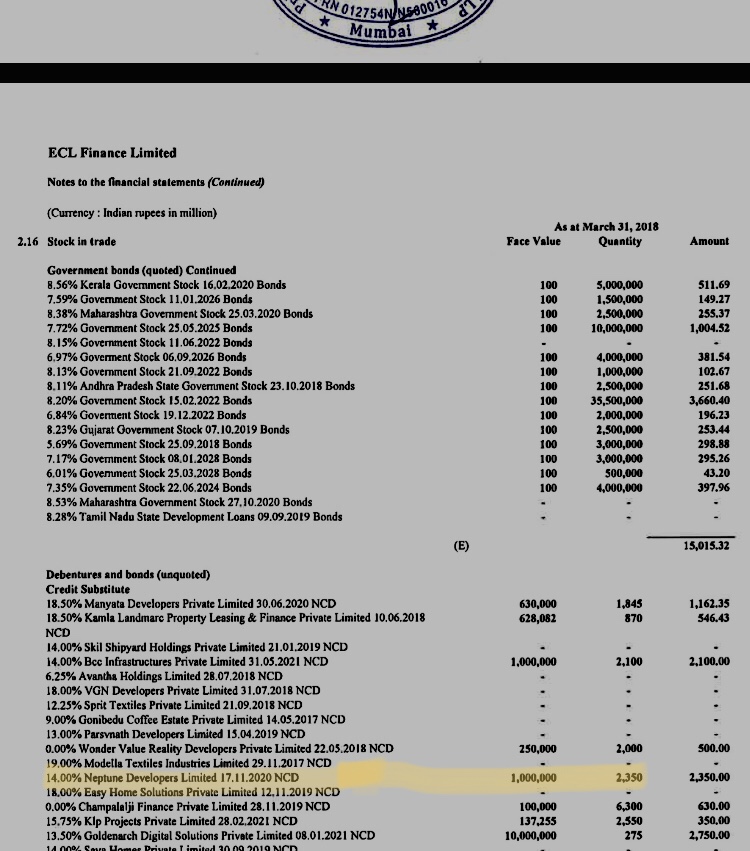

ECL Finance’s Stock in Trade schedule as on March 2018 showed an Investment of Rs 235 Cr in NCDs of Neptune maturing in Nov 2020.

Neptune’s register of charges shows a charge of Rs 235 Cr against Receivables and Escrow Account in the name of IDBI Trusteeship Services Limited.

Additionally, there is a charge by ECL Finance of Rs 145 Cr against uncalled share capital, immovable property and some movable assets plus escrow.

10 Likes