Very detailed and more importantly FAIR presentations by Edelweiss on Q2 overview and path ahead for H2 FY19.

Key takeaways on the lending business (comments in brackets)

- “We are in an environment where liability management models are being tested. Liquidity is returning to the system steadily and slowly. We have raised ~ INR 2,600 Cr since September 21st, including INR 1,450 Cr in CPs. We have bought back around INR 1,000 Cr in CPs”

(Re: liquidity returning - as per various info, rate of CP issues is going up https://twitter.com/deepakshenoy/status/1055798219291090944. However, As funds are expected to get costlier, hence chucking out costlier source of fund seems to be a margin protecting move, which is welcome)

-

"We have been here before in 2008 and also in 2013. This is a passing phase; we expect normalcy to return in next few months.We expect to see a return to the growth path in FY20.

-

We expect the corporate credit book on our balance sheet to reduce while simultaneously investing in such opportunities through our funds in Asset Management"

(In a recent interview on a TV channel, Mr Rashesh Shah mentioned that NBFC’s growth would moderate to ~15%. Looks like management is prepared for even zero or marginally negative growth in Loan book in next few quarters. Again, not too concerning as markets seem to have already priced this. But nice to hear the management being up front and fair about this)

- “We will continue to grow our SME and small ticket housing loans in a focused manner. Our customer understanding and product suite in these segments enable us to have pricing power and hence protect NIMs”.

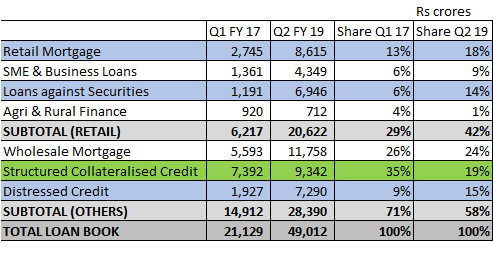

(To be fair, the management has walked the talk in the past on the aspect of increasing Retail as a % of Total book.Against the self set target of 50% of Retail by 2020, it has already reached 42%.

Further Management has significantly reduced proportion of risky Structured Lending with increase in proportion of relatively less risky Retail Mortgages and LAS in the last 2.25 years, refer tabulation below

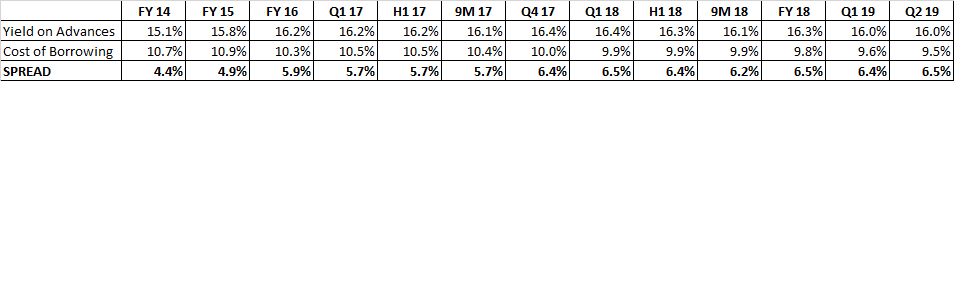

However, the concern here is that to achieve the target blended yield of 16%, if the high yielding Corporate Book is to be replaced with SME loans - there would either be a reduction in spread or an equally risky SME loan book as a consequence. This I feel is an inherent problem of an NBFC which borrows at 9.5-10.5%. A lot of these SME loans would have to be unsecured. As per management their unsecured SME loans have an average yield of 21% and average ticket size of Rs 10 lacs. Another factor is what would be the demand for these loans, especially in times of rising interest rates and the competition. I think it would be reasonable to expect a contraction in spreads of Edelweiss, relative to banks. Refer tabulation for spread analysis of Edelweiss QoQ

IIFL, which has a more retail oriented Loan book had an Yield of 14.5% as on 30.06.18.

-

Long term borrowing as a % of Total borrowings has gone up from 34% in FY 15 to 59%. (Aggressive long term borrowing when interest rates were lower, will certainly help spreads in short - medium term)

-

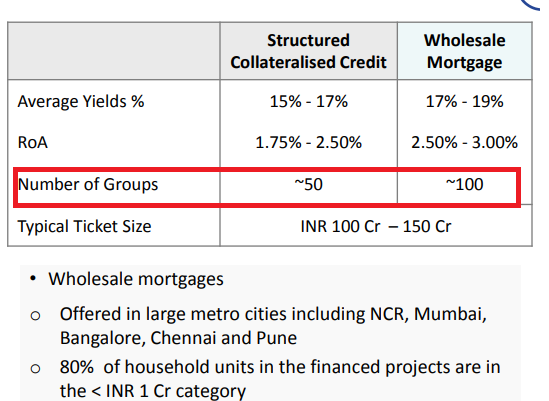

Management has disclosed ~ No of groups in Wholesale Loan Book.

-

“Wholesale Mortgage market is ~INR 5 Lac Crore”

-

“Edelweiss Wholesale Mortgage book size is ~INR 12,000 Cr (~2.4% market share)”

-

“All lending post land acquisition and key approvals”

-

“Sole lender status gives exclusive control - 95% of Total”

-

“Well collateralized at ~1.9x cover; Exclusive charge on the collateral and cashflow control”

-

“Strong legal documentation with step-in rights - eight Asset Resolutions done through a mix of stepping in, bringing in new developer and end customer sales through captive distribution team”

(I feel the management is telling us that they have most of the controllable risks under control. For eg: a builder having approvals will largely eliminate the risk of unfavourable political, environmental events which will jeopardize the project; sole lender and escrow mechanism will largely ensure crony promoters dont divert inflows of projects; management capability to ‘resolve’ potential deadlocks by bringing new developers, end customer sales etc.

The inherently non-controllable risks like slowdown in demand cannot be addressed by any lender.

I feel Edelweiss’s RE lending book is more seasoned and less risky vs someone like a Piramal which gets into pre-approval lending and loans for land acquisition.

However, having ~50 groups in a Structured Loan book of Rs. 9000+ crores and ~ 100 groups in a Wholesale book of Rs. 11,000+ crore is something that Im not very comfortable with. Even One or two groups turning Non-Performing would cause a significant spike in NPA %.)

Overall, it is very comforting to see the management attitude in being upfront and sharing such information. If one is able to read between the lines, there is plenty to digest  This is a welcome change from the lop-sided investor presentations released by some peers.

This is a welcome change from the lop-sided investor presentations released by some peers.

The risks of contraction in margins, slowdown in growth and asset quality continue to loom over the horizon, but management performance (and perception) has been equal to the challenges faced in the recent past.

I continue to hold and add on dips. Views invited