Is this promoter selling a part of buyback? Or is it in addition to buyback?

eClerx has witnessed USD revenue stagnation (+0.1% 12-qtr-CQGR) coupled with a structural swing in operating model (shift to onshore) resulting in EBIT margin plummet from 33.5% to 13.8% in the past 12 qtrs. We reckon that the shift to onshore will continue given the on-site heavy digital projects coupled with low demand for traditional KPO services.We remain cautious on high concentration and stagnation of T-10 accounts, shorter duration projects providing limited visibility and lower quality of revenue mix.

Is It safe to assume that Eclerx’s business model is “Disrupted” ?

@jamit05 These are trades reported on account of tender offer of buyback during June 2019. All the shareholders were eligible for buyback and everyone tendered at 1500 per share happily.

2 Likes

Eclerx was a major holding few years back because of Good execution by management due to domain expertise in financial back office processes that offers it competitive advantageleading to healthy margins. However due to fundamental shifts in the sector and in continued underperformance it seemed that in the long term the business would be hurt by disruption due to automation etc. This is still a watchout.

However current valuation levels seems to make it an attractive bet as the market seems to value it almost little above its cash (2000 crores market cap vs. 1000 crores of Cash + investment) as a firm which seems to be going out of business. Company is still growing through margins are shrinking and 10 PE seems like a good value to enter. Looking deeper into the company few other factors seems to be favorable indicating a possible revival in growth.

- Company is still at zero debt. It has reduced its dividends considerably and using it to invest in business - this is a good sign showing that company wants to fight the unfavorable markets conditions and turn around the growth trajectory

- These investments seem to be in the right areas based on my experience of the KPO sector - 1) in building onsite team for some of its financial clients - this is becoming critical with the need to be closer to clients and extreme difficulty global delivery models are in due to visa laws 2) acquisition (2 4 consulting) to further build domain expertise 3) research and innovation in automation and machine learning - again this tends to be cosmetic to build valuations but in this case based on my experience in analytics industry the areas company have invested in (scraping, process automation, etc.) seems to be tactical and something with tangible ROI

- Company is also diversified and not solely dependent on one sector - business into digital marketing (content creation, management for ecommerce etc.) should provide diversification of revenue sources though need to watch what expertise(domain/process) is being built in this sector

Overall the valuations are a good entry point and position can be further built when company starts to deliver on this investments.

Some more notes based on the Q1 earnings call

Further negative news with bad Q120 results with margins further depleting and Sell rating from HDFCsec. Stock is at 9 PE and account for Investments and cash only at 4PE which should be a definite buy. MArket is completely writing off any growth in the business. Theinvestment thesis around eclrex is that with the onsite investment and focus on automation this is now a different business model at lower profitability. As long as there is growth at this price level can increase weightage to 7-8 % and possibly even 10% as a big bet in the sector. PE rerating may take some time and few quarters of growth given broader and specific negative sentiment. The legacy contracts (>5 years) are more at threat vs. Automation. With time as % of legacy work decreases performance should increase. Decreased legacy work which was more optimized also leads t lower staff utlization as more capacity building is required in newer areas initially. High attrition also leads higher bench requirements. Overall this strengthens the thinking that this is a different business models and competence of management to adjust to the new demands will determine growth. Business also shifting to project based vs. annuity . 1/4th of revenues is onsite“Our business is in midst of a deliberate transformation that has needed and will continue to need investments from us. From being an all-India delivery Knowledge Process Outsourcer reliant on a handful of clients and service lines, we are changing to become a more technology-centric process management and data analytics company. . We service today several hundred clients across many functions,from locations across the world,with a fantastic,global management team. We are aware that this transformation has meant lower profitability and growth in recent past than shareholders have been otherwise accustomed to, but we believe this transformation to be key to our long-term future and to shareholder returns”

Overall while the earlier business has been disrupted management has been responsive with changing scenario and current bet would be on management making it work.

Disclosure: invested

1 Like

I would agree with some of your observations, about change in business model from pure KPO towards automation + data analytics + KPO.

Many large IT organizations have also invested heavily into Data analytics, AI, Chat bot, Machine learning, and Robotic Process Automation and have demonstrated growth of over 25% in digital revenues, over past 2-3 years. The same model need to be replicated to some extent by eClerx, with their deep KPO knowledge. How much management archives this, is something which we need to watch.

It would take around 4-6 quarters, or less, to see if this onsite model is working or not. It is no longer a high OPM business, but still has potential to grow at reasonable rates.

We have seen how Mr. Market raised the P/E of a mid cap IT company (Mindtree) during 2017 & 2018 from 13 to 31 in span of six - nine months, the same can happen with some other IT and KPO businesses.

Mr. Market sometimes punishes the business badly and then rewards it very soon.

Though eClerx is completely different, but we need to watch if Management can convert the business model slowly, reduce dependency on pure KPO, and make it more diversified over next few quarters.

Disclosure: Invested.

1 Like

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

It appears that the management has put its best foot forward. From being just a KPO, they have started Offices/touch points overseas in seven different locations internationally. That is a big-deal, and is well executed, this is shown by steadily increasing Sales.

With Eclerx, I am sold on management quality and its future prospects, but the only thing that is an eye-sore is its reducing OPM%… it is steadily decreasing for the past decade.

In its AR, the management is attributing this to increased expenses and competition. After OPM% decreasing sharply from 42% to 22% presently, even if it stabilizes here the EPS should steadily start to climb.

I think this should could be a candidate for long term.

Watching.

1 Like

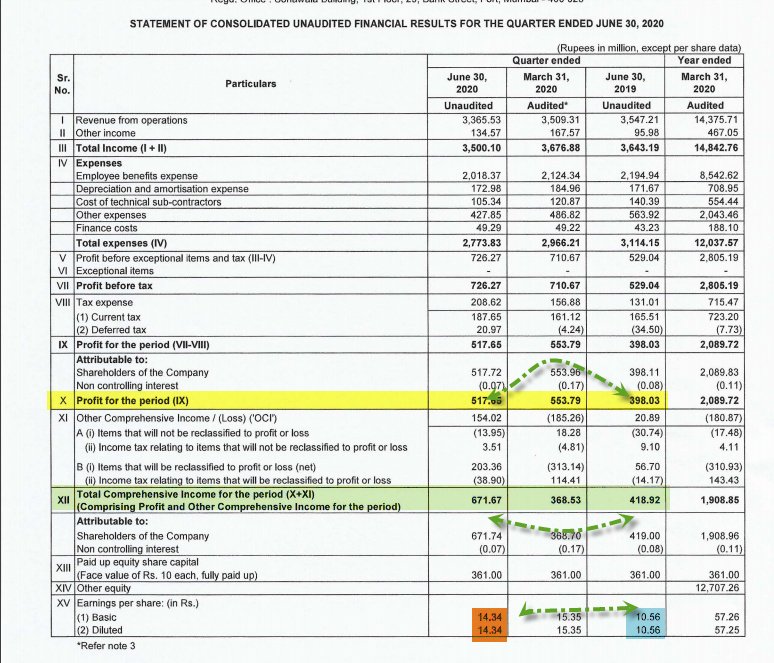

Results are out…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a08a2f82-1a99-490a-b423-76197c930a51.pdf

This looks interesting…

1 Like

Concall highlights

Challenging work-from-home transition: ECLRX faced challenges in getting work-from-home approvals due to the nature of BPO services, especially in the voice segment. Voice delivery has now been partially moved to chat. New laptops and data cards had to be procured, leading to increased costs (~US$ 2mn). About 90% of employees have been transitioned to work- from-home mode. Most banking clients were supportive of this shift. Demand environment severely impacted: ECLRX saw delays in project go-lives and roll-offs due to lower demand, depleting Q4FY20 revenues by US$ 2mn. Clients have reshuffled and reallocated budgets. Top 10 client revenue contribution declined 12.2% QoQ. The impact of Covid-19 reversed gains from improved deal pricing in H2FY20, especially in the top 10 accounts. The travel vertical (~2% of revenues) and managed services have been the worst affected. Retail (7-9% of revenues) was the second-most impacted vertical. Banking, hi-tech and telecom remained relatively resilient. FY20 USD revenue growth was flat, decreasing 0.1%. EBITDA margin for the year improved 100bps due to improved deal pricing.

ECLRX business slows: While the analytics segment maintained growth, managed services which consists largely of travel and hospitality clients slowed down. CLX (based in Italy) was the hardest hit along with the onshore consulting business, reflecting in a 14.5% QoQ decline in Europe revenue (in dollar terms). Some recovery is being seen in the segment as Italy emerges from the pandemic.

1 Like

Not tracking this company lately. However, just observed that HDFC Mutual Fund has significantly raised allocation since the Sep19 quarter.

Sep10 (5.653%), Dec19 (6.068%), Mar20 (6.662%).

Analyst Reports

1 Like

results announced:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aeb1e3bf-4083-4245-9f12-51e25c8a5d9c.pdf

Market seems to have liked it, its up 20% - Upper Circuit.

- Revenue has fallen marginally by 5% both YoY and QoQ

- PAT Q-o-Q seems same with a marginal drop of ~5% but with OCI incorporated almost a ~80% jump in Profit

- Y-o-Y seems 30% increase but with OCI incorporated almost 60% jump

Results have been announced.

1 Like

Seems like this business thread hasn’t seen any updates.

Was doing a sector screening when this looked a little interesting.

“CC growth” keyword search didn’t find any matches in the thread. So checked one of the HDFC reports where this factor was extremely less for a “smallcap” business at ~1.5%

Latest CC growth at 7.6% with attrition rates at 41% !!!

1 Like

no activity on this thread for more than a year.

EClerx Q2 - FY24 Concall Notes :

- Good growth QoQ in sales(5.5%) and profit(27.1%) , margins above Q1 (18.8% vs 15.5%)

- Lower Delivery costs causing EBITDA margins to go up

- Financial, capital market compliance & KYC assistance driving fast growth

- Good Q3 expected. Also revised growth upwards. Earlier gave downward margin guidance.

- Europe, luxury post-pandemic hyper-growth is now normalising.

- Generally, Q3, and Q4 margins are mostly in line or better versus the Q2 margin. So, the same trend can be expected.

- No seasonality in product portfolio in Q3

- 900 Cr cash pile up & looking for M&A opportunities. Recently opened new position of M&A head.

- Looking for higher growth by increasing the onshore sales team. This will depress margins but provide growth in the topline

- Growing headcount in line with sales.

- Hiring in 3 different streams, ML researchers, business analysts and the implementation team as well

- Not seeing a major threat from Gen AI at the moment.

- The FY25 picture will be clearer by Q4 FY24.

1 Like