It is mentioned in this quarterly result. Eclerx had some tax credits which were used to reduce tax outgo and increase net profit in this quarter

But even if you see previous years its consistently around 20%. Every time they cannot have tax credits. Not sure if it is any accounting fraud case.

Notes from my research →

eClerx is the knowledge process outsourcing (KPO) company based out of India. The company has three businesses -

- Financial Services

- Cable & Telecom

- Digital

Financial services was the business that was natively started by the company. The promoters have financial industry backgrounds & that helped them in initial days. The expansion/entry into newer segments has been primarily driven by Acquisitions. Following are the details of the acquisition so far -

The company follow a model where a small team of subject matter experts (~100 to 200) is present in onshore locations & rest of the headcount is based out of India.

More About Businesses

Financial Services

This was the first business area of the company & eClerx provides services like trade processing support, reference data management, expense management, accounting & finance etc. There are two factor based on which this business does well -

- If global banks are doing well, they take long term view of offshoring & that is good for eClerx to get good business

- Regulatory changes like Dodd-Frank Act drives more IT investments & acts as a trigger for company

Digital Services

This business was previously known as Sales & Marketing business. It provides services like - Web Content management, Web Analytics, Competitor Benchmarking & Pricing, Customer Data Management etc. The client list seems impressive at PayPal, Citi Bank, American Express, Sky etc.

As per management, a definitive shift happened around 2013-14 where sales started moving from laptop/desktop to mobile based platforms. This is an encouraging trend over long term.

This business can be categorised into two parts - content creation & content management. To enhance the content creation part of the business, company acquires CLX, a European content creation company for various luxury brands. CLX acquisition provides more products to sell and enhances the service offerings to end to end.

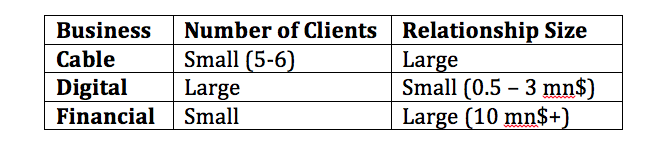

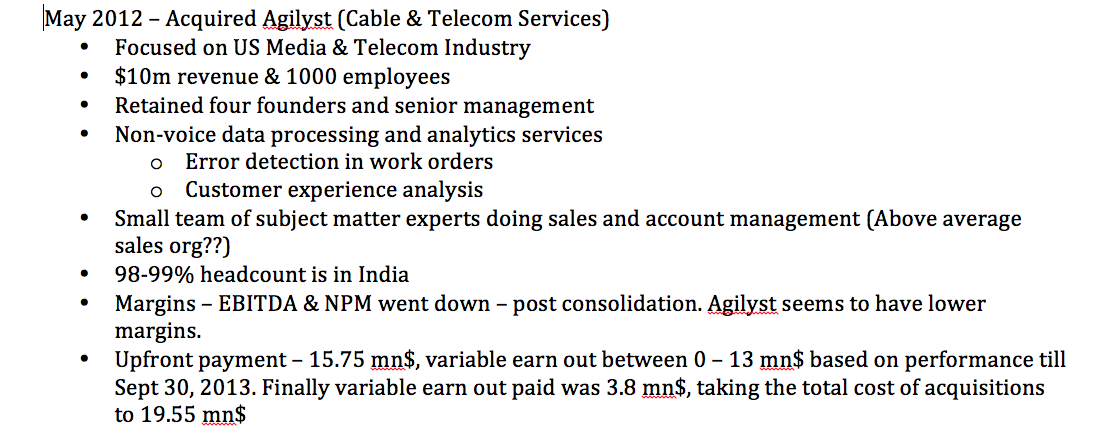

Cable & Telecom

This business division was started with the acquisition of Agilyst Inc. in 2012. Agilyst was focused on US media & telecom industry. The service offerings primarily include - improvement in customer care, reduction of the cost, reduction in work order errors, reducing visits to customer sites, uniform communication & analytics across various communication channels like - web, voice etc.

The client & relationship profile of the business is described below →

Management Team

There are two promoters named - P D Mundhra & Anjan Malik. P D Mundhra has total 10 years experience in investment banking with Lehman Brothers and corporate treasury at Citibank. Anjan Malik ran trading department at Lehman brothers and Senior Consultant – European Capital Markets, Accenture.

This exposure seems to give them good access to financial clients.

In years FY12, FY13, FY14, FY15 – P D Mundhra offered to forgo his annual hike and the offer was accepted. But a handsome bonus was paid to PD Mundhra by board of directors for performance.

The onshore team of subject matter experts seem to have an impressive resume. This is the reason I was led into researching about this company.

Management team seems to have impressive variety and leaders for different geographical regions. Can it be assumed to be above average sales organization from online info (Need to do scuttlebutt?)?

A lot of executives from Dell and some from technological companies like Intel have moved to eClerx. This represents a healthy sign.

More Details About Acquisitions

Agilyst

CLX

PROS

The major reason I got attracted to this company was because of onshore team of subject matter experts. I believe at this point of time that - they represent above average sales organisation & thought leaders in the world of outsourcing. They hail from various background & different geographies. Above average sales organisation remains my primary motivation for investment.

On the face of it acquisitions are bad sign but if one thinks as business owners, especially in IT field, then acquiring small companies with similar profile seems to be better way of expanding than creating service offerings from scratch. Although I don’t know a lot about analysing acquisitions, sales & net profit has grown significantly without much debt every time company has done acquisitions. Above average acquisition strategy remains my second motivation for investing in this company.

The company has consistently maintained operating margins of 30%+ & 40%+ in some years. Highest operating margin remains third motivation for investing in this company.

CONS

Technological automation, robotic automation remains the biggest threat & as per management up to 60% business can be impacted by this. Although company is trying to embrace automation & starting to offer automation services, the revenue on offer is smaller.

Client concentration remains second risk area. The company has reduced dependency on top 5 clients consistently but still derives 57% revenue from top 5 clients.

The stock is already well discovered as 40%+ stock is held by FII + MFs. Further gains for the stocks can come only from good performance.

Revenue is grown by acquisitions. Overprices or unrelated acquisition remains one of the key risk areas for the business.

Miscellaneous

Headcount

Notes from AR

AR FY12

Promoters sold around 10L shares, bringing holding down from 60% to 54%

AR FY14

Net profit grew by 40% due to currency depreciation

AR FY15

PAT margins dipped down from 30% to 24% due to →

Onshore marketing teams expanded to 350 people – causing 41 cr increase in the cost

New facilities were commissioned leading to higher costs

Headcount increase

AR FY 16

Dividend seriously reduced from 35 Rs in FY15 to 1 Rs in FY16. Two promoters (PD & Anjan) used to get 20 Cr+ in dividends. Company initiated buyback at price of 2000 Rs. Need to check if promoters are participating in buyback.

Disc - Invested, 5% of portfolio, not a buy or sell reco

11 Likes

The disclosures are for sale only. Where did you find info about them buying from open market?

Dividend is surely reduced due to additional tax of 10% on dividends above Rs 10 lakhs. Buyback is a better option now for promoters and many companies will be following this. Since promoters avoided dividend for this sole reason, they have participated in the buyback.

Disc - Invested and continue to hold

1 Like

@rupeshtatiya thanks for the analysis. What’s your though on future growth drivers for the company? I have been holding this company since IPO but never really paid much attention to where the growth will come from as their core financial services offering was growing for last so many years. However, that story has largely played out and two other businesses (digital media and cable) are growing but I think these are still small compared to financial services.

Recent buyback of 235 cr although is a replacement of dividends, is about 68% of FY15-16 profits of 350 cr. Last year, dividend payout was just over 100 cr. Such a large payout is an indication that company does not see much acquisition opportunities. Such moves makes me wonder where the growth will come from. Recent organic growth numbers were also tepid.

2 Likes

Yes, the growth visibility for next 2-3 quarters is low. But company said in conference call that they continue to evaluate 25-30 acquisition targets every year & make move when they find something they can buy. So I think acquisition will come along sooner than later.

One of the basic criteria for financial investment business is that US banks should do well. I think US economy & US banks are doing well & I’m hoping to see some action on that front over next 3-4 quarters. The digital & telecom businesses are growing at good pace.

Regards,

Rupesh

2 Likes

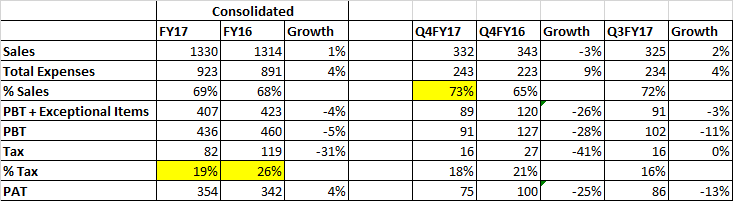

Eclerx Q3FY17 results & investor presentation out -

- PAT has grown on 9M basis due to lower taxes paid.

- Operating margins took a hit - company claims this is due to first year of adoption of Ind-AS accounting standard.

- Company expects headwinds to continue till Q1FY18.

Disc - I continue to hold, not a but/sell reco

1 Like

Q3FY17 Conf Call

Growth

The reasons for lackluster growth are automation, in-sourcing, Mergers & Acquisition on client side.The revenue loss is due to very client specific reasons (of large 2-3 clients). One of the client (large?) got acquired & new management philosophy is to source work locally rather than off shoring.

The growth momentum from new clients still remains decent. The growth in base financial services was very good. A lot of growth is driven by tier 2 clients, they have potential to grow to become large clients. If regulation (like Dodd-Frank) is reduced, some existing business might be reduced but our customers would see increase in revenues (which they haven’t seen in sometime) & that might lead to more trading.

RoboWorks

RoboWorks is proprietary robotics platform of the eClerx & it has been successfully deployed across 3 verticals. The company keeps looking for opportunity to deploy it in all projects. So far, 600 employees have been trained on RoboWorks, the company plans to double the count next year.

The banking vertical is attracted to bot like solutions more than digital or cable.

Robotics & Automation have always been headwinds for all our businesses, the risk profile has not changed much in last 4-5 years. The business is shifting to work that is left after automation.

H1-B, Trump, Employees

Business/Revenue is not impacted by H1-B potential changes as number of employees in onshore team are small & we always strive to & will continue hire locally.

Employee cost will remain elevated level as planning to shore up onsite team. Capex expected to go up over next 2 years

Total number of employees stand at 8648 out of which Sales & Marketing staff is around 81. The attrition rate is down from 41% to 33% this Quarter which is lower than yearly average.

Disc - I continue to hold, not a buy/sell recomendation, please do your own diligence

2 Likes

This was a big part of my portfolio and I really liked this company due to the strong capability it had build and the great execution capability along with a great management. I think this still hold true but the sector (knowledge/transaction processing outsourcing) is facing fundamental shifts. Automation/Insourcing is going to be a threat and it is now seen in the poor growth Eclerx is showing and is also projecting in some time.

It is probably the best managed company in its sector but what do you do when the whole sector is facing headwinds.

I have exited my position as I would want to allocate this to businesses that have more clarity in terms of sources of growth in the medium to long term.

Again this may prove to be a mistake and this post will be a reminder for that but some of my fundamental concerns and questions on the business are not getting a positive outcome i am looking for.

Key trigger for me to exit is when you start consistently losing business from your core clients. We could see a recovery and will continue to be interested in the company but I feel I have better options right now to invest in.

It was my top 3 holding and had spent quite a lot of time to think over this. There is a tendency to double down and fall in love with your top pick and back it. But I would always rather Average up and than Average down at reasonable valuations in a company that continues to do well.

4 Likes

you are not alone, this was 20% of my portfolio and I exited

however considering the stock I have made an SIP and will come to 10% of my Portfolio in next 6 month

stock should bounce back in few quartes

eClerx Q4 Update

Results

Q4FY17 Conf Call

INDUSTRY

Due to political environment and other technological updates, clients prefer to reduce cost through automation compared to outsourcing. Tech enabled businesses are emerging as challenging competition.

GUIDANCE

The current pipeline that company has visibility over is largest over last 4-5 quarters. The new contracts and orders are similar to last year. The company has added large number of clients in each of the business verticals.

Previously the company was expecting Q1 FY18 to be a soft quarter as some work was supposed to be finished transitioning from company to client. That now has been delayed by one quarter and company now expects that Q2 will be soft instead of Q1.

Overall there remains softness with top 5 clients and company expects growth to be driven by emerging clients. The on-shore revenue is still in high single digit percentage excluding non-CLX revenue.

The tax rate in FY17 was low at 19% as company used MAT credits. As company has used all MAT credits, the tax rate would go back to normal of 25%. There will be impact of increased salaries after April, the company expects high single digit hike for India employees and low single digit hikes for overseas employees.

BUSINESSES

The largest revenue generating business for the company has been Digital by a large margin. This is followed by financial services business which has a very large margin over Cable business

i.e. Digital >> Financial >> Cable

For the businesses that have large on-shore staff/operations, OPM is low e.g. CLX and Onshore Consulting.

Overall the company’s total business still remains a concentrated one where top 10 clients contribute 70% revenue and top 5 clients contribute 60% revenue.

Digital

In this business, there were some instances of re-shoring or near-shoring the work along with reduced contract spend and duration commitment. This has been the best year so far for Analytics business. Some cliche stuff was mentioned like - we are moving from data to value extraction and some analytics services are taken to other businesses.

Financial

In last few quarters, the increase in new sales (new clients or new services) has been strongest. Even in FY17, there has been decent growth in the revenue of this business. We feel that tailwinds for growth are developing for this business and expect it to pick up over next 12-24 months. The capital markets provided good revenues, mentioned derivatives moving from OTC to something (?).

Cable

The clients in this business are very new to outsourcing. There is some M&A activity going on in this sector which will impact the company in Q1FY17. We are in advanced stages of talks with 2 potential clients.

CLX

The CLX is the content production business and it contributes 20-22 mn Euros in the revenue. This has been a very mature business for last 40 years. The expected growth rate in CLX are high single digit. Since this business is primarily on-shore business, the OPM are low in this business.

On robotics front, company has tried to do more partnerships and tried to integrate some layers of machine learning. Company has also increased employee training on this robotics platform.

NEW INITIATIVES

The company has started following new initiatives -

- The company has been trying to cross sell the services to clients from different businesses and this is in very early stages.

- The company has started centralized client marketing method. I assume this is meant for “wide” marketing of products across different business verticals.

- The company has started first delivery center in the US in North Carolina. This will be used for clients who expect on-shoring or near-shoring.

- The company has started another office in Austin and this will be primarily used for Analytics business.

- The company has incorporated a Canadian subsidiary and expects boots on the ground in coming future.

HIRING

The company has hired managing principal in US to manage some sub-vertical (?) in Financial vertical. The company has also appointed independent board member who that relevance/experience of client market and has formed advisory group.

Disc - I continue to hold

1 Like

Reviving this thread. With the buy back around the corner and with a steep climb up on Fri (22/12/17), is there juice left? also, the wording was a tad vague…not exceeding 2000 Rs …given that there are far more qualified folks in this board to predict the possible Acceptance ratio of retail, can someone take a stab at it please? Thx

1 Like

Considering the promoters are also participating in the buy back, I wanted to know is it a mandate to allocate a certain portion of the buy back shares for retail quota?

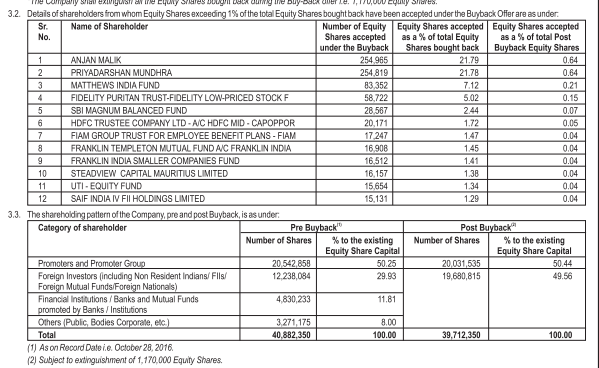

Here’s a nice analysis of similar buyback by eclerx in the year 2016.

This time the situation doesn’t seem very different.

A quick and dirty exercise to see if any juice is left for special case investing in Eclerx:

Assumptions: Investor buys @1550 to participate in the buyback. Qty: 100 Shares. Post buyback price: Rs.1300 (where it was when buyback was announced). At theoretical acceptance ratio (~12%) this is strictly a no-no.

As you can see from this table, acceptance ratio increasing to 25% shall also not help!

Another case, assuming post buyback price of Rs.1400.

Still, 25% acceptance ratio brings you to breakeven, and no money to earn.

Please also note that all these calculations are without brokerage or taxes.

Only case left is that of investors who bought shares earlier, say @1300 or @1400, then they should participate and earn some quick, short term gain.

Disc: no investment.

1 Like

A sudden jump in the prices of Eclerx. I didnt find any news item related to this. Any ideas

Hi,

Is eClerx loosing its competitive advantage?

ROE has been reducing every year, and now as per screener.in, it is close to 22%.

OPM has also reduced over a period.

On the other hand, promoters seems to have increased their stake.

Does any one is holding and tracking this? I would like to know if eClerx management is doing some thing in digital and automation areas, to improve efficiency so that further margin erosion will not happen.

Any views are welcome.

Disc : Tracking closely as it looks good business available at fair value.

I was listening to the commentary from past 2 quarters from management. Following is what I make of this:

Operations:

Onsite expenses are increasing. They hire employees and train them for few months before putting them on projects. They hire in anticipation of demand in small lots.

Offshore is hit badly with deals rollover issue. Attrition is as high as 45% because of projects closing. This was high margin business.

Clients are hit by tech innovation and hence not much on tech spend from them.

Big deals are not going through. They did crack a 1 deal in 5 million range. and lost some in 1-5 million range.

OPM and EPS are both downwards.

Revenue has finally increased after 2-3 years of lull. Next 2-3 quarters are to be watched. Commentary was not so rosy, with scepticism all over.

They have consolidated the facilities in Pune and they have capex there which has hit profits and EPS.

Disc: invested a small amount.

3 Likes