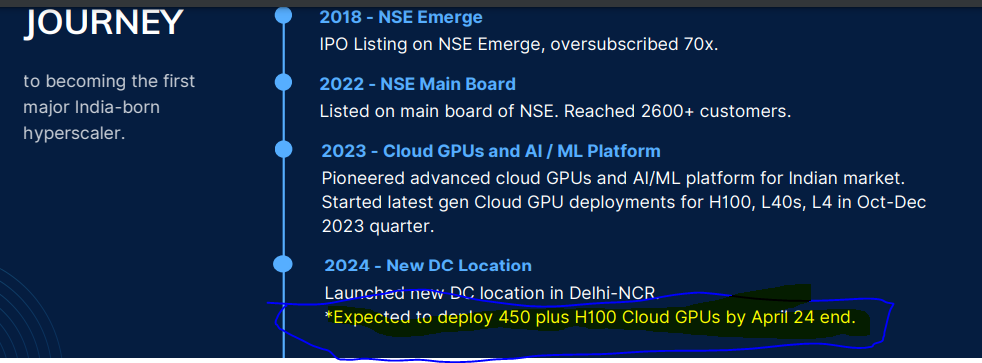

Latest Investor presentation from E2E networks. Seems they are already procured 140 CR on GPU (450 nos of H100 GPUs) from planned 200 to 250 cr this financial year. in last qtr concall, CEO was saying, they would procure 30 to 40 CR GPU in first batch. but looks like they are giving conservative no in concall.

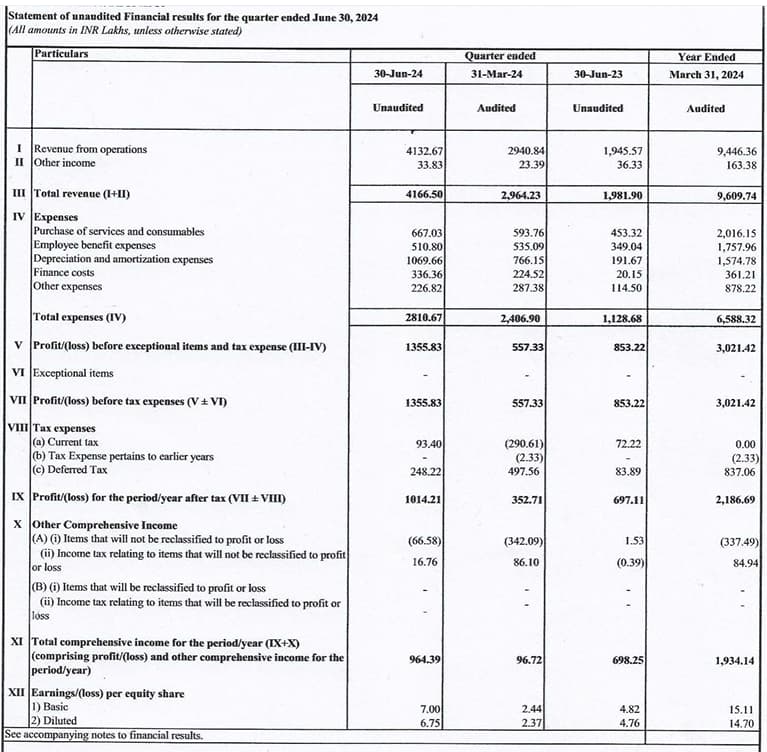

Results have just come out. No complaints except reason for rise in other expenses. Revenues have really increased and I can excuse temporary dip in bottom line when company is in high growth mode. Their finance costs have also increased a bit. https://nsearchives.nseindia.com/corporate/Signedfinancials_24052024142750.pdf

Key points from the conference call: The FY25 capital expenditure plan is set at 800 crore, to be funded through a mix of equity, debt, and vendor financing. The MRR could increase to 16 cr rupees with full capacity utilization, up from the current 10.8cr rupees. Management is highly confident in their competitive advantage and the industry demand outlook. They are also planning geographical expansions, which will significantly increase their Total Addressable Market

Thanks for sharing, This looks like repeating in Esconet now. Mcap/Sales at 1.5 and acquired Zea cloud focussed on SME clients. Have you looked at this ? Any thoughts ? thanks

Netweb and Esconet don’t fall under the category of compute providers; rather, they serve as system providers. This is an important distinction because compute providers typically require robust software platforms, comprehensive developer documentation, APIs, and integration capabilities, none of which are their primary focus.

Moreover, both Esconet and Netweb are primarily engaged in the delivery of hardware systems and servers. Therefore, while they could potentially serve as clients in an end-to-end setup, they don’t operate on the same level as compute providers and are better characterized as clients rather than peers in this context.

Zea Cloud is a typical Infrastructure as a Service (IaaS) provider, not an advanced computing platform which E2E is. Their services are so conventional and basic that you can find at least a handful of similar vendors in India offering the same.

In future if they do develop and launch some new offerings then it can be considered

E2E Networks Receives Cloud Service Provider Empanelment from MeitY

Commenting on the MeitY empanelment, Tarun Dua, Managing Director of E2E Networks said, “Today’s announcement of MeiTY empanelment presents a plethora of opportunities for us to assist India’s government agencies and public sector organizations in expediting their digital transformation, as over 3,000 customers have already reaped the benefits of E2E Cloud Infrastructure. We are dedicated to the expansion of our team in order to accommodate the substantial growth of our public sector business.”

Recently I have been doing the research on the cloud computing space in the GPU era and I have found some astonishing facts. Some of them are as follows:

Global Cloud Computing Market: The global cloud computing market is projected to reach $2.5 trillion USD by 2032, up from $500 billion USD in 2022.

Top Cloud Service Providers: The three leading cloud service providers—AWS, Azure, and Google Cloud—are expected to hold a 36% market share in the $2.5 trillion cloud computing market (approximately $900 billion USD). This growth is driven by the ongoing AI revolution.

Indian Hyperscalers: Currently, there are no hyperscale cloud providers originating from India.

Yotta’s Initiatives: Yotta, a player in this space, has ordered 16,000 NVIDIA H100 chips, with a total acquisition and implementation cost of around $1 billion USD. The shipment was scheduled for receipt by June 2024. Yotta has launched its own cloud computing platform called Shakti Cloud, which has already sold out its capacity, with more companies on the waiting list.

Yotta’s Cloud Capacity: Yotta’s cloud capacity is sufficient to train two ChatGPT-4 models within three months.

Global NVIDIA Chip Shortage: Despite TCMC doubling its capacity in 2023-24, there remains a global shortage of NVIDIA chips. TCMC plans to double capacity again in 2024-25.

Challenges for Indian Data Centers: Indian data centers, even the latest ones, are not adequately equipped to handle the power and cooling requirements of next-generation GPUs like the H100 and Blackwell. Reengineering is essential to host cloud computing in Indian data centers.

Indian Public Cloud Services Market: In 2023, the revenue from Indian public cloud services (including IaaS, PaaS, and SaaS solutions) reached $8.3 billion USD, according to the International Data Corporation (IDC). The overall Indian public cloud services market is expected to grow to $24.2 billion USD by 2028, with a CAGR of 23.8% for 2023-28.

E2E Networks Concall Analysis

Capex and GPU Acquisition: In FY 2023-24, E2E Networks invested approximately ₹145 crore in fixed assets, primarily acquiring 450 NVIDIA H100 GPUs. The cost per GPU was approximately ₹32 lakhs.

Monthly Recurring Revenue (MRR): Following the recent capex, the company expects an MRR of ₹14-16 crore. For FY 2023-24, the MRR stood at ₹7.83 crore.

Incremental Revenue and Profit:

The increase in MRR amounts to ₹8.17 crore, resulting in an annual incremental revenue of around ₹98 crore from the current year’s capex.

The incremental PAT (Profit After Tax) is approximately ₹12.48 crore.

Assumptions: EBITDA margin at 51%, depreciation based on a 6-year straight-line method, interest cost at 9% for outstanding short-term and long-term borrowing, and a tax rate of 25%.

Note: There is a scope of improvement in EBITDA margin.

Guidance for FY 2024-25:

The management aims for an ideal capex of ₹800 crore in FY 2024-25.

Assuming consistent parameters, the company could acquire 2500 H100 chips with this capex.

Incremental revenue from the ₹800 crore capex, following the same MRR Increase/capex ratio, would be ₹540 crore.

Incremental PAT would be approximately ₹79.52 crore.

Assumptions: Source of funding – 50% debt: 50 % equity, EBITDA margin at 51%, depreciation based on a 6-year straight-line method, interest cost at 9% for outstanding short-term and long-term borrowing, and a tax rate of 25%.

Note: There is a scope of improvement in EBITDA margin.

Total Peak Revenue:

After the ₹800 crore capex, the total peak revenue is projected to reach ₹732 crore.

The peak PAT is estimated at ₹111.34 crore.

Challenges/ Questions for which I am looking the answers for:

Sourcing NVIDIA H100 Chips: Will the company be able to source NVIDIA H100 chips?

Fundraising for Capex: Will the company be able to raise funds for the required capex?

Data Center Space: Will the company be able to obtain the required space from data centers for running the GPUs?

Selling Cloud Computing Space: Will the company be able to sell cloud computing space to customers?

Technical Readiness and Staffing: Is the company well-equipped technically and does it have the required number of employees to cater to such a large number of customers?

Product Strength and Demand Creation: Is the company’s product strong enough to create this kind of demand?

Competitive Strengths: What is the company’s right to win? What are its competitive strengths?

Software Stack Importance: What is the importance of the company’s software stack in the GPU era?

Feel free to share your findings, and I’ll be here to continue the discussion!

Question Sourcing NVIDIA H100 Chips: Will the company be able to source NVIDIA H100 chips?

Answer: I have gone though some research material and I have found out some insight into this topic:

A) Partnership with NVIDIA:

NVIDIA lists three types of partnerships on their website: ELITE, Preferred, and partner.

There are a total of 73 cloud partners for NVIDIA. Among these, 19 are elite partners, and 61 are preferred partners.

In India, there are only two cloud partners, both of which are preferred partners: E2E Networks Limited and Yotta Data Services Private Limited.

Advantages of being a preferred NVIDIA partner:

Sales and Distribution Support: Preferred partners gain access to enhanced sales and distribution resources, enabling them to reach more customers effectively.

Training Opportunities: NVIDIA provides specialized training programs, allowing partners to build expertise in GPU-accelerated computing and stay up-to-date with the latest technologies.

Marketing Collaboration: Preferred partners can collaborate on marketing initiatives, co-branding efforts, and joint campaigns to promote their solutions.

Service and Support: These partners receive priority support, ensuring timely assistance for technical queries and customer needs.

Recognition and Rewards: NVIDIA acknowledges their commitment by recognizing Preferred partners and rewarding their achievements.

B) Commitment done by Jensen Huang -

India is getting special attention. In September’2023, Huang met with Prime Minister Narendra Modi and said he would prioritise any orders from data centre operators in country. “You have the data, you have the talent,” Huang said at the time. “This is going to be one of the largest AI markets in the world.”

“In pursuit of this goal, Yotta is acquiring 16,000 of Nvidia’s H100 Tensor GPUs. After all, Nvidia practically owns 90% of the GPU market. This acquisition is noteworthy considering the global shortage of Nvidia H100 GPUs, which has caused delays in numerous major projects worldwide. Despite the challenges posed by the global GPU shortage, the breakthrough in securing these GPUs for Yotta followed Prime Minister Narendra Modi’s meeting with Nvidia CEO Jensen Huang.”

“In September, when Jensen Huang, founder & CEO, Nvidia came to India, he had met Prime Minister Narendra Modi. At that time, Prime Minister had expressed his desire of bridging this gap, helping India come at the forefront of AI, and even sought Huang’s help for the same. The Nvidia CEO offered PM Modi to help in his best capacity possible by offering technology and support to the local providers,” says Sunil Gupta, Co-founder & CEO of Yotta. He adds, “As somebody has to invest in, take a step forward to build this infrastructure in India, Yotta took the first step and placed the order.”

Nvidia and India have a shared interest in betting on, and speeding up, the country’s AI ascendancy. Chipmakers cannot sell top-end microprocessors to China, which accounts for a fifth of Nvidia’s sales, amid fears the chips could be used to develop autonomous weaponry or wage cyberwarfare.

“India is the only market remaining so it isn’t surprising that Nvidia wants to put multiple eggs in that basket,” said Neil Shah, vice president of research at Counterpoint Technology Market Research.

Read more at:

D) Sovereign AI –

Sovereign AI refers to a nation’s capabilities to produce artificial intelligence using its own infrastructure, data, workforce, and business networks. Essentially, it means that a country aims to rely on itself for AI development and usage, without external dependencies. This concept transcends technology; it’s about a country’s identity and autonomy. By building its own AI capabilities, a nation can strategically protect and advance its interests in an increasingly AI-driven world.

NVIDIA has openly advocated for democratizing AI and has talked about the importance of sovereign AI at various occasions and conferences. This will help all the nations in building its own AI capabilities starting from data centers infrastructure, cloud computation to using its own data to create its own models and AI.

E) Small Quantity required compared to total Nvidia GPU production –

In Year 2023 the company sold around 550,000 of its latest H100 compute GPUs worldwide in 2023, with most going to American tech firms. Looking ahead to 2024, Nvidia plans to at least triple the output of its compute GPUs, including the H100, GH100, and other processors for artificial intelligence (AI) and high-performance computing (HPC) applications. The projected shipments for 2024 range between 1.5 million and 2 million units.

Despite this growth, the E2E network requirement remains minuscule compared to the total number of units produced.

I have invested a small amount, and I want to put more. However I am a bit confused about the valuation. PE is 107, PEG 1.5 and TTM current EPS growth is 75% as per screener.

There are FMCG companies growing at 8% but command a PE of 90-100, compared to them, E2E still looks better priced. However, E2E also carries a lot of debt.

Does anyone have a view on valuation? Is it cheap/expensive at current level, what is your perspective.

Capex Commitment: The management clarified that they are not committing to an 800 crore capex. In the previous concall, they mentioned that ideally, they would need to invest 800 crore capex, which was misunderstood by investors. This quarter, they have denied providing that guidance.

*Demand and EBITDA Margin: Despite not committing to the 800 crore capex, the demand remains very high. The management expects to maintain the same EBITDA margin going forward.

Strategic Shift The management is shifting their strategy to focus on high-end players, whereas previously, they were onboarding all small players. They believe the market size is sufficient to accommodate more players like them.

International Business: Their medium-term goal is to achieve 30% of their business from international markets.

Technology Implementation: Coming quarter, they plan to implement 256 H100 chips, bringing the total to 700 H100 chips.

ARPU Improvement: The management is optimistic about improving their ARPU from 7.5 lakh.

Current Quarter Capex and Utilization: The current quarter capex is 23 crore, with a 90% capacity utilization rate. Their MRR is 14.5 crore.

EBITDA Margin Sustainability: The management is optimistic about sustaining the EBITDA margin even with the emergence of more players.

E2E is not a company that is to be judged or invested in based on screening filters. This is evident by the fact that this stock never got talked about much or hyped. It just didn’t meet anyone’s criteria based of its unique circumstances and so didn’t show up on most screeners.

The PE that you are seeing is momentary. A doubling of earning would lead to halving of the ratio. The question is would that take 1 year, 2 years, 10 years? So, the discussion of it is not really from the perspective of today. E2E’s proposition is from a future perspective.

Talking about the future, anyone who does a deep dive into the company’s product and offerings, will know that this is a capex heavy business, despite the fact that the value generation happens at the software layer: the custom software the comp. has been building over the past decade. It is due to this that the debt also comes into play. Tarun Dua is a not a business magnate. He’s a tech guy who happens to run an IT firm. Fiscally, he’s been pretty conservative till now. Also, the way the company pivoted from a cloud player to a AI first cloud player is understated and under-applauded, showing his firm understanding of the industry and a nose to sniff out the directions the winds are blowing.

It is due to this upcoming obscene demand stemming from AI workloads, company needs to expand quickly. The cash reserves are not sufficient and raising equity is an option, just like debt. The question is not the high/low debt. The question is whether you think the comp. will be able to pull off the large risk it is taking.

To answer that question, I turn to 3 things:

The asset turn - which for E2E is awesome

Whether the comp. will use the fund judiciously - to be seen. Will raise eyebrow if c-suite gets big bonus cheques this year

whether the demand for the assets purchased (mainly GPUs) is good. - In recent concall, Dua estimated that their top GPU H100 has 90-95% capacity utilization though they have reserve GPUs and can acquire more if need on a short notice.

#1 is a number thing that is verified. #2 is a time thing. Let’s wait and see #3 is a trust thing. Whether you believe this statement or not.

IMO, the recent quarterly results are a good indication of what’s to come in the next few quarters. I think we’re looking at a multiple times EPS growth in the next 4-6 quarters. How that works for the valuation will be dictated by Mr. Market.

I have been invested since E2E had a 65cr market cap and still believe the company is walking the talk and will continue to hold. I am probably biased.

Disclaimer: I am invested. This is not investment advice.