The QIP issue is closed already. The fact that they opened the issue yesterday (Feb 25) and closed it today (Feb 26) suggests the “book” was oversubscribed almost immediately.

1 Like

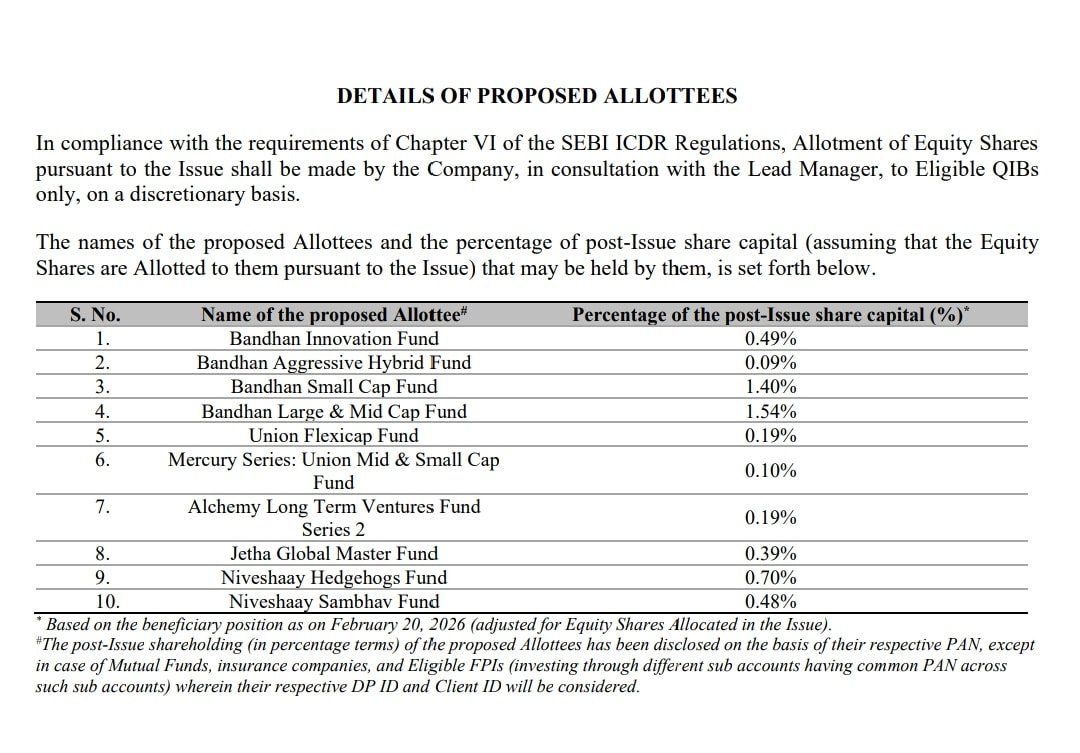

anybody knows the size of QIP. news articles are allover the place. some say 100+30 crore , some saying upto 1000 cr.

Total 107 cr raised by QIP at 2500 per share

1 Like

E2E Networks Limited has issued 4,28,000 equity shares at ₹2,500/share (₹10 FV + ₹2,490 premium), aggregating to ₹107 Cr.

1 Like

If they continuously dilute their equity the existing investor will suffer.

raising 107 crores v/s the capex needed, does not make much sense?

what can they do with 107 crores more in terms of capacity expansion?

Diluting equity is not an issue as long as they are raising at higher and higher prices. I am upset that this is effectively a down round from the LnT acquisition. But regardless 107 Cr will not dilute too much as that is just 2% of the market cap.

If tomorrow E2E goes to 5000 Rs+, they definitely should raise as at higher prices, Equity is better than debt

2 Likes

Just a thought connecting a few dots here and happy to take inputs.

One of the large customers for E2E is Gnani. Gnani serves BFSI clients, and in many cases, BFSI players prefer on-premise or dedicated infrastructure rather than relying on public cloud, primarily due to data security, regulatory, and compliance considerations. These institutions are more likely to deploy their own GPUs or dedicated infrastructure.

In such a scenario, E2E could potentially have an opportunity to position its sovereign cloud offering. Being an Indian cloud provider and one of the older players in the space, E2E may be well placed to cater to BFSI clients that require localized, compliant GPU infrastructure.

I tried to informally confirm this with a Gnani executive in India AI Summit, who indicated that they are unlikely to provide APIs directly to banking customers. Instead, these customers would need to host the infrastructure themselves, especially in BFSI use cases.

If this understanding is correct, the opportunity size for E2E could be meaningful, given that it is among the few players offering sovereign GPU cloud infrastructure in India.

Disclaimer: These are personal thoughts, not verified with management. Views may be biased as I am invested.

6 Likes

BFSI customers and PSUs generally ask for Datacenters in India for Cloud Service Providers. If that requirement is getting fulfilled then it is fine with them as well as regulators.

1 Like

As per MeitY, data centre capacity in the country has grown from 375 MW in 2020 to more than 1500 MW till 2025.

The Government of India is taking measures to promote adoption of Artificial Intelligence (AI) and digital technologies, including for MSMEs. The IndiaAI Mission is a comprehensive initiative, approved by the Government on 7th March 2024 with a budgetary outlay of ₹10,371.92 crore. India AI mission encompasses key pillars of the AI ecosystem including, India AI Compute Capacity, India AI Innovation Centre, India AI Datasets Platform, India AI Application Development Initiative, India AI Future Skills, India AI Startup Financing etc.

2 Likes

have few questions , may be answered in next concal

1. are they pivoting from gpu as a service to pure software stack provider? then what is the revenue sharing model? VYOMA will be having 20000 blackwell gpus at year end what would the role of e2e? is e2e would be the FRONT GATE of the ai factory?

2. what is the specific road map for next few years to capture the massive growth in data center?

3.the purpose of QIP fund raise?

YOTTA is v clear i think they will be having 20000 gpus at year end and doing partnership with big hyperscalers, e2e some how lacking in commercial deals. or they have some complete different road map?

2 Likes

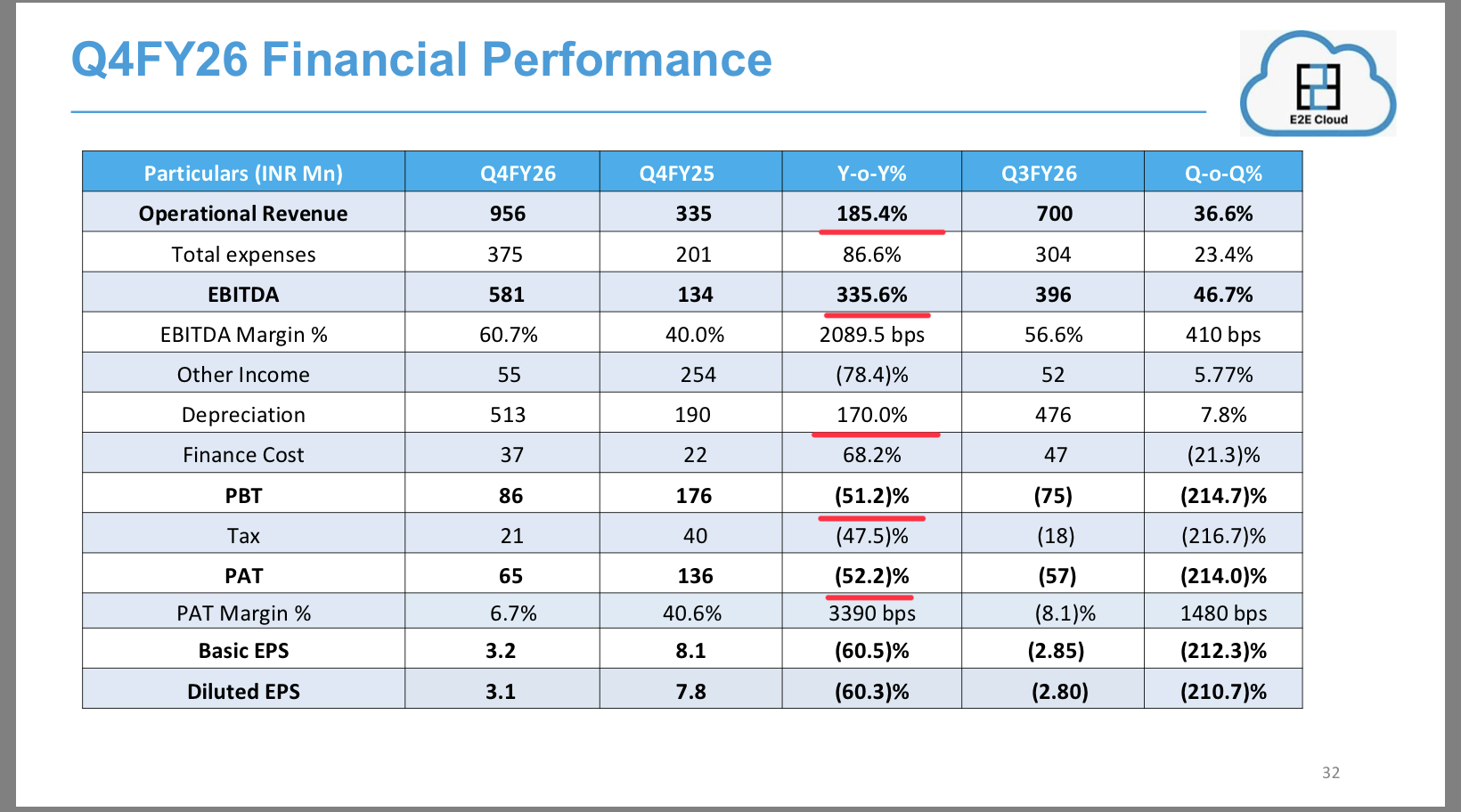

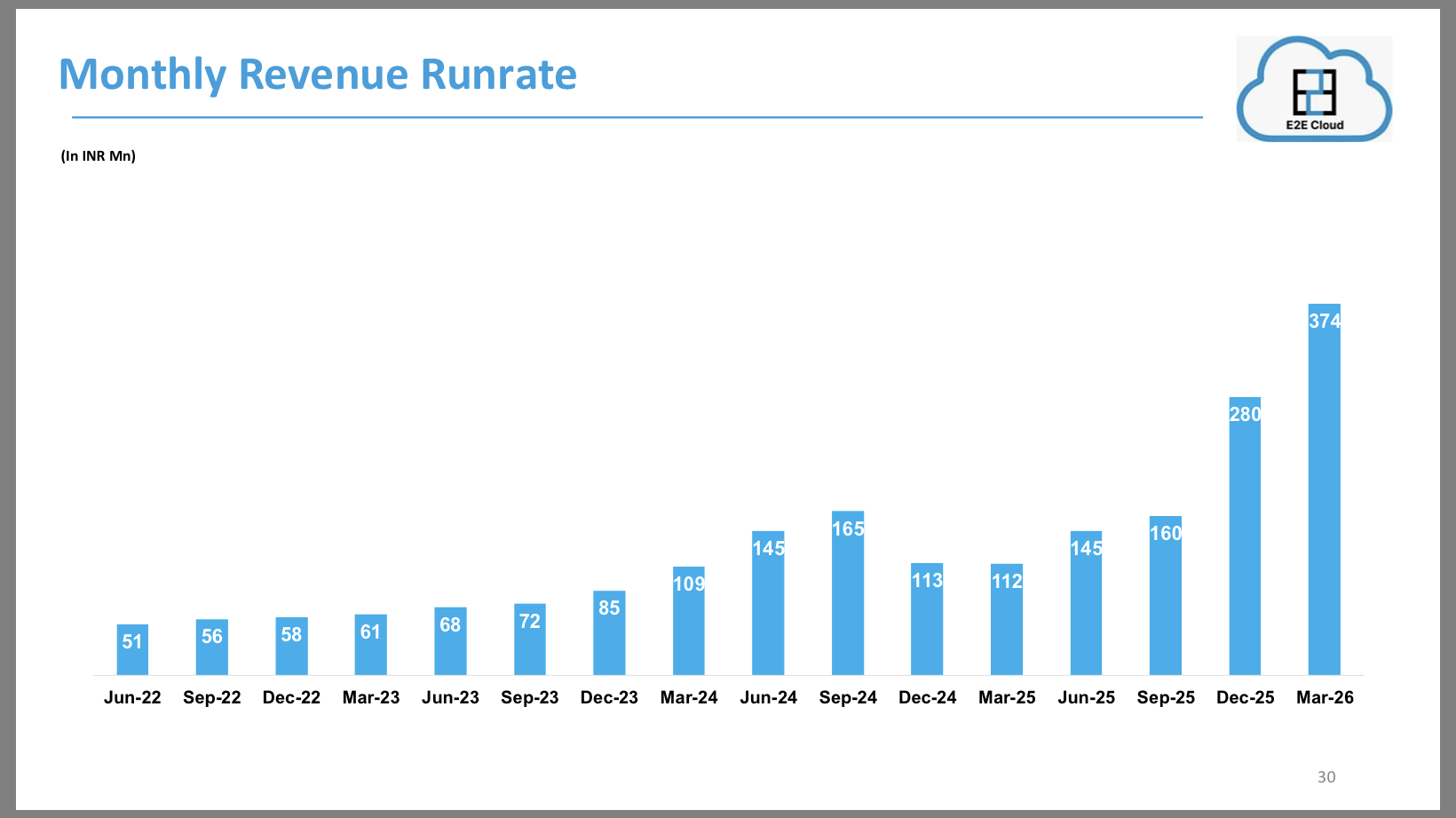

E2E networks results : Top line and EBITDA showed good traction. PAT was down due to high depreciation. MRR in March inched up to 37 cr which is above the guidance .

5 Likes

Right way to look is P/CFO. 122crs is CFO in FY26 and market cap is Rs5569crs crs so stock trading at 45x P/CFO which very reasonable given future growth.

5 Likes

Rather upbeat conference call. Minimum 6000 GPUs by year end and maximum is unconstrained. Looks like a good sign. Literally only negative according to me was the delay in setting up the GPU cluster but hopefully that gets resolved. Else it seems management has made clear that lumpiness should reduce drastically, guidance not given because they want to aim for the highest upside and plans to monetize beyond asset turn on GPU’s

5 Likes

35% export revenue was also a good surprise honestly. If global GPU shortage gains significant momentum then players like E2E will be reached to by global token consumers. I just hope they sell at competitive prices to them.

We have been getting too much of ‘we are prioritizing for indian enterprises/ India AI mission’ which I do not like that much. They should bring forward their long term growth strategy in front of the investors so we always have that default narrative to fall back to and talk to them about instead of them always inserting ‘focus on IndiaAI’ in every other answer. They can say whatever they want to meity to manage their relationship with them and those things like all govt programs can come and go but object clause purpose of business remains.

4 Likes