The best part of the above video is from 55 minute onward

3 Likes

Thanks. Good to hear about the Soverign part & AI etc.

Exirlted from E2E today, result are not good

this is the biggest issue for a company like E2E.

came across this report. it breaks down the unit cost economics beautifully.

4 Likes

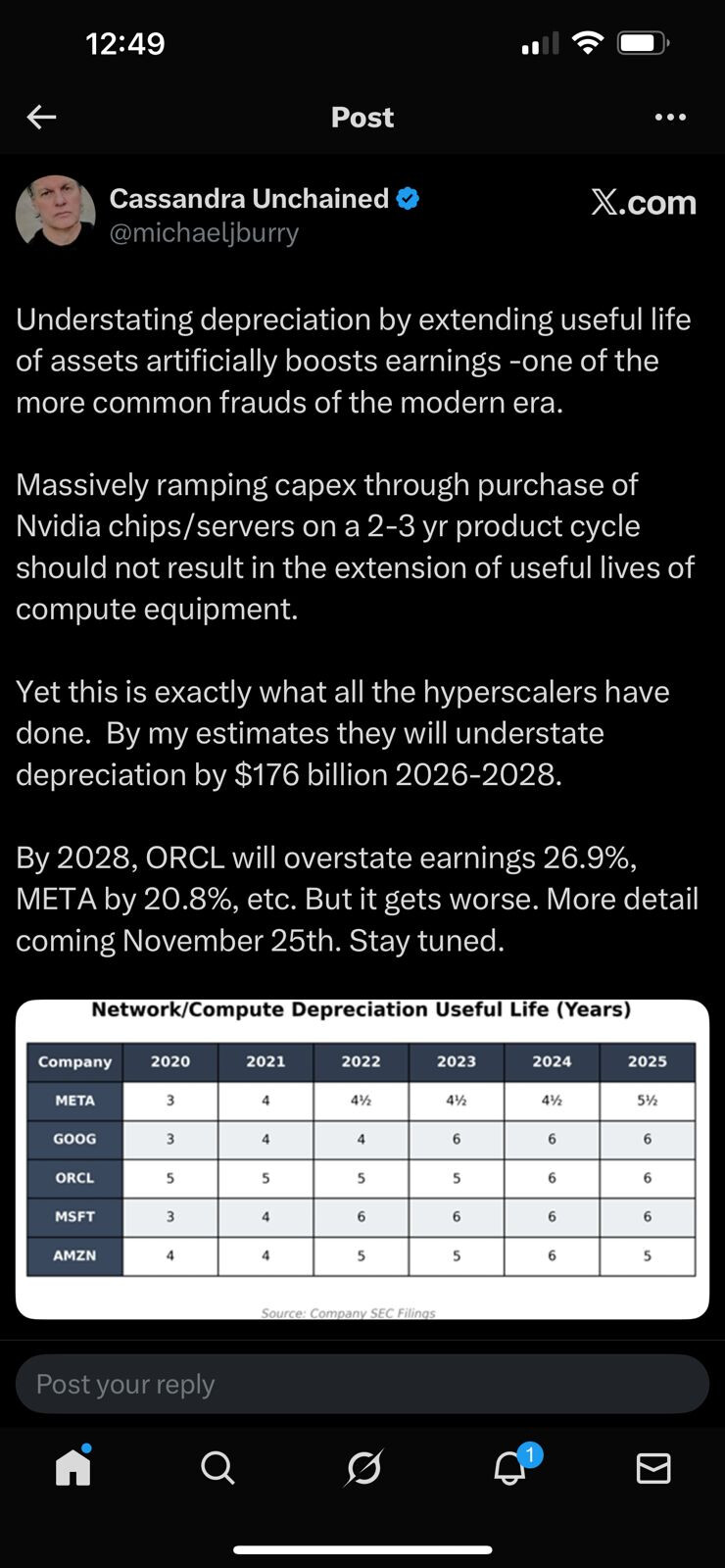

As per concall, management is confident in achieving their guidance of 35-40 cr MRR even before March. They are also looking to buy 2048 Blackewell Gpu before Fy26. As per them GPU life is 7-8 years.

5 Likes

I think one should not take the management’s words at face value, but try to assess things independently. I have not gone deeply into the issue, but whatever I have read/ listened to suggests, it is unlikely these chips will be effective for 7-8 years. That is to say, they will work, but their performance will degrade, as a newer generation of chips will come to make the older chips obsolete. An imperfect analogy will be the telecom Industry and its cycle of constant spectrum auctions for upgrades (2G/3G/4G/5G etc)

You can listen to the following podcasts to get some more depth

D: Not invested.

2 Likes

Once they hit their 35-40 MRR run rate than they become a cash generating machine of about 300 cr per year. That is when the narrative could switch. That alone can help fund further chip acquisitions though i believe they will do another raise when share price improves.

There have been many bearish on CoreWeave but time will tell the outcome. No one knew AWS would be so siccessful!

Can you explain in detail how they are going to generate 300 crore cash per year with 35-40 ARR ??

1 Like

At 40cr MRR annual revenues will be 480crs. Company was expecting margins to move up to 70% on better utilisation on concall held yesterday. Let us take 60% margins then EBITDA will be 288crs.

4 Likes

Can someone explain me how balance sheet has shrunk byalmost 800Cr since year ended in march to now? They had money in deposits (Other Bank balances in current asset) as well as in CWIP+plant&equipment. CWIP has fully shifted to Plant & equipment but what happened to other balance going from 893Cr to 6.9Cr? If they would have give money for order of blackwells should that not appear in some kind of advances line item or something? what happened here?

1 Like

The way AI is changing and new gpus are introduced every month, I see any infra hosting coming soon falling to huge depreciated assets burning cash without subscription. As newer ones are more efficient and cheaper that old ones.

1 Like

As per my calculation. They will have 200 cr depreciation per year given 1200 cr+ capex in total which is done or will be done in few months. As they previously mentioned in last concall life of GPU around 6 years.

So I feel next year end FY 27(not FY26) they should should become profitable.

Lot of positive things keeps going on in this sector, so never know if some big client comes and things start moving a lot earlier.

Disclosure : Biased was holding but sold after last q1 result and depreciation thought. May add again.

Same thoughts, and so stock will stay in range or go lower for at least a year.

Can’t say anything about the stock price as this is very dynamic field and one positive order/partnership will change all dynamics but yes profit should take time of 1 year plus to justify these valuations.

1 Like

If management is planning to do capex (Already placed order for 2048 Blackwell) then they must be seeing the demand.

2 Likes

57% from 52 week High,

RSI Below 28,

Result negative : Depreciation Hit due to 35% utilization rate. Need to improve Sales to counter the depreciation. Two in Hand Orders can bring momentary relief.

Very Hot Sector

Very High Pessimism

Opportunity or long wait. Only time will tell.

It’s like a situation Love me Or Hate Me but you can’t ignore me…

Worth Tracking

6 Likes

Neysa getting acquired by Blackstone and Softbank should bring more clarity on valuations and numbers

2 Likes

Takeaways from the conference call

- Capacity of more than 3,900 cloud GPUs. Capacity will go up by 2048 GPUs by Mar 2026.

- Current utilization is 35%-40%. By Mar 2026 3900 GPUs will be 80%-90% utilized.

- 2 large orders from IndiaAI Mission for Rs.88 crores and Rs.177 crores. In advance discussions with both the IndiaAI team as well as the customers. Expect these to go live very soon.

- Guidance for Mar 2026 for the monthly run rate was 35-40 cr/ month. With above 2 orders, we should be able to meet MRR target much earlier than Mar 2026. Current MRR is Rs 16 cr/ month. The AI mission orders will add Rs 20cr/ month

- Continuing to see a very robust global demand for cloud GPUs

- Given the market scenario of like a lot of demand picking up for Blackwell, we are already in very advanced stages of placing the orders for nearly 2,048 Blackwell, majorly B200.

- Chennai location went live from 1st of August. Now, all of our capacity today is completely online and available for use by our customers

- EBITDA margin guidance is close to 70% plus/minus. We stand by that.

Disclosure: Invested

12 Likes

Journey to Mar 26 won’t be smooth, and only Mar can tell real value. Let’s hope it aligns. I will wait till then.

Exited recently after results.

1 Like

Gemini 3 was trained 100% on Google TPUs

Google has publicly confirmed that Gemini models were trained and deployed largely on its in-house Tensor Processing Units (TPUs), particularly TPU v4, v5e, and newer Ironwood variants. These chips are optimised for large-scale AI workloads and give Google full control over its infrastructure. This means Gemini is not dependent on Nvidia GPUs for its core training and cloud inference operations.

Source: ‘Could change AI’: Google Gemini is performing strong even without Nvidia GPUs

I believe hardware companies and compute providers are underestimating the rate at which AI models are advancing. This rapid progress renders hardware outdated, effectively turning today’s gold standard into tomorrow’s bottleneck.

3 Likes