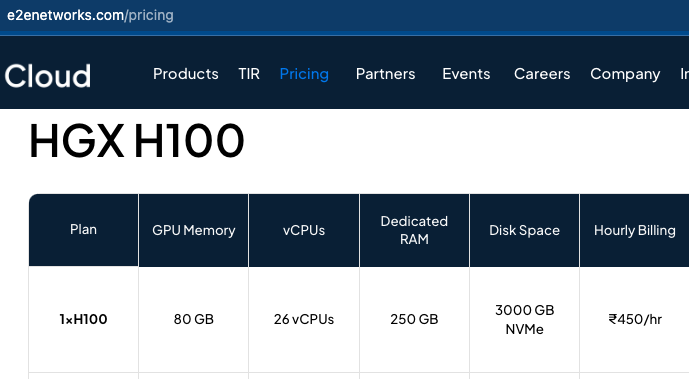

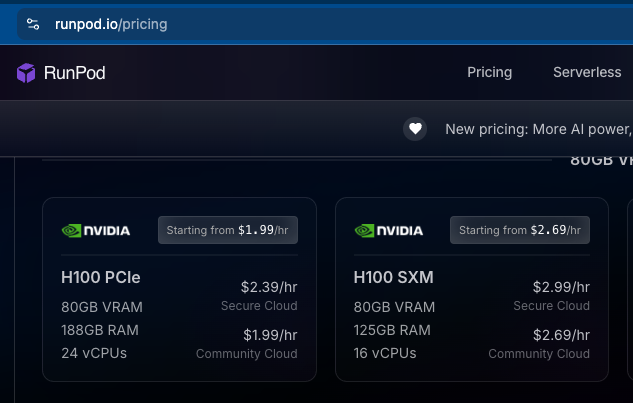

e2e h100 is ₹450/hour which is around $5.17.

runpod h100 is under $3

though the disk space is different, if i understand it correctly.

e2e h100 is ₹450/hour which is around $5.17.

runpod h100 is under $3

though the disk space is different, if i understand it correctly.

You cannot compare services of AWS vs E2E. There is very big difference between both. But team is able to use their GPU machines. Sometimes there is availability/CUDA issues but there are workaround via alerts and restart mechanism to solve it.

Good for gov. Challenging for currently empaneled companies. Gov got the leaders to set the lowest price and then opened it to the market keeping the price the top players are providing and then allowing everyone to participate.

This further leads me to think that GPUs are going to be considered a commidity like CPUs in the future.

The leaders will either depend on innovation and/or entrenching themselves in the ecosystem so deeply that all large orders flow through them and they provide the best price due to economies of scale.

GPU’s by itself will be a commodity. The value add and the differentiator will be the UI sitting on top of it, ease of use, latency, speed and technical support. So that is where E2E can either shine or fail. While NVIDIAs GPUs are the best in the world, their main differentiator comes from their inteconnect and their software CUDA that allows programmers to work on GPU’s and AI effectively. While the above rolling tender situation is a risk, E2E has priced fairly aggressively for the H100s with many bidders surprised, and then again, they would need to be vetted just like it happened in the beginning. So risk from existing players as it would not be too easy for new players, but why would anyone want to hurt their margins anymore?

Also the biggest player Yotta was not the cheapest for the H100s and they hold 50% of the capacity. Even if a new entrant quotes a lower value but has like 500 GPUs to offer, what is Yotta and E2E just backs off saying the margins are impossible to work with.

We have got the opportunity to meet the E2E management after the LT deal. Sharing my Key takeaways here

The Reason LT did deal with E2E was because of their Software.

Currently E2E has 2 Software offering

1.Cloud Software is used to create clouds and manage multiple servers and clouds.

2. TIR platform has a host of AI compute and Gen AI features. If any one wants to train a model on data TIR platform works like a plug and play in layman language. The TIR platform is very similar to Sage Maker.

E2E will now license the above software to public and private cloud customers.

Why will clients switch or take E2E cloud software ?

If we want to compute on MW basis then the calculation goes like this

E2E will charge roughly $2million dollar (So, pricing comes $2million/MW). This is visible in LT deal where e2e is charging 16cr/mw. and LT has 2MW data center live in panvel.

So, Deal with L&T is L&T will sell E2E software globally and domestically (Reseller agreement) where they will split the revenue. And E2E will also sell the software independently.

Demand projection

Globally 50GW clouds are expected to come. Where 30GW will be done by Hyperscalers(AWS,Google,Meta). The Remaining 20GW will be NCP (national and independent cloud players). E2E and L&T will target this.

Total opportunity size is 20000 MW * 16 cr/ Mw == 3.2L cr. As per data 20% of global data is generated by India. so, 4GW (4000 MW) cloud is expected in India

E2E expects they can get 500 MW in Cloud so roughly 8000 cr in license revenue.

Revenue can come from multiple streams 1. License revenue 2. implementation revenue 3. Modification requests 4. Managed services

Other interesting pointers

1.Internally E2E is working on how they can provide Gen AI solutions to enterprises without the requirement of any big tech thing. So that a non-techie can also use Gen AI solutions.

2. L&T along with group companies spend roughly 2000cr on AWS. They will slowly shift to E2E. 3. Gpu business now they first want to stablise the revenue. And that will come from getting more inference workload rather than training workload. Training workload requires a higher number of GPUs but they are spiky in nature. Whereas inference is sticky in nature.

4. Planning to hire Enterprise sales head.

5. Government AI mission is very complex. It will only support topline.

In Short, E2E is Transitioning form Hardware sales to Software sales. They are becoming a one stop solution for AI Infra solution. Any startup or enterprise wants to integrate AI or want to explore AI. E2E is one stop shop.

Thank you @HiteshTinna and team for the elaborated write up.

can not thank you enough for meeting the management and updating the forum.

Love every bit of this update.

Would have preferred this info coming from the management though.

I’ve said this before: Dua has a nose for changing winds.

As was being discussed a couple of days back, GPUs are going to be commodities, there’s no future for any company with big ambitions to have that as the main focus long term.

The projections look quite optimistic but plausible.

I don’t like the gov. business as well. Good enough to build credibility and improve the tech stack for Indian large scale use case but not to drive business.

In my personal experience, there’s a lot of improvement needed for the tech in E2E platform but hopefully it only goes up from here!

Thanks for sharing @HiteshTinna

Note: Not sure how sharing company based strategy in this selective manner is permissible by exchanges. I hope the company is coming out with this info soon, but it does seem like privileged info to me.

Cheers!

This IndiaAI mission is to showcase their capability. Secondly, Because of this IndiaAI mission. Management is expecting additional 3000Cr Demand of GPU every year. Which will be served by private players. So Industry is going to expand. A little bit hiccups always comes in every industry. But in Long term E2E is going to be the winners. They have the ability to Learn and adapt. Till now also the TIR platform has been developed from customers feedback. Although i Know the feedback loop is very slow. But it better to build a software that customer use rather than just build. And because now they have deep pockets things will change very fast with time, software will scale quickly than slowly.

Hi Hitesh,

Thanks for sharing this info. By approx when L&T will start on the 2MW data centre or it has already started? Did this meeting happened this Feb month.

Also regarding the 500MW in cloud for 8000cr for license revenue. Have they mentioned any projections like 3-5 year or something?

Also any projected timeline for this as well.

"L&T along with group companies spend roughly 2000cr on AWS. They will slowly shift to E2E "

E2ELTDEAL.pdf (93.8 KB)

why am i not able to find this document on nse announcements page. could you please link it from there? sorry for the trouble.

https://nsearchives.nseindia.com/corporate/E2E_05112024153329_SignedEGMNotice.pdf

Page Number 20,21,22,23

Somehow I also missed it. Reaching to page 20 in bull market is not easy.

Thanks a lot Hitesh for sharing your valuable inputs. Could you please provide an idea what kind of bottomline E2E can click in FY 28? Do you have any projections in mind? Also jio is heavily investing in data centres. How will competition impact E2E?

Well if I go by What management said to us I expect Roughly 1000cr Bottom line by Fy28 or 29. This is my wild guess. And i will be very happy if i go right.

Secondly, E2E along with LT will target Private Cloud Market in BFSI sector. Because there is were lot of activity is happening. Because BFSI has to store data locally for that they need Cloud.

Regarding JIO coming up with massive data centre. I don’t see that as a threat. And Reliance is entering in AI infra it means something. Because as AI will scale up you will need massive AI infrastructure for inference. And one good thing with Reliance is they expand the market or sector wherever they enter.

One more thing which i like to share is With coming of Deepseek. In India atleast the enterprise are now looking at adapting AI. because the cost of experiment has come down drastically. But caveat here is Because of IndiaAI mission the pricing of compute has also come down drastically. But the volume will increase.

And my channel checks says that AI compute Industry has gone to Pull mode then push mode. All thanks to deepseek.

Great work with the scuttlebutt. I do believe though that going from 160 Cr of topline to 1000 Cr bottom line is going to take much longer than 3-4 years, at least if they intend to grow without massive equity dilution.

E2E need to do capex to grow. Sure, they value-add on top of the basic infra, but without said infra they can’t grow.

Hence, if we go by the highest asset turns achieved in the past, it’s around 3.6 times in FY18. Assuming they’re able to match that, and also that they’re able to rapidly deploy the cash sitting in the balance sheet (close to 500 Cr), they can potentially have fixed assets close to 800 Cr. At peak asset turns, it could yield a revenue of about 2800Cr. Assuming a PAT percent of 25 (extremely optimistic numbers, never achieved in a full FY yet), that gives a PAT of about 700 Cr.

The demand definitely exists, no doubt. But the questions to ask are:

How soon can they convert the cash into cash generating assets?

How soon can they reach optimum capacity utilisation?

Can they maintain operating margins while doing so?

They could reach 1000 Cr profit some day if they execute well and continue generating cash like they have in the past. But it could take some time.

E2E no longer wants to grow Asset heavy GPU business which has become a commodity. With LT they are targeting Private Cloud space. Where they will License their Cloud and TIR platform

Hi Hitesh,

Good insights, would be interested to know the computation of $2 million per MW. From the EGM notice it is not getting clear if 30Cr is for 2MW.

Also, the 2000Cr usage of AWS by LnT group entities looks huge number. Will need to check if the same is valid. Also the workloads cannot be moved just like that from Hyperscalers like AWS and it takes time to move out of any Hyperscaler.