There is another thread on E-Pack durables but since it is locked starting a new one. (Admin can merge if deemed fit).

Industry Overview

-

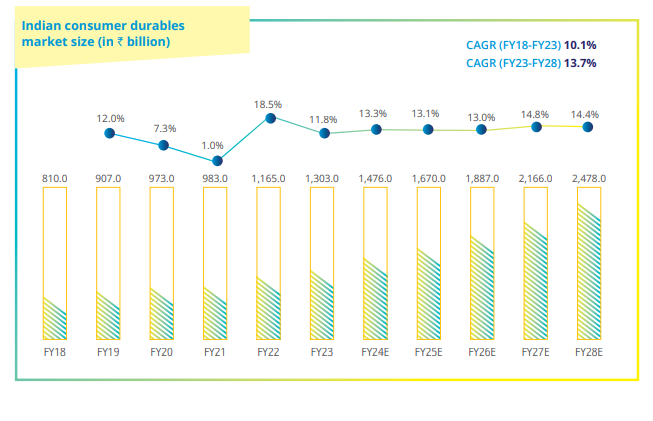

Indian Consumer durables industry is poised to grow from c.1300 bn to c. 2500 bn Rs at 13.7% CAGR from 2023-2028 with significant growth projected from the RAC segment.

-

Indian RAC market achieved a domestic sales value of C. 250 bn Rs in FY23 with volumes reaching 8.4 mn units.

-

This has substantially grown in FY24 due to heat wave conditions in most of India as the same is evident from the numbers reported by all major OEMS and ODMs in AC segment.

-

RAC manufacturers heavily relied on imported critical components (60-70% import reliance) , however the PLI scheme with c. 6500 cr has prompted many OEMs and ODMs to backward integrate.

-

The RAC market is estimated to grow at a CAGR of 12.1 % in volume reaching c.15 mn units in FY28 and 15.7% CAGR in value reaching c. 525 bn by FY28.

About the Business

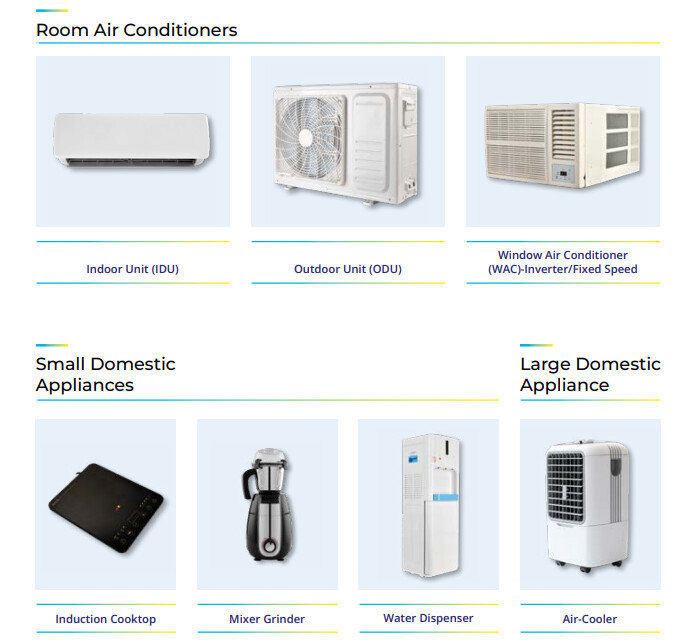

Epack durable is an ODM (Original design Manufacturer) which got listed in January 2024 . They claim to be the second largest ODM for RAC in India.

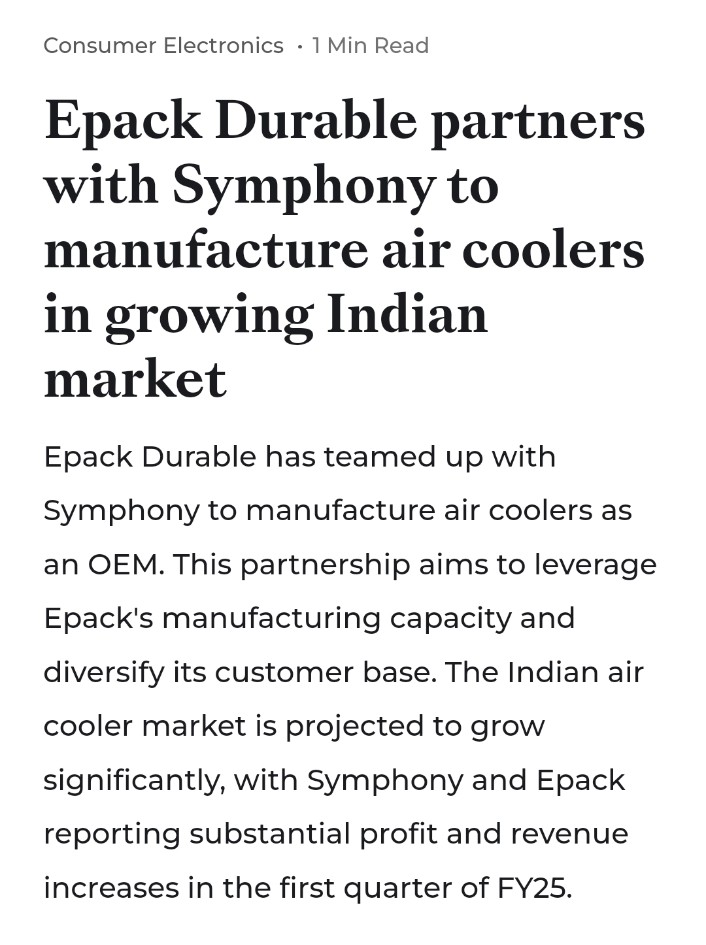

They also manufacture Small Domestic Appliances (SDA) : Mixer Grinders, Induction Cook top , Water dispenser and are planning to venture into Large Domestic Appliances (LDA) : Washing Machines, Room oil heater, tower fan, Induction water heater, hair dryer etc.

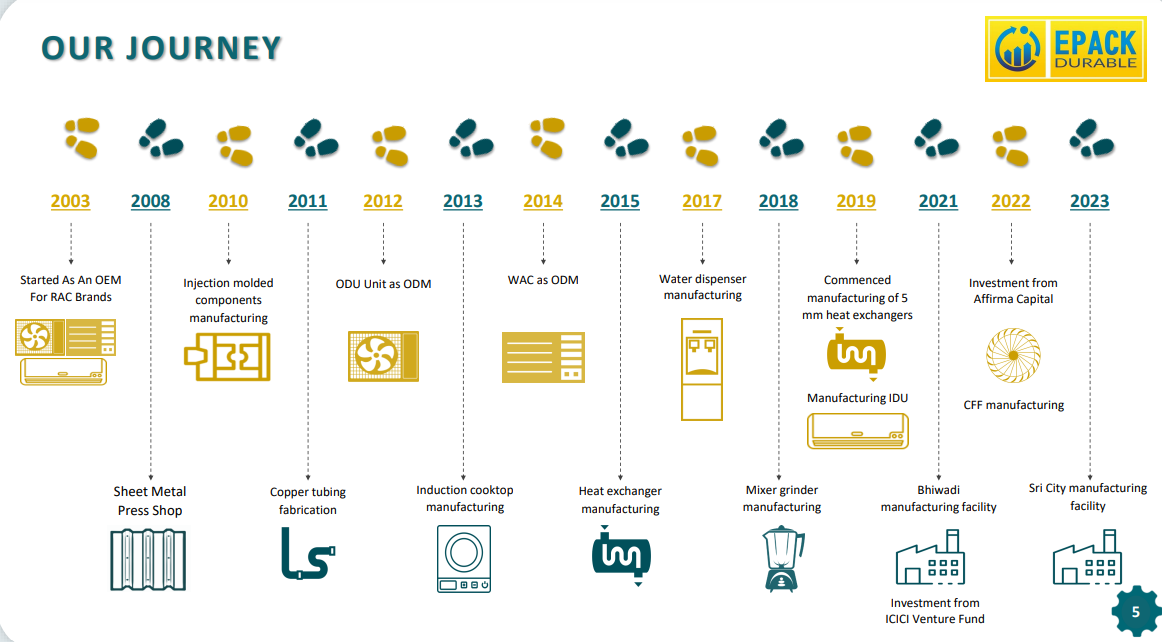

Incorporated in 2003, EPACK Durable (EPACK) started off as a contract manufacturer of

consumer durables such as RACs, Induction Cooktops, Juicer-mixer grinders, and water

dispensers for OEMs.

• Later in 2012 it transformed into an Original Design Manufacturer (ODM) for Air conditioners

and small domestic appliances. EPACK has grown significantly since then to become the second

largest ODM player with a market share of ~24%

• EPACK was founded by the Singhania and Bothra family who have been involved in

manufacturing consumer durables for more than two decades with extensive industry

knowledge and experience.

• It has 3 manufacturing facilities located strategically in Dehradun, Bhiwadi, and Sri city. All the

facilities enjoy strong backward integration offering cost competencies against its peers.

• About 80-85% of the company’s revenues come from the sale of RACs and their components

and the balance from small domestic appliances.

• It has marquee clientele, including Voltas, Haier, Philips, Godrej, Daikin, Havells, Bosch &

Siemens, Bajaj, Crompton & Greaves, Blue Star among others with whom it has established

strong relationships.

• EPACK received a total private equity investment of ~$40 million (approximately Rs. 320 crores)

from ICICI Ventures and Affirma Capital during FY2022 and FY2023 respectively, which was

largely utilized in capital expenditure during FY23 & FY24.

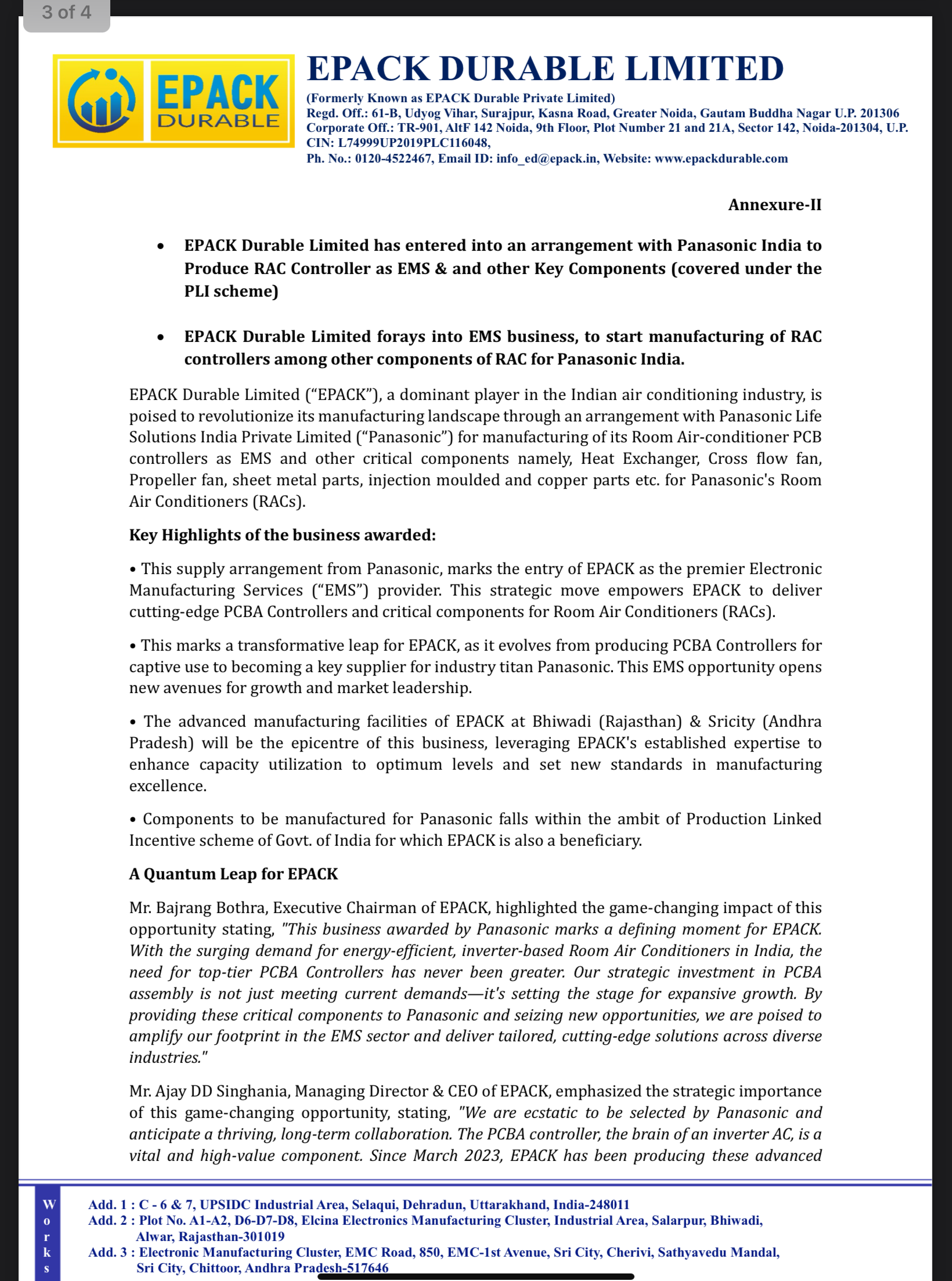

E-Pack has a fair amount of backward integration in its AC manufacturing including heat exchangers, cross flow fans, copper tubing, sheet metal, Plastic molding etc.

Manufacturing Facilities

.

** About the Management**

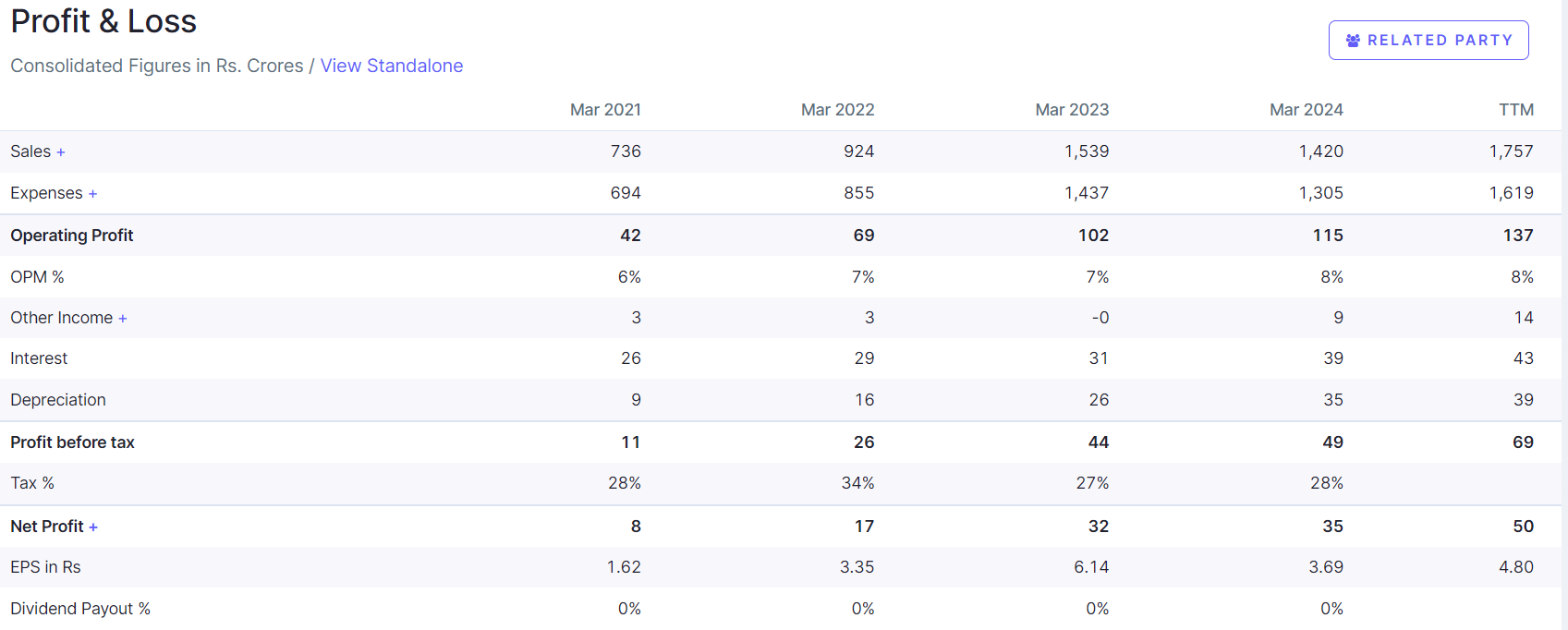

Financials and Valuation

Epack has achieved a 3 yr CAGR of 66% on bottom line.

Few inputs from the Concall

-

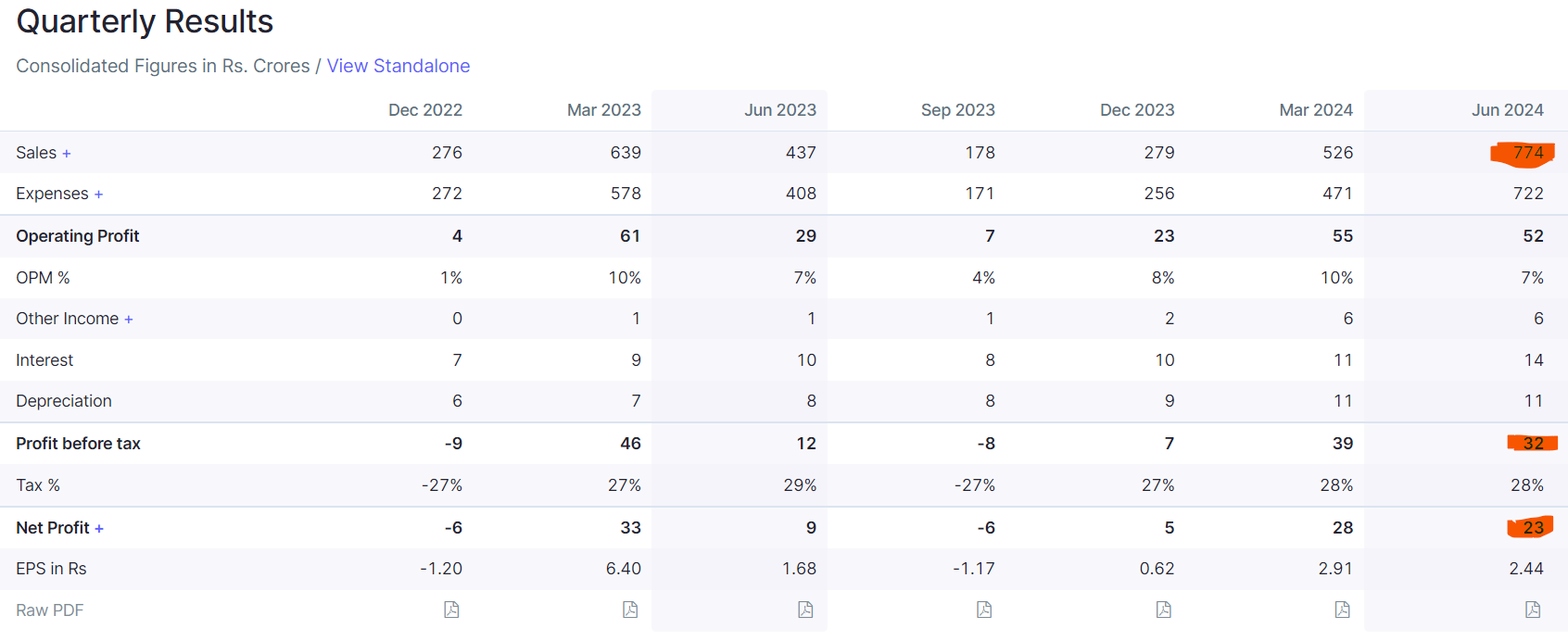

Reason for lower margins in QoQ is due to Sri City plant getting commissioned and material cost escalation. Due to pass through nature of cost , this can get postively impacted in subsequent quarter.

-

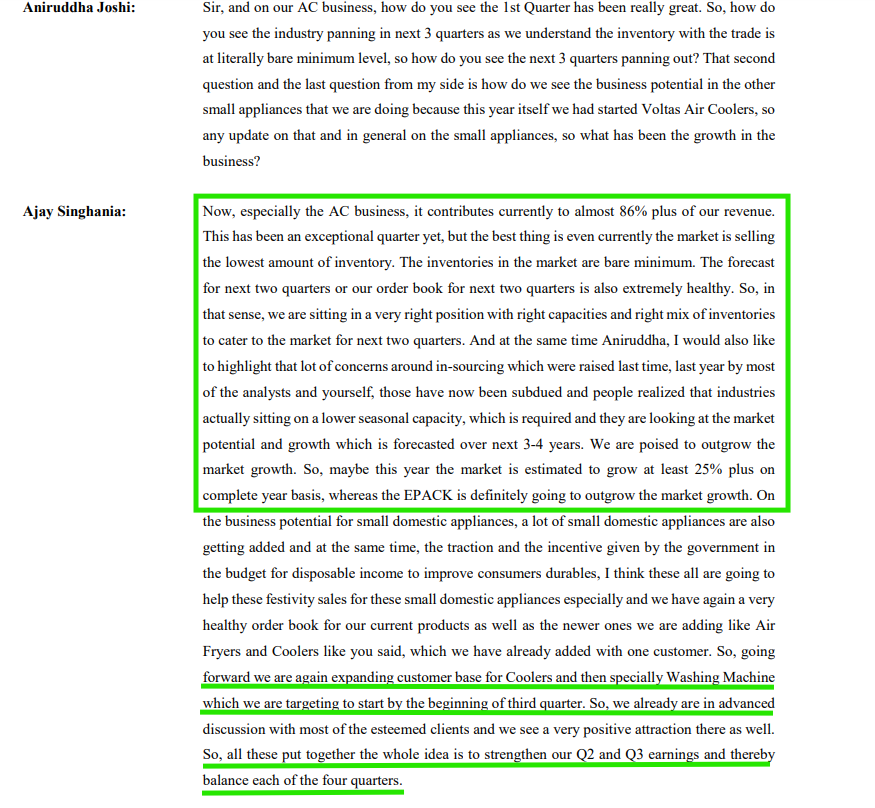

E-pack is starting Washing Machines with Fully automatic Top load variants and have signed with several top OEMs .

-

In FY 25 the total outlay for PLI is going to be C. 37.5 Cr and out of which C. 15cr is accounted in Q1.

-

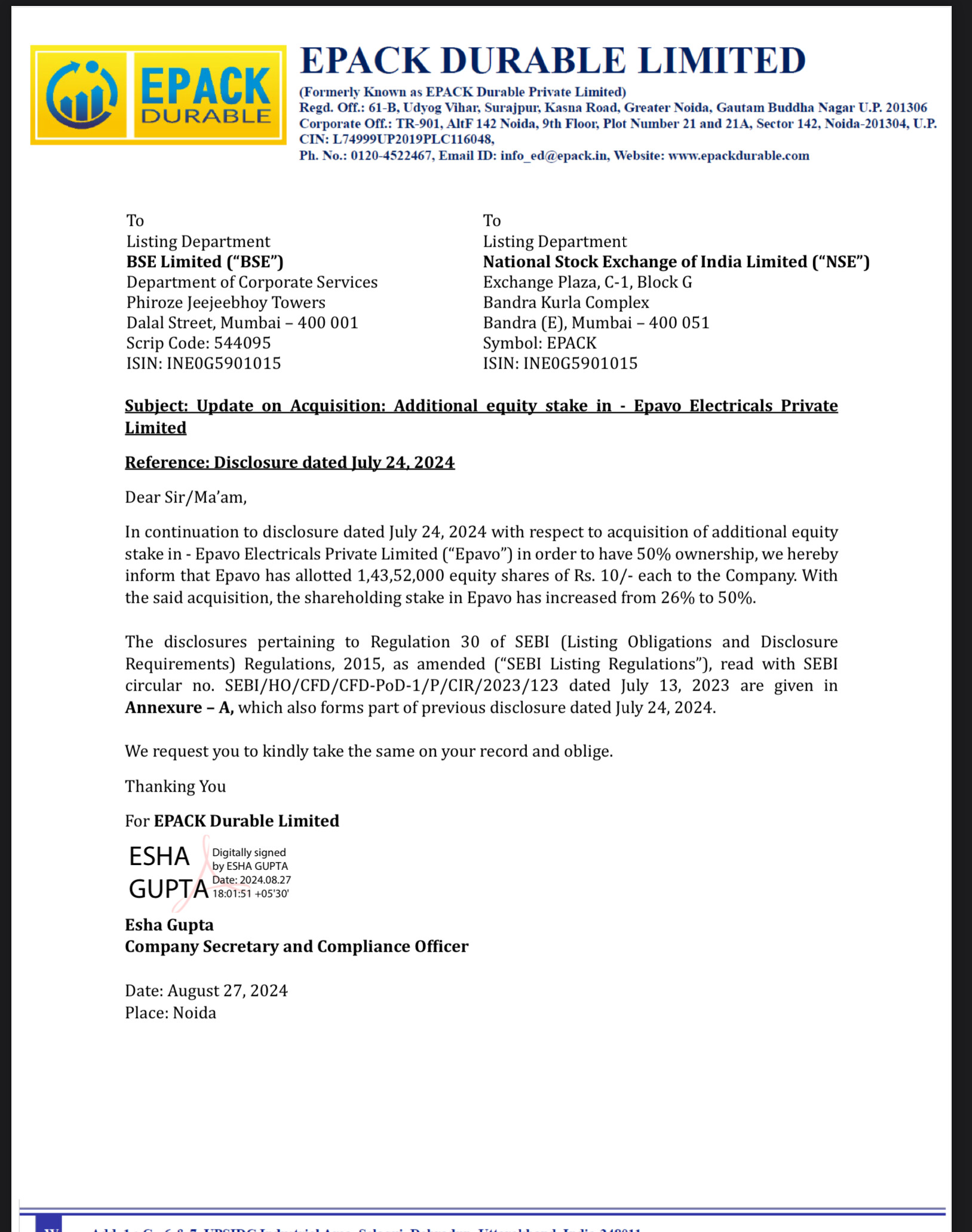

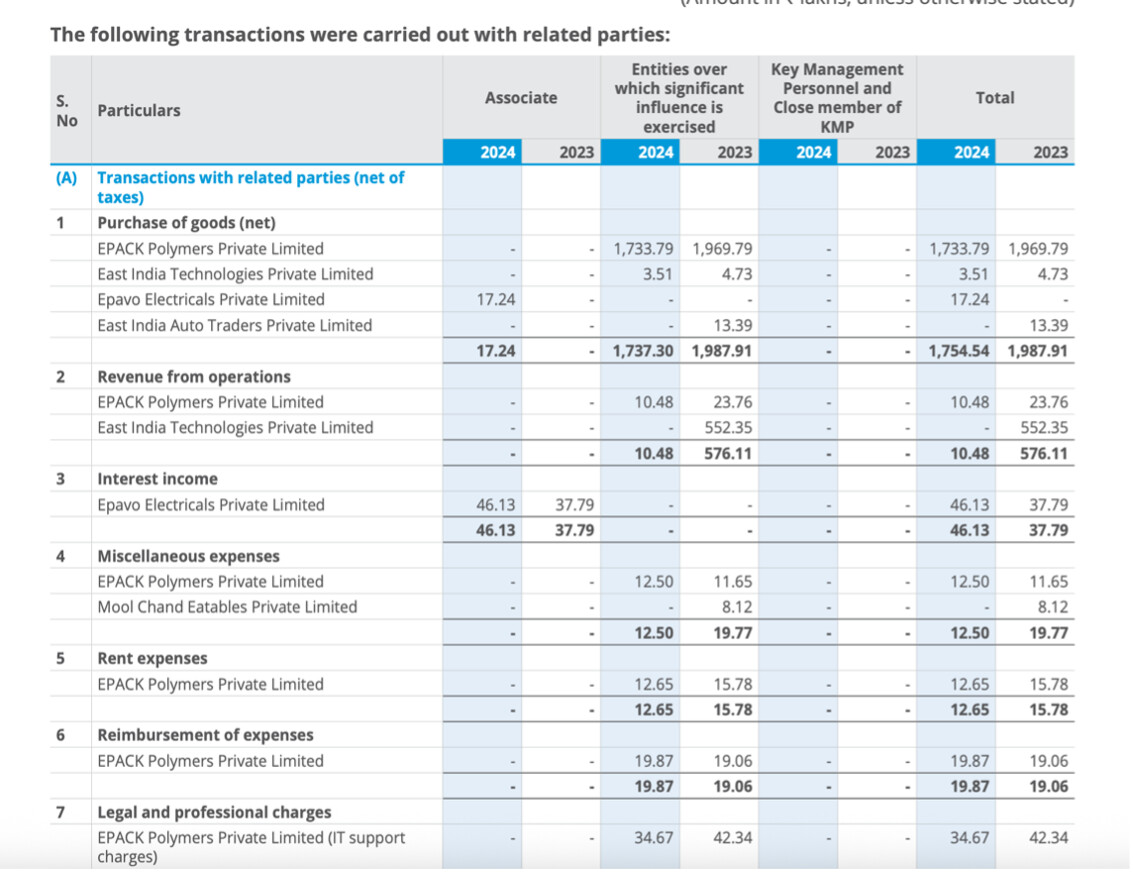

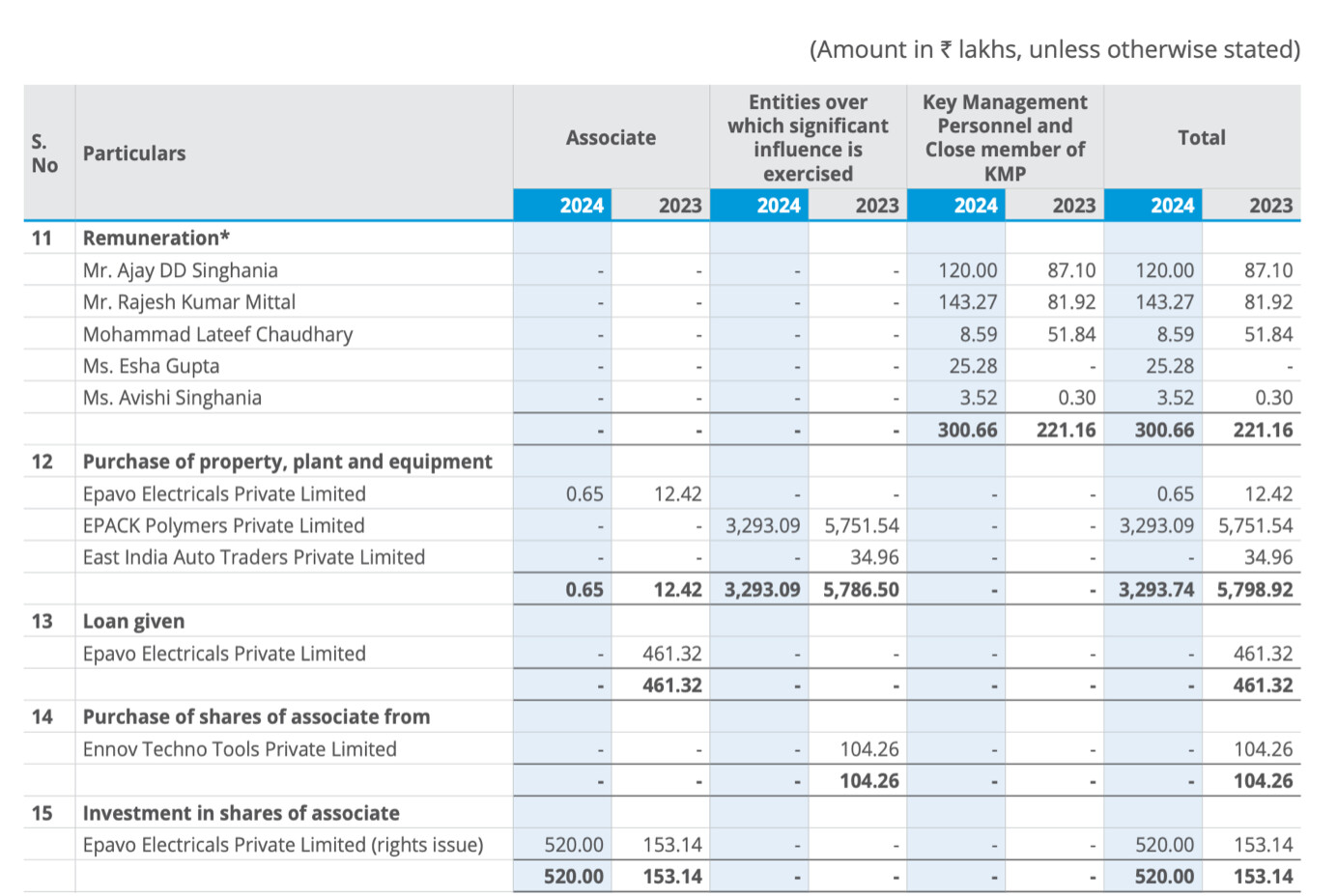

Epack has acquired 26% stake in associate company EPAVO in which 76% is held by M/s Rama Ratna Wires. Epack plans to enhance the holding to 50% soon. The company manufactures BLDC motors for AC, Fans etc. This unit also has PLI support.

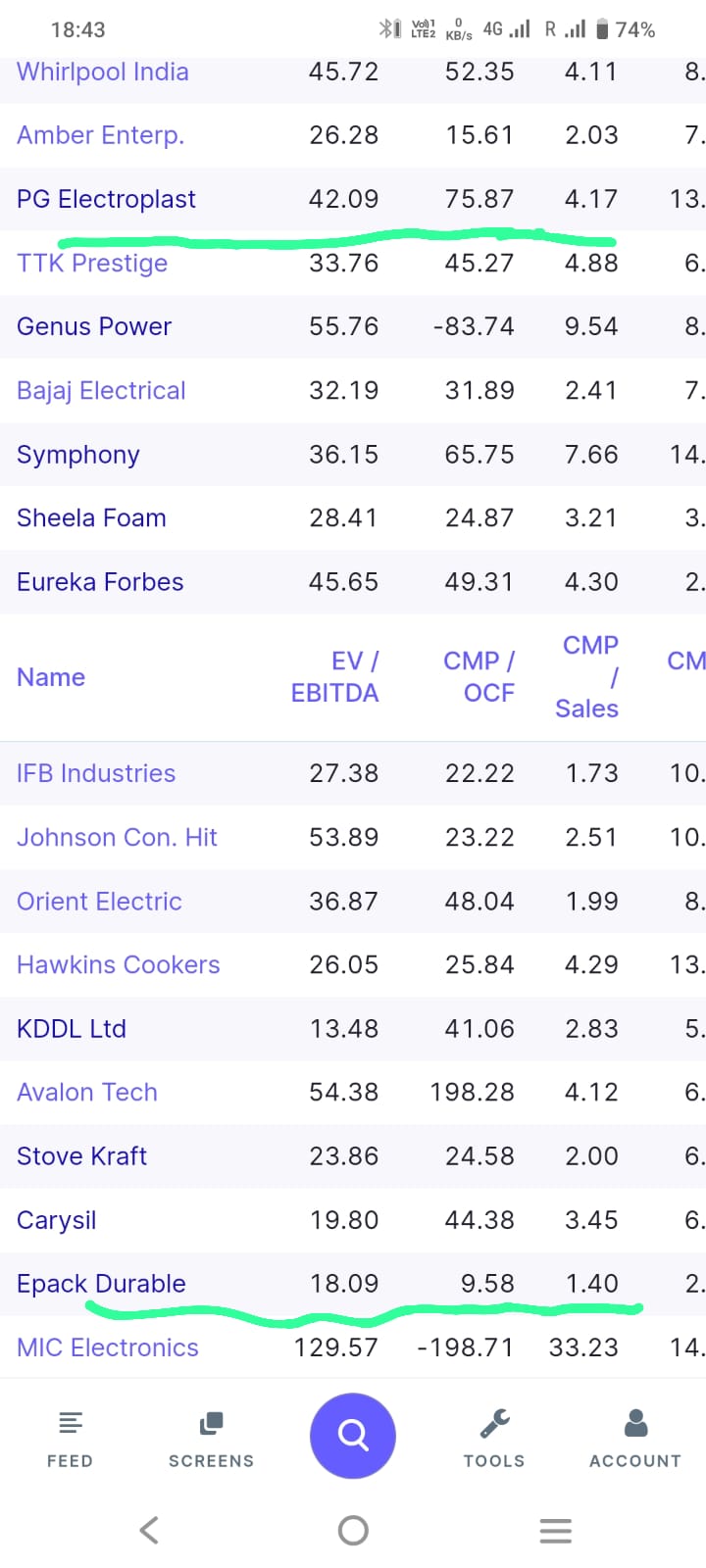

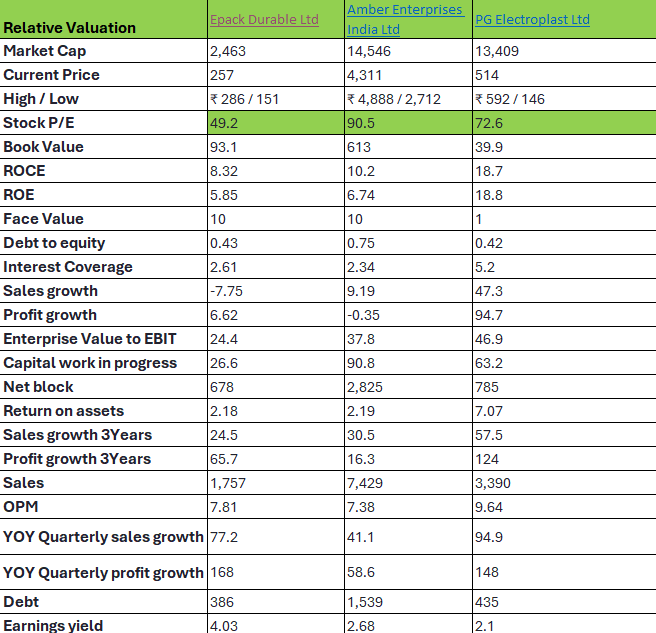

On a relative basis Epack looks cheap compared to peers Amber and PG electroplast.

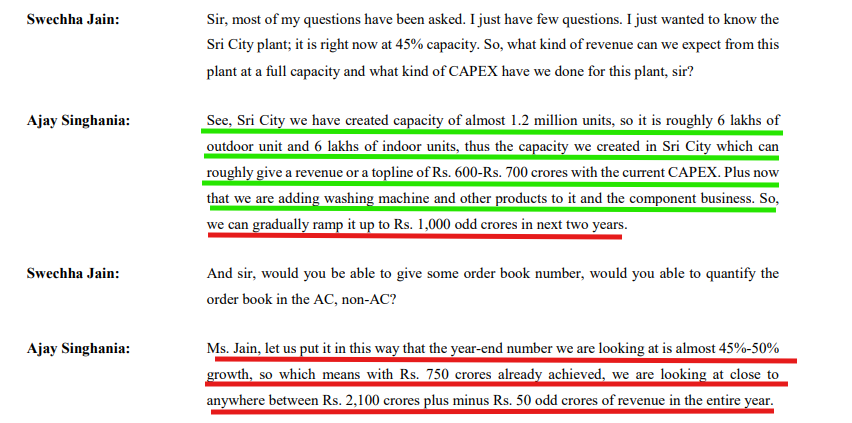

Based on the management guidance of 45% growth and 100 Bps improvement in margins ;

(Cooling of raw material prices , Sri City plant getting fully operational , Last 2 qtr trends )

FY 25 revenue = 2100 cr.

PAT = 63 Cr

@ 50 PE (current P/E : Industry peers at 75+) market cap= Rs 3150 Cr.

Current Market Cap = 2475 Cr

Potential Upside = 27%

Risks and Threats to the business

-

Several OEMs have started their own manufacturing facilities due to import restrictions and PLI benefits. Since Fy 24 AC sales soared due to Heat wave conditions the impact was not fully understood. Once the OEM facilities come on steam fully only the impact will be understood.

-

Epack is diversifying into Washing Machines and other Large domestic Appliances. How they manage this transition is to be seen.

-

RAC business is seasonal in nature with Q2 and Q3 typically muted in nature. This can lead to short term pain and price erosion.

-

The company has c. 350 Cr debt. Even though the interest coverage is comfortable and company has done most of the capex already this can be a deterrent if the cycle turns .

Conclusion

E-pack durables is available at almost the listing price, it has several industry tailwinds going for it and looks to be cheap relative to peers. The company adding new product lines and additional capacity can add to future top line growth. The company has good amount of back ward integration , with the govt push for components (via PLI and import duties) will also aid the growth.

Disc : Invested a tracking quantity . Might add or reduce without prior intimation. Pls do your due diligence

Sources : Company Presentation, AR, Concall transcripts