On the face of it, it looks like a bad company. Poor history, bad ratios and chequered past. However what caught my eye were a few changes that management was adopting.

Let me run you through the history of the company

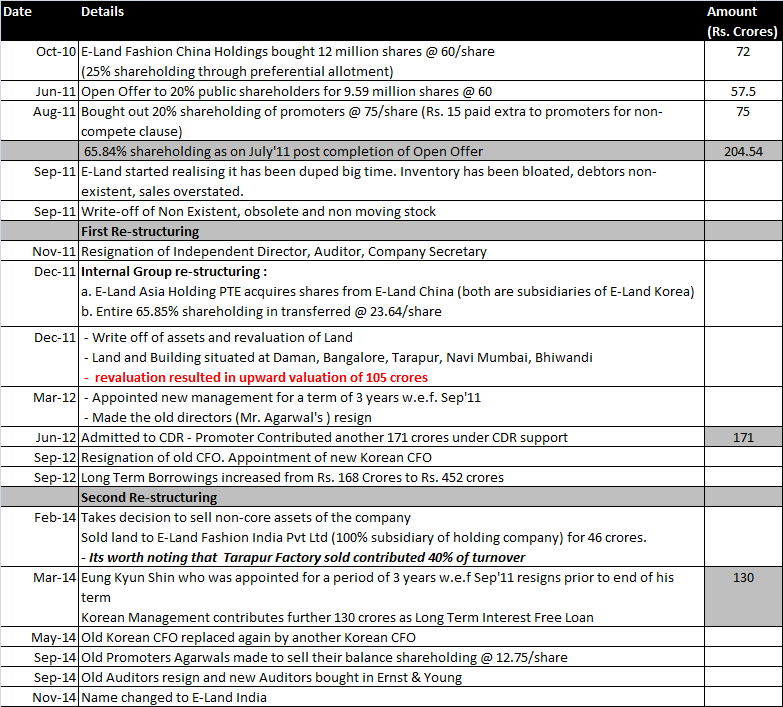

E-Land Apparels was knows as Mudra Lifestyle. In 2010, E-Land of Korea made an open offer to buy into Mudra from the erstwhile owners (we will later see, how the old owners apparently played foul)

**E.Land Group is currently the second largest retailer in South Korea and the group is worth USD 20 billion. (website : http://en.eland.com/group/group01.html)

So, old promoters got multiple shocks one after another after acquiring the company.

It is worth noting, that they didnt give up and have continously pumped in more money and more management man power into the Indian venture.

What I liked

As of date, they have pumped in close to Rs. 500 crores in the Indian company

In the second re-structuring, they have bought in new management, bought in a Big-4 auditor,

Sold Non Core Assets

We are still getting the company at less than 1/2 times of the value which promoter has pumped in (200 crore market cap as on date)

Company has started showing signs of turnaround and has started reaching breakeven levels

Disclosure : I recently bought shares in it and it is 2% of my portfolio as on date

This is an educational post and no investment decision should be taken on the basis of this post. I am not a SEBI Registered Investment Analyst

It is worth noting that during the revaluation done during year ended Mar-2012, Land and Buliding of the company itself was valued at 180 crores and Plant & Machinery at 340 crores (after impairment), i.e. a total of 520 crores in Tangible Assets

Thereafter Tarapur Factory was sold for 46 crores.

Management has been pretty straight and honest in their reporting. Soon after taking over they had written off 100 crores of overstated inventory. I would tend to believe that the revaluation shows a true picture and hence we have 480 crores worth of Tangible Assets against market cap of 200 crores as of date

@ashwinidamani The quarterly results show 300 crores of long term debt on books. However interest payments are accounting for only 94 lakhs as quarterly outgo. Also no decent cash on books but other income in September quarter of over 2 crores. Can you help ?

The new management was pretty straightforward and wrote off inventory of 100 crores. They could have postponed this decision or not done it at all. No one would have known.

Also they have apointed a Big 4 Auditor recently. Which management would want to fudge accounts and still change their small auditor to a Big 4 Auditor.

@karu_lamborghi_ Debt from related party (Eland group) is interest free. For CDR Debt also, interest would be under moratarium

Please go through Annual Report of 2014-15 - Section Long Term Borrowings

True the stock has started picking up after these positive changes from management.

But before anything else can anyone help me in understanding the sector and it’s prospects in next two years?

Stocks like Indo Count , Welspun India had a unbelievable run in past two years ; Is this explosive growth of textile sector going to be sustainable or has the time come to flip the game in China’s favor ?

There is no CDR debt. The debt outstanding is from the holding company. The details are

Loans and Advances from related parties is interest free and is repayable as per below schedule :-

10% of the loan amount not before December 31, 2022

20% of the loan amount not before December 31, 2023

Balance 70% of the loan amount not before December 31, 2024

The concern here why such a long term loan is given. Is it becoz with P&L negative of Rs 217 cr, management sees a long road for recovery.

They are not able to sell Daman unit and shown as Assets held for sale. A possible write-off of Rs 25 cr ( Maximum) can happen on this.

Rs 15 cr yet to be received on slump sale ason 31-3-2015. I hope they have received this from E-Land Fashion

3.We need to understand the relationship between ELand and Eland Fashion and more on manufacturing abilities and locations.

Manpower Cost 30% of the sales . We need to understand why such a high ratio. Possible due to underutilisation and can drop when sales increase.

The main concern here is point no 1 Loan shows the pessimism of the management.

Again the appointment of Elizabeth Ravi as Director, Can’t make out why?

An amount of Rs 217 cr has to turn positive before they can repay the LT loan or pay dividend. A reasonable estimate can be made on this only after analyzing performance for atleast 4 qtrs.

Discl: Not Invested but tracking becoz of the Parentage.

Regarding manpower cost you would observe that they are same as last year. Last years ratio was roughly 16%. This year the sales have dropped due to slump sale of Tarapur Unit which contributed 40% of the turnover. What is worth researching is that how much would the slump sale of Tarapur Unit affect the company. Also if you go back and check the Red Herring Prospectus of Mudra Lifestyle (filed in 2007), IPO funds were raised for Tarapur factory construction. What I mean to say is that the company isnt solely dependant on Tarapur and it is a latest addition

Assets held for sale is an Accounting Requirement. When the board/mgmt gives an in principal approval for disposal of certain assets, they have to disclose it under Assets Held for Sale. Yes you are right, that they havent been able to close the sale fast, but lets watch for some more time

For the borrowings section and your observation of Point No. 1 Loan, I would request you to check Annual Report of FY 2012. The company did undergo a CDR mechanism and the details are mentioned in the Annual Report. You will not get the Annual Report on company’s website, but it is available on BSE

This is based on my interaction with the management

Post the acquisition, the company has been facing one shock after another. However the management is extremely focussed.

The have repaid the entire term loan of Bank using the promoter’s loan fund infusion

The core business hasnt been changed despite the challenges. E-Land continues to supply clothes to various branded garment manufacturers (The names of the branded retailers werent shared, but my best guess is Zara is one of them)

Company is extremely focussed on cost. The head office has already been shifted to Suburban Mumbai and manpower rationalisation is also happening. They are constantly engaging with suppliers for re-negotation of key contracts

Focus is now on increasing sales and the management is exploring a few options. Details cant be divulged and we have to wait for corporate announcements.

Daman plant is already available for sale, but the management doesnt want to do a distress sale and is waiting for the right value.

Auditors have helped lot in terms of increasing controls.

I have gone thru all the reports. I meant there is no CDR debt now. I should have added "now " in addition to “is”. Please verify your figures of 16% for Sep 15 and Mar 15. Have you done any adjustments to for arriving at 16%. The concern is mainly on the long repayment schedule of the promoter loan. It is almost 7 years and back ended.

I think fabric is in Tarapur Unit and Garment in Bangalore unit. I still dont understand why there is slump sale of Tarapur unit when they say they are going to manage the fabric from now onwards. E-Land fashion is also showing a Tirupur unit. IMHO there is no clarity on this relationship. Can you please help?

Well during my discussion with management, they mentioned that Tarapur factory was a loss making unit right from the time it was started. Hence when they were looking to sell the non-core assets, Tarapur was first on their list. (Tarapur was added after IPO of Mudra)

The 16% is based on Apr’13 - Mar’14 financials. (5581 lacs/32183 lacs)

Thereafter they sold the Tarapur unit, hence there was a drop in sales without the employee reduction

Well for me the long repayment schedule is a positive. Here is a parent company which is ready to give a long term support to its subsidiary (and that too interest free).

Regarding the relationship part between E-Land Fashion and E-Land retail, even I am yet to understand the difference between the work of each.

There are challenges and there are issues with the company, that is why it is available cheap. If things were perfect , we wouldnt have got it at this value.

I don’t see why no one has raised this point…but how is sale of Tarapur unit to a wholly owned subsidiary classified as “selling of non-core assets”? The subsidiary’s losses would still be the parent’s losses and ultimately it will have to be funded further to keep the unit going. So is this just an attempt to get rid of this unit from the balance sheet but still effectively keep shouldering the losses from it?