- Tariff Fears: The U.S. government is considering imposing new tariffs on copper imports, which is driving buyers to stockpile copper before the potential price increase. Traders are reacting by sending copper into the U.S. to take advantage of higher prices.

- High U.S. Demand: U.S. copper prices are higher than the global prices, which is attracting copper from other regions, particularly Asia and Europe, to take advantage of the price premium in the U.S.

- Decreasing Copper Exports from Chile: Chile, the world’s largest copper exporter, has been facing challenges, including labor unrest and lower copper ore grades. This has led to a decline in its copper exports, tightening global supply.

- China’s Increasing Demand: China’s copper demand is rebounding, leading to an increase in copper purchases, which is further tightening the global copper supply.

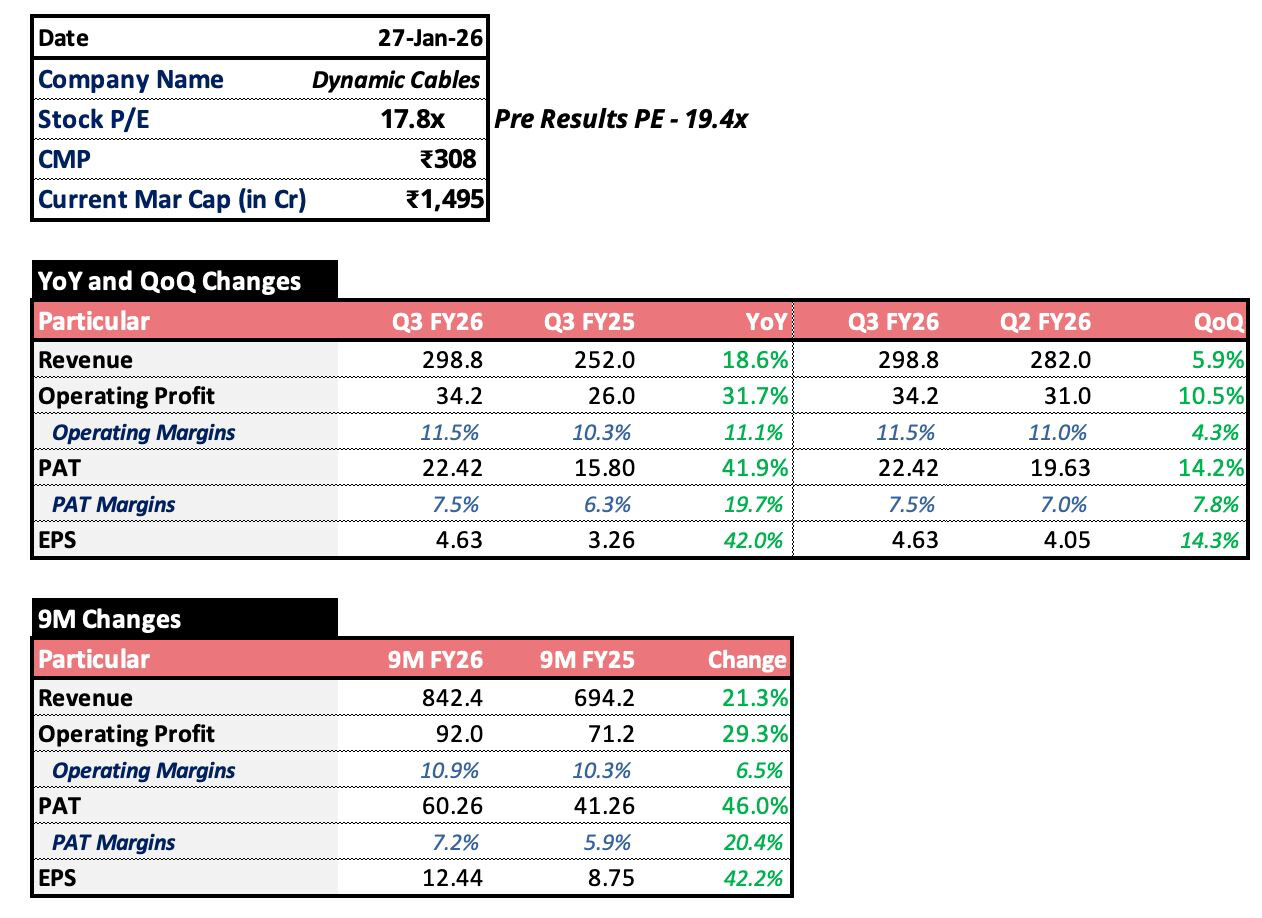

But Dynamic Cable will have no impact because 80% of the raw material is aluminium and 20% is copper and all increase in the price is fully passed on that’s why they are able to maintain the margin of 10% over last 4-5 quarters.